CARI Captures Issue 719: Cabinet reshuffle sparks concerns over Indonesia’s future fiscal credibility

Captures has widened its scope to include news related to all the members of the Regional Comprehensive Economic Partnership (RCEP) agreement which was signed towards the end of 2020. Besides the ASEAN Member States, this includes Australia, New Zealand, China, Japan, and South Korea. The other weekly newsletters under CARI, China-ASEAN Monitor and Mekong Monitor will also be consolidated into the Captures newsletter. We hope this new version of Captures will serve you better and look forward to providing a curation of stories relevant to ASEAN and its trading partners.

INDONESIA

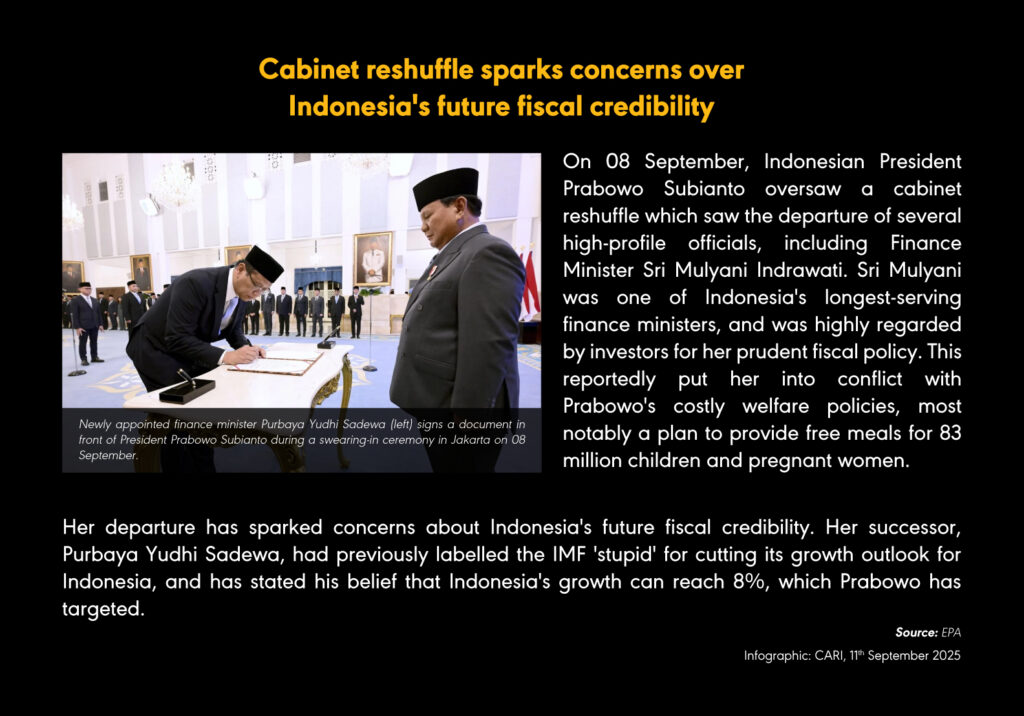

Cabinet reshuffle sparks concerns over Indonesia’s future fiscal credibility

(09 September 2025) Indonesian President Prabowo Subianto on 09 September announced a cabinet reshuffle that removed several officials, most notably Finance Minister Sri Mulyani Indrawati, The move was prompted by recent nationwide protests over lawmakers’ housing allowances, economic inequality, and rising living costs, with the unrest resulting in 10 people being killed and five remaining missing. Sri Mulyani was one of Indonesia’s longest-serving finance ministers and was highly regarded by investors for her prudent fiscal policy. This reportedly put her into conflict with Prabowo’s costly welfare policies, most notably a plan to provide free meals for 83 million children and pregnant women. Sri Mulyani had reportedly previously offered her resignation after Prabowo had instituted cuts of up to USD 48 billion in government spending to fund his populist agenda. New finance minister Purbaya Yudhi Sadewa, previously head of the Indonesia Deposit Insurance Corporation, drew criticism after remarks downplaying the recent protests and asserting that 6–7% growth would end the unrest, before apologising and reaffirming confidence in Prabowo’s 8% growth target within two to three years. Sri Mulyani’s departure has sparked concerns about Indonesia’s future fiscal credibility, with Prabowo having voiced his desire to remove a legal deficit ceiling of 3% of GDP for the annual budget.

