CARI Captures Issue 746: Australian Prime Minister Anthony Albanese visits Brunei Darussalam and Malaysia

Captures has widened its scope to include news related to all the members of the Regional Comprehensive Economic Partnership (RCEP) agreement which was signed towards the end of 2020. Besides the ASEAN Member States, this includes Australia, New Zealand, China, Japan, and South Korea. The other weekly newsletters under CARI, China-ASEAN Monitor and Mekong Monitor will also be consolidated into the Captures newsletter. We hope this new version of Captures will serve you better and look forward to providing a curation of stories relevant to ASEAN and its trading partners.

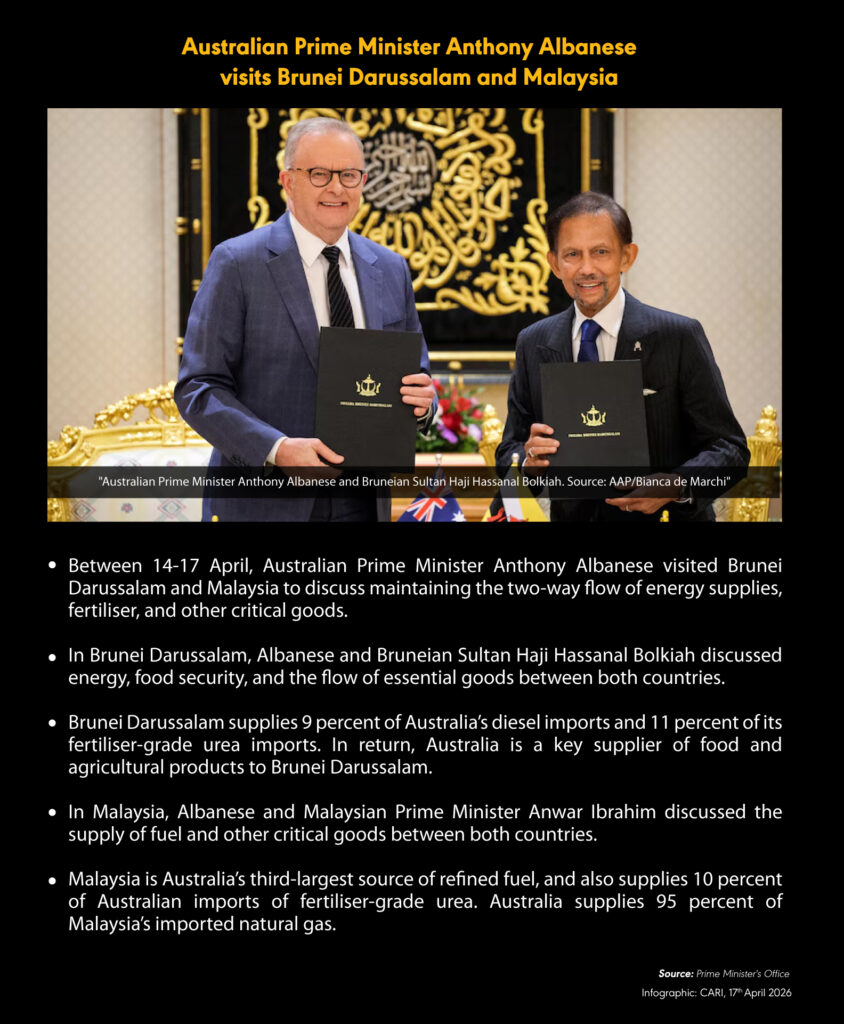

BRUNEI DARUSSALAM, MALAYSIA, AUSTRALIA

Australian Prime Minister Anthony Albanese visits Brunei Darussalam and Malaysia

(15 April 2026) Prime Minister Anthony Albanese travelled to Brunei Darussalam to secure urea supply amid disruptions caused by the Strait of Hormuz closure linked to conflict in the Middle East. Australia imports over two-thirds of its urea from the Middle East, with 65% sourced there in 2025. Albanese met Bruneian Sultan Haji Hassanal Bolkiah to discuss exchanging urea for Australian agricultural products and maintaining flows of fuel and key inputs. Brunei accounted for 11% of Australia’s urea imports and about 9% of diesel imports last year, positioning it as a key alternative supplier. Australia typically imports about 3.5 million tonnes of urea annually, but April shipments have fallen to 300,000 tonnes compared with 600,000 tonnes a year earlier, with only one vessel arriving from the Middle East. Import prices have risen sharply from about USD 700 per tonne in mid-February to more than USD 1,550 per tonne, more than doubling due to supply constraints. Following his trip to Brunei Darussalam, Albanese visited Malaysia, where he met with Malaysian Prime Minister Anwar Ibrahim. Anwar stated that Petronas will prioritise supplying excess fuel to Australia following discussions with Albanese on strengthening energy and agricultural trade. Anwar indicated domestic demand remains the priority, but confirmed assurances were obtained from Petronas to support Australia amid Middle East-related supply disruptions. Malaysia signalled interest in exchanging urea supplies to Australia for mineral phosphates sourced from Australia. Australia remains a key supplier of natural gas to Malaysia, accounting for about 20% of its domestic imports, alongside exports of wheat, lamb and beef.

