CARI Captures Issue 744: Southeast Asia faces looming fertiliser shortages amidst Iran war

Captures has widened its scope to include news related to all the members of the Regional Comprehensive Economic Partnership (RCEP) agreement which was signed towards the end of 2020. Besides the ASEAN Member States, this includes Australia, New Zealand, China, Japan, and South Korea. The other weekly newsletters under CARI, China-ASEAN Monitor and Mekong Monitor will also be consolidated into the Captures newsletter. We hope this new version of Captures will serve you better and look forward to providing a curation of stories relevant to ASEAN and its trading partners.

ASEAN

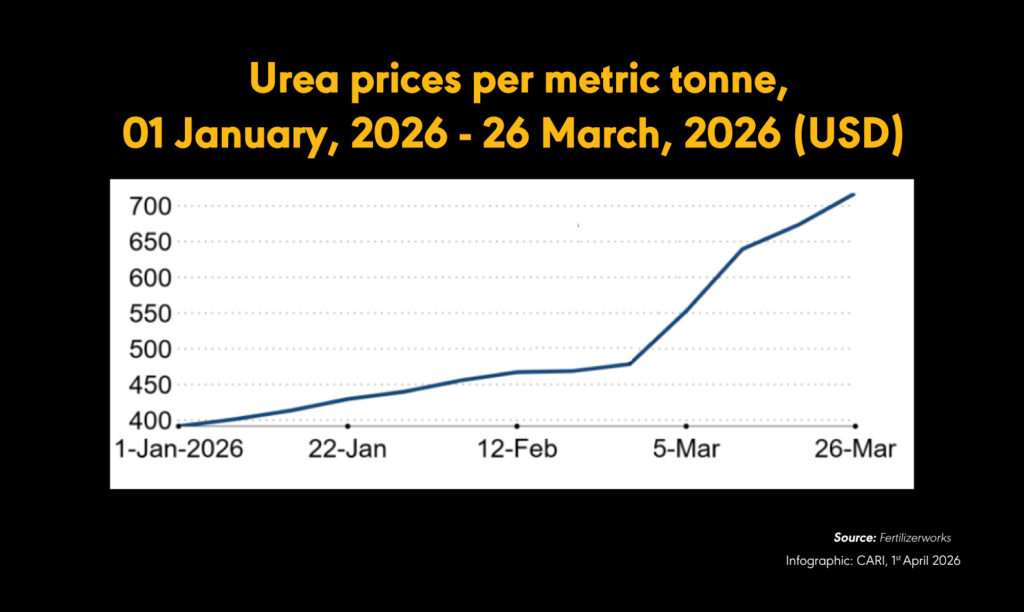

Southeast Asia faces looming fertiliser shortages amidst Iran war

(31 March 2026) Southeast Asia faces rising risks of fertiliser shortages and price increases due to disruptions in the Strait of Hormuz, with over 20 vessels carrying nearly one million metric tonnes of fertiliser reportedly stranded, constraining regional supply. The crisis centres on urea, a key nitrogen fertiliser, whose price has risen 83% year to date and 50% since late February to USD 717.74 per tonne, with the Persian Gulf accounting for 30%–35% of global exports and natural gas representing 60%–90% of production costs. International Fertilizer Association indicated that while price impacts are evident, prolonged disruption could lead to physical shortages. China’s export restrictions have further tightened global supply. Exposure varies across Southeast Asia, with Thailand highly dependent on imports, sourcing 1.8 million tonnes or 55% of nitrogen raw materials from the Middle East in 2025, and holding sufficient stocks only until August 2026. Countries with domestic production capacity, including Indonesia, Malaysia and Viet Nam, are relatively more insulated, though supply constraints persist at the firm level, with Indonesian producer Saraswanti Anugerah Makmur reporting only 45 days of urea inventory. Concerns were raised over potential export prioritisation by state producer Pupuk Indonesia, with calls for export controls to secure domestic supply. Supply risks may escalate if Gulf production facilities halt operations due to storage constraints, prolonging disruption even if trade routes reopen. High fertiliser prices are expected to impact agricultural sectors unevenly, with stronger resilience in oil palm plantations due to elevated palm oil prices, while crops such as rubber, coffee, sugar and cocoa face greater pressure. Continued price volatility may also distort purchasing behaviour, delaying procurement and potentially reducing crop yields due to missed application cycles.