INDONESIA

New finance minister announces USD 12 billion cash injection to boost lending

(11 September 2025) Indonesia’s new finance minister Purbaya Yudhi Sadewa announced a USD 12 billion cash injection to boost lending, transferring IDR 200 trillion—half of the IDR 400 trillion in government reserves held at the central bank—to state-owned banks, with instructions not to use the funds for government debt purchases but to accelerate loan growth, currently at a three-year low. Sworn in on Monday after Sri Mulyani Indrawati’s removal, Purbaya told lawmakers he aims to “rev up the monetary and fiscal engines” and pledged to drive growth above 6% towards President Prabowo Subianto’s 8% target, citing financial “drought” from slow spending and weak money supply. He said the transfer, drawn from underspent reserves, would not be inflationary, as inflation in August was 2.31%, below the 6.5% growth threshold that might trigger risks. The move follows a smaller IDR 16 trillion transfer earlier this year for low-cost housing and village cooperatives, and contrasts with Indrawati’s reluctance to release reserves at this scale. Markets reacted with Jakarta’s benchmark index rising for a second day, led by financials, though the rupiah remained 1% weaker and bond yields were stable, with investor sentiment still cautious after Indrawati’s exit. Purbaya said budget absorption, particularly for large allocations such as free school meals, will be monitored more closely, while Bank Indonesia has cut its policy rate by 125 basis points since September and reduced SRBI issuance to expand liquidity.

MALAYSIA, VIET NAM

Elevation of Malaysia-Viet Nam relations to strengthen economic, cultural, and educational cooperation

(10 September 2025) Malaysia’s Consul General in Ho Chi Minh City said on 10 September that the elevation of Malaysia–Viet Nam relations to a Comprehensive Strategic Partnership (CSP) in November 2024 would strengthen cooperation in economic, cultural, and educational sectors. Bilateral trade in 2024 reached USD 18.14 billion, with more than 700 Malaysian projects registered in Viet Nam, while the number of Vietnamese students in Malaysia rose by over 340% between 2022 and 2024. The High Commissioner highlighted Malaysia’s ASEAN chairmanship in 2025 under the theme “Inclusivity and Sustainability,” focusing on regional integration, digital transformation, and coordinated responses to global challenges. The remarks were delivered during Malaysia’s 68th National Day and 62nd Malaysia Day celebration in Ho Chi Minh City, attended by the Vice Chairman of the city’s People’s Committee, diplomats, and members of the Malaysian community.

MALAYSIA

Malaysia slows data centre expansion amid electricity and water constraints

(12 September 2025) Malaysia is slowing its data centre expansion amid power grid and water resource constraints and growing U.S. pressure to prevent Chinese firms from using the country as a channel to access U.S.-made AI chips under export controls. More than two-thirds of Southeast Asia’s data centre capacity under construction is committed in Malaysia, with Johor emerging as the hub, hosting 12 operational sites totalling 369.9 MW and 28 planned projects adding 898.7 MW, representing 78.6% of national IT capacity and MYR 164.45 billion in approved investments by Q2 2025. In July, Malaysia mandated permits for all exports, trans-shipments and transits of high-performance U.S. chips, such as Nvidia’s, though rules still allow Chinese data centres to import chips for in-country use. Washington has raised concerns that such facilities could train AI models for Chinese military purposes, adding sensitivity as Malaysia negotiates a trade deal with the U.S. Chinese operators, including GDS Holdings, have adjusted by spinning off overseas units such as DayOne, citing regulatory divergence and trade tension. Johor’s vetting committee for new projects, introduced in 2024, initially rejected about 30% of applications over sustainability concerns, though approval rates have since risen. Despite political momentum under Xi Jinping’s Belt and Road Initiative, including pledges on AI and 5G cooperation after his April visit to Malaysia, analysts warn scrutiny and tariffs could curb Chinese data centre expansion in Southeast Asia.