MALAYSIA

Malaysia records 47% increase year-on-year in retrenchments in first quarter of 2026

(15 April 2026) Malaysia recorded 24,100 retrenchments in the first quarter of 2026, a 47% increase from about 16,500 in the same period of 2025, based on data from the Social Security Organisation analysed by Hong Leong Investment Bank. Layoffs peaked at 10,700 in January before declining to 7,500 in February and 5,900 in March, indicating an initial surge followed by moderation but still elevated levels overall. Manufacturing was identified as the most exposed sector due to reliance on global trade and external demand, with additional job losses in wholesale and retail trade and logistics. The bank characterised manufacturing as the “weakest link” in the labour market amid global economic uncertainty and geopolitical tensions. Retrenchments were concentrated in the Klang Valley, with Selangor accounting for 29.3% and Kuala Lumpur 25.6% of March layoffs, exceeding half of national totals. Kuala Lumpur’s share reached 38% in February, reflecting early impact of corporate restructuring in major urban centres. Outside the Klang Valley, Penang and Johor remained at higher risk due to dependence on export-oriented industries, including electrical and electronics and trade-linked sectors. Despite increased layoffs, the unemployment rate held at 2.9% for four consecutive months, according to the OpenDOSM Labour Market Dashboard. Job vacancies rose to about 107,000 in March, indicating continued hiring activity, particularly in services and construction. The contrast with 2025 reflects weaker manufacturing conditions and reduced semiconductor demand. Hong Leong Investment Bank assessed the retrenchment trend as part of an adjustment phase under uncertain global conditions and warned that export-driven sectors remain exposed to downside risks.

VIET NAM

Viet Nam and China signs multiple cooperation agreements during To Lam’s visit to Beijing

(15 April 2026) To Lam met Xi Jinping in Great Hall of the People on 15 April, marking Lam’s first overseas visit since assuming the presidency, and both sides signed multiple cooperation agreements without disclosed details. Lam identified relations with China as a “strategic priority” and “top priority”, calling for a shift from expanding trade volumes to deeper integration across development strategies, supply chains, production networks and infrastructure. The engagement reflects Viet Nam’s effort to strengthen ties with China while balancing its economic relationship with the United States, its main export market. Bilateral trade data shows Chinese exports to Vietnam rose 22.4% last year, with Viet Nam importing USD 198 billion in goods, while Chinese imports from Vietnam declined 0.7%, resulting in a trade deficit of nearly USD 100 billion for Hanoi. The discussions occur amid global trade disruptions linked to tariffs under Donald Trump and supply risks associated with halted shipping through the Strait of Hormuz due to the US-Israeli conflict with Iran. Viet Nam and China both rely on this route for oil imports, adding pressure to secure economic stability. Lam stated that geopolitical rivalry between the United States and China poses a constraint on Viet Nam’s target of achieving double-digit growth over the next five years.

VIET NAM, ITALY

Viet Nam and Italy call for expanding cooperation in trade and investments

(16 April 2026) The Italy–Vietnam Joint Commission on economic and trade cooperation, co-chaired by Italy’s Undersecretary of Foreign Affairs and Viet Nam’s Deputy Minister of Industry and Trade, focused on expanding collaboration in trade, industry, investment, energy transition and agriculture, including negotiations to open new product markets and enhance cooperation in mechanisation and food processing. Bilateral trade reached EUR 6.7 billion in 2025, an increase of 9.2% year-on-year, making Viet Nam Italy’s largest trading partner in ASEAN, while Italy remains Viet Nam’s third-largest partner within the EU. The Italian Undersecretary emphasised the need for balanced trade growth, stronger intellectual property protection and improved market access for Italian companies through continued dialogue to address sector-specific issues. A memorandum was signed for the Red River II project, financed by the Italian government with a EUR 2.86 million soft loan, aimed at improving management of the Red River hydroelectric basin through a monitoring and decision-support platform. The project includes new installations and upgrades to existing infrastructure across multiple sites to support energy system management.