SINGAPORE

Inland Revenue Authority reports tax collection of SGD 88.9 billion for April 2024-March 2025 period

(11 September 2025) Singapore’s Inland Revenue Authority (Iras) reported tax collection of SGD 88.9 billion for April 2024–March 2025, a 10.7% increase from SGD 80.3 billion the previous year, representing 76.9% of government operating revenue and 12.2% of GDP. Corporate income tax rose 6.7% to SGD 30.9 billion, remaining the largest contributor at 34.8% of collections, though down from 36.1% previously. Goods and services tax increased to SGD 20 billion, or 22.6% of revenue, driven by higher spending and a GST rate adjustment. Individual income tax rose to SGD 19.1 billion, while property tax and stamp duty each grew to SGD 6.6 billion, up from SGD 5.9 billion and SGD 5.8 billion respectively. Tax enforcement actions involved over 8,600 cases, yielding SGD 507 million in recovered taxes and penalties, down from SGD 857 million recovered from 9,590 cases a year earlier. Iras disbursed more than SGD 1.3 billion to around 127,500 businesses under schemes including the Progressive Wage Credit Scheme and Senior Employment Credit. Digital services were enhanced through the expansion of eGiro from two to seven banks and its rollout to corporate taxpayers, alongside upgrades to the myTax Portal with simplified navigation and centralised notifications.

THAILAND

Public debt stands at 67.9% of GDP, among highest in ASEAN

(12 September 2025) Thailand’s public debt stands at 67.9% of GDP, among the highest in ASEAN, and is projected to rise to 68.9% by 2028, with recurring expenditures exceeding 70% of total spending and supplemented by short-term stimulus and tax relief measures. The IMF on 11 September urged prudent fiscal management and consolidation to build buffers, highlighting Thailand’s relatively higher debt compared with regional peers. The Fiscal Policy Office data show Thailand’s fiscal deficit has widened across administrations: –0.8% of GDP in the Thaksin–Surayud era, –2.2% under Abhisit–Yingluck, –2.7% in early Prayut years, –3.9% during Covid-19, and –4.0% under Srettha–Paetongtarn. Economists are questioning the feasibility of reviving the Khon La Khrueng (Half-Half) Co-payment Scheme, warning that limited fiscal space—less than THB 5 billion available—requires reallocations and a clear redesign to balance between supporting small shops and stimulating consumption. The IMF is monitoring political uncertainty and border tensions, with updated economic forecasts to be released in October.

VIET NAM

Government warned that rapid credit expansion may fuel inflation and asset bubbles

(11 September 2025) Vietnamese academics warned lawmakers on 5 September that rapid credit expansion risks fuelling inflation and asset bubbles as the government pursues 8.3%–8.5% GDP growth, well above external forecasts, despite new U.S. tariffs on exports. One economist highlighted that Viet Nam’s money supply growth has led to the region’s highest credit-to-GDP ratio, with loans in 2024 reaching 136.4% of GDP (USD 476 billion), over three times the median for emerging markets. Bank credit expanded 19.3% in H1 2025, exceeding the central bank’s 16% full-year cap and well above the 14% average of the past five years, with much directed to real estate, creating “ghost cities” and pushing up prices. Tthe credit surge has been linked to a stock market rally, with margin debt exceeding USD 11 billion in Q2, about 5% of market capitalisation, while bad debt rose to 5.3% of loans by February from 5% last year. The World Bank noted banks’ capital buffers have nearly halved in three years, raising vulnerability. Despite inflation at 3.2% in August, the government has not indicated plans to slow credit growth and intends to remove credit caps from 2026, a move Fitch Ratings warned could escalate systemic risks without tighter prudential controls.