INDONESIA, AUSTRALIA

Australia to import 250,000 tonnes of agricultural-grade urea from Indonesia

(16 April 2026) Australia will import 250,000 tonnes of agricultural-grade urea from Indonesia under a government-facilitated deal to offset supply disruptions linked to the Iran conflict. Incitec Pivot Fertilizers Ltd. will procure the volume from PT Pupuk Indonesia Holding Co., covering about 20% of Australia’s remaining urea requirements for the winter cropping season, including wheat, barley and canola. Incitec’s president stated the additional supply would help stabilise availability for farmers. Fertiliser prices in parts of Australia have doubled since the conflict, with around 60% of normal urea supply routes affected by the disruption of the Strait of Hormuz. Supply constraints have led some farmers to shift towards less fertiliser-intensive crops, potentially reducing wheat output. Indonesia reported a surplus of 1.5 million tonnes of urea, enabling exports, with interest also expressed by countries including India, the Philippines and Brazil.

THAILAND

Foreign investors flee Thai equities and bonds in March in largest outflow since October 2024

(16 April 2026) Foreign investors have reduced exposure to Thai assets following the Middle East conflict, with net equity outflows of USD 823 million and bond outflows of USD 705 million in March, marking the largest combined outflow since October 2024, reversing inflows of USD 1.7 billion recorded in February. The shift coincides with rising oil prices nearing USD 100 per barrel, increasing pressure on Thailand, which sources nearly half of its oil and gas from the Middle East. The economic outlook has weakened despite earlier optimism linked to the election of Prime Minister Anutin Charnvirakul, with analysts citing an energy shock as a near-term headwind. Thailand’s economy remains fragile, with growth at 2.4% last year and deflation preceding the conflict, while public debt stands at 66% of GDP, close to the 70% ceiling. Inflation is projected to rise to as much as 3.5% this year, compared to a 0.54% contraction in the first quarter. The central bank faces constrained policy options, with limited scope to tighten without harming growth or ease further due to inflation risks. Energy exposure is elevated, as over half of power generation relies on gas and increasing liquefied natural gas imports. The Thai baht has depreciated about 2.8% since the conflict began, although it has partially recovered following a ceasefire. Authorities have ruled out fuel subsidies but are absorbing costs to stabilise electricity tariffs, while concerns persist over fiscal limits and potential pressure to raise the debt ceiling. Analysts warn prolonged high energy prices could reduce consumption, weaken exports and tourism, and further strain economic recovery.

THE PHILIPPINES

Fuel prices in the Philippines more than double since Iran conflict began

(16 April 2026) Fuel prices in the Philippines have more than doubled since the Iran conflict began on 28 February, with over 90% reliance on Middle Eastern fuel exposing the economy to supply shocks and volatility. The Philippines’ Energy Secretary stated diesel prices may not return to 60 pesos per litre due to structural damage to Gulf oil facilities, indicating prolonged supply constraints and slower price declines. The blockade of the Strait of Hormuz has yet to fully impact supply, suggesting further price pressures. Economists assessed that sustained declines to pre-pandemic price levels are unlikely due to geopolitical risks and structurally higher energy costs, although recent oil price easing to about USD 96 per barrel and peso appreciation may moderate near-term inflation. Consumer groups criticised the government’s stance and called for stronger intervention, including tighter control over pump prices and reforms to the 1998 deregulation law, which limits price controls. Economists indicated direct price controls are not viable, recommending targeted subsidies, temporary tax relief, transport support and stricter monitoring instead. The government has introduced a subsidy of 10 pesos per litre, but concerns remain over its adequacy and implementation complexity. Proposals to remove fuel taxes, estimated at 22 to 25 pesos per litre for diesel, could provide immediate relief but would reduce fiscal revenues for social programmes. Analysts highlighted risks that persistently high fuel costs could sustain inflationary pressure and burden consumers, particularly in transport-dependent sectors.