RCEP Monitor

SOUTH KOREA, UNITED STATES

US and South Korea remain in deadlock over USD 250 billion investment fund

(09 September 2025) The US and South Korea remain in deadlock over a USD 350 billion investment fund central to their July trade deal, with South Korea’s director of national policy at South Korea’s presidential office warning on 10 September that even the Make American Shipbuilding Great Again (MASGA) project may not proceed without agreement. Washington has presented Seoul with draft terms similar to Japan’s USD 550 billion pledge finalised last week, but Seoul has rejected this, citing differences in economic scale, foreign exchange market risks, and the yen’s reserve currency status. Kim stressed that beyond governance and profit-sharing issues, the core challenge is securing and managing USD 350 billion in foreign exchange, adding that South Korea intends the pledge to be structured mainly as loan guarantees rather than capital injections. The fund is tied to the preservation of a 15% tariff on South Korean imports, while US auto tariff cuts for Seoul have not yet been implemented by executive order, leaving working-level talks ongoing. Additional tension stems from a US immigration raid on a Hyundai–LG Energy battery plant in Georgia, where hundreds of South Koreans were detained, raising concerns over Korean firms’ willingness to invest in the US. Kim cautioned that while tariff reductions for autos are significant, the scale of the investment fund risks destabilising South Korea’s economy if rushed.

AUSTRALIA

Future Fund’s valuation reaches AUD 252 billion as of 30 June

(09 September 2025) Australia’s Future Fund reported on 10 September that its valuation reached AUD 252 billion (USD 166.22 billion) as of 30 June, delivering a 12.2% annual return, more than double its 6.1% mandated target, while shifting allocations away from the US towards Germany and Japan. Investments in developed markets rose to AUD 65.13 billion, up from AUD 46.83 billion in 2024, representing a quarter of total assets, while Australian equities increased to AUD 27.2 billion from AUD 23.1 billion. Future Fund’s CEO said the US remained the fund’s largest international recipient but cited tariff changes, taxation adjustments, political uncertainty and fiscal imbalance as reasons for reducing exposure. Property holdings declined to AUD 11.1 billion from AUD 12 billion, and credit investments fell to AUD 22.4 billion from AUD 24.82 billion, while allocations to developed market currencies and commodities, including gold, were raised. Arndt highlighted Germany’s fiscal stimulus measures and Japan’s relative equity market value as driving factors for the diversification.

CHINA

Exports rise 4.4% year-on-year in August 2025, weakest pace in six months

(08 September 2025) China’s exports rose 4.4% year-on-year in August, the weakest pace in six months and below July’s 7.2% growth, while imports increased 1.3% compared with 4.1% the previous month, according to customs data released on 9 September. Exports to the US fell 33% amid ongoing trade tensions, while shipments to south-east Asia rose 22.5% and to the EU 10%, contributing to a trade surplus of USD 102.3 billion, up from USD 98.2 billion in July. Goldman Sachs noted August weekly container throughput dipped but was 5.6% above 2024 levels by month-end. Capital Economics’ attributed the slower export growth partly to a higher base effect, cautioning that fading benefits from the US-China trade truce and Washington’s higher tariffs on rerouted goods could pressure exports further. HSBC analysts said the August slowdown had not yet fully reflected tariff shifts on other trading partners. China’s export growth continues despite domestic weakness in consumer demand and housing, with policymakers last September introducing supportive measures, including stock market support, as trade talks with the US proceed under an extended 90-day tariff truce.

|

15 participating countries |

20 chapters |

2.2 billion |

US$26.2 trillion |

28% |

| ASEAN member states, Australia, China, Japan, South Korea, New Zealand | trade in goods and services, investment, intellectual property, e-commerce, competition, SMEs, economic and technical cooperation, and government procurement | combined population, 30% world’s population | combined GDP, 30% global GDP | global trade (based on 2019 figures) |