RCEP Monitor

SOUTH KOREA

South Korea records record 4.76 million foreign tourist arrivals in first quarter of 2026

(16 April 2026) South Korea recorded 4.76 million foreign tourist arrivals in the first quarter of 2026, a 23% year-on-year increase and the highest first-quarter total on record, according to the Ministry of Culture, Sports and Tourism. March arrivals reached 2.06 million, up 27% from 1.61 million a year earlier, marking a new monthly record. Chinese visitors led with over 1.45 million arrivals, rising 29%, followed by Japan with 940,000 arrivals, up 20.2%, while Taiwan recorded the fastest growth at 540,000 visitors, up 37.7%. Long-haul markets including the United States and Europe contributed 690,000 visitors, increasing 17.1%. Cruise tourism expanded significantly, with 338 ship calls at ports such as Jeju, Busan and Incheon, up 52.9% year-on-year. Regional dispersion improved, with arrivals via regional airports rising 49.7% and the share of visitors travelling outside Seoul increasing to 34.5%, up 3.2 percentage points. Foreign card spending rose 23%, and visitor satisfaction reached 90.8 points. The upcoming BTS performance supports the revised 2026 target of 23 million visitors, up 21.4% from 18.94 million in 2025. Policy measures included expanded eligibility for five- and 10-year multiple-entry visas for nationals from 12 countries and an increase in automated immigration clearance coverage from 18 to 42 countries. Additional steps included expedited immigration screening for conference participants and coordination with Korea Railroad to improve regional access. Officials noted risks from rising airfares linked to higher fuel costs and uncertainty in global travel demand.

JAPAN

Japan pledges USD 10 billion in financial support for Asian countries amidst oil crisis

(16 April 2026) Japan pledged USD 10 billion in financial support to Asian countries, particularly in Southeast Asia, to secure crude oil and petroleum supplies amid disruptions linked to the Iran conflict. Prime Minister Sanae Takaichi announced the initiative following an online meeting with regional leaders, outlining a framework to support fuel procurement, maintain supply chains and expand stockpiles. The funding, equivalent to roughly one year of crude oil imports for Association of Southeast Asian Nations members, will be sourced from institutions including the Japan Bank for International Cooperation, Nippon Export and Investment Insurance, Japan International Cooperation Agency and the Asian Development Bank. The initiative was endorsed by leaders from countries including the Philippines, Malaysia, Singapore, Thailand, Viet Nam, Bangladesh and South Korea. The move responds to heightened regional vulnerability, with nearly 90% of oil and gas shipments through the Strait of Hormuz destined for Asia. Japan confirmed the plan would not affect domestic supply, noting reserves sufficient for 254 days of consumption, although 50 days of oil have already been released with a further 20 days planned. Concerns persist over potential shortages of naphtha, a key petrochemical used in medical supplies, which could affect healthcare systems. Regional governments have introduced conservation measures, while the Philippines declared a national energy emergency and President Ferdinand Marcos Jr called for activation of an ASEAN fuel-sharing mechanism.

NEW ZEALAND, AUSTRALIA

New Zealand and Australia impacted by fertilizer supply disruptions linked to Middle East conflict

(16 April 2026) Fertiliser supply disruptions linked to the Middle East war and China’s export restrictions are exposing reliance risks for New Zealand and Australia, both of which depend heavily on imported fertiliser for agricultural output and exports. Fertiliser production is concentrated in a small number of countries, with over 80% of countries importing at least 75% of their needs, increasing exposure to shocks in trade routes and supply chains. The Strait of Hormuz, which carries around a quarter of global seaborne oil, gas and fertiliser, is identified as a key vulnerability due to conflict-related disruption risks. Gulf states including Iran, Qatar and Saudi Arabia supplied 36% of global urea exports between 2023 and 2025, while China’s export restrictions have further tightened global availability. Rising natural gas prices have increased urea costs, contributing to higher food price pressures. International agencies, including the International Monetary Fund, International Energy Agency and World Bank, have warned that fertiliser market disruptions could threaten food security and increase inflation ahead of planting seasons. Industry and policy groups in Australia and New Zealand have called for fertiliser taskforces, strategic reserves and supplier diversification. Proposed alternatives include biofertilisers and local production of urea using green hydrogen, including projects such as the Kapuni initiative scheduled for 2027. Fertiliser price spikes following COVID-19 and the Russia-Ukraine conflict are cited as previous indicators of systemic vulnerability. Agricultural stakeholders argue that the absence of a coordinated national food and fertiliser strategy leaves both countries exposed to repeated supply shocks and rising costs.

|

15 participating countries |

20 chapters |

2.2 billion |

US$26.2 trillion |

28% |

| ASEAN member states, Australia, China, Japan, South Korea, New Zealand | trade in goods and services, investment, intellectual property, e-commerce, competition, SMEs, economic and technical cooperation, and government procurement | combined population, 30% world’s population | combined GDP, 30% global GDP | global trade (based on 2019 figures) |