MALAYSIA

Bank Negara Malaysia indicates no immediate requirement for economic stimulus

(31 March 2026) Bank Negara Malaysia indicated no immediate requirement for a broad economic stimulus package despite the ongoing West Asia conflict. BNM’s governor stated that economic support should be holistic and targeted rather than broad-based, based on an assessment of overall economic conditions. He noted that Malaysia is entering the year from a position of strength following recovery from multiple crises, particularly the COVID-19 pandemic. Existing post-pandemic support measures, which are largely targeted, remain in place. The banking sector is prepared to assist borrowers, corporates, and SMEs facing financial difficulties. The government continues to obtain sectoral input through the National Economic Action Council (MTEN) to assess needs. This approach enables authorities to form a comprehensive view of economic conditions and direct assistance to priority areas. The governor emphasised that support cannot be applied broadly across sectors and must instead reflect a holistic and targeted framework.

INDONESIA

Indonesian business lobby calls for temporary higher deficit cap to address energy crisis

(31 March 2026) The Indonesian Chamber of Commerce and Industry called for temporary policy measures to address rising energy costs, including lifting the fiscal deficit cap, implementing work-from-home arrangements and sourcing oil from alternative suppliers such as Russia. The chamber’s chairman proposed raising the deficit ceiling above the statutory 3% of GDP to 4%–5% for three to six months to sustain at least 5% economic growth, as crude oil prices exceed USD 100 per barrel versus the USD 70 assumption in the 2026 budget. The Organisation for Economic Co-operation and Development revised Indonesia’s 2026 growth forecast to 4.8% from 5% and projected inflation at 3.4% compared with 1.6% previously. Moody’s Ratings and Fitch Ratings had earlier downgraded the sovereign outlook to negative, citing fiscal risks and policy uncertainty linked to government programmes. The chamber stated these assessments predated the Iran war and argued that temporary fiscal expansion would be understood under current conditions. The government has yet to confirm a deficit increase after retracting a 13 March proposal, maintaining a cautious approach focused on budget efficiency measures without detailing fuel pricing or broader interventions. Indonesia imports approximately one-third of its oil, with around 20% routed via the Strait of Hormuz, and holds less than 30 days of supply, increasing vulnerability to disruptions. The chamber indicated the need to diversify oil sourcing, including from Russia and the United States, to ensure supply stability. He characterised the government’s response as measured despite limited policy announcements relative to regional peers. Longer term, they expect the crisis to accelerate investment in more resilient energy systems, including renewables and electric vehicles, with discussions ongoing on potential incentives to support EV adoption.

INDONESIA

Indonesia to proceed with B50 biodiesel mix in 2026 amidst energy supply disruptions

(30 March 2026) Indonesia’s President Prabowo Subianto stated during an official visit to Japan that the country will proceed in 2026 with its B50 palm oil-based biodiesel programme. He confirmed at a business forum ahead of a meeting with Sanae Takaichi that Indonesia will increase the palm oil content in diesel from 40% to 50% this year. The B50 blend consists of 50% palm oil-based biodiesel and 50% conventional diesel. Authorities had previously scrapped the B50 rollout in January due to technical and funding constraints, maintaining the B40 blend instead. The policy shift indicates a reversal of that decision within the same year. The move follows discussions to revive the programme amid energy supply disruptions linked to the U.S.-Israeli war on Iran.

THAILAND

Bank of Thailand signals wait-and-see monetary policy amidst oil shock

(31 March 2026) The Bank of Thailand signalled a wait-and-see monetary policy stance, stating that interest-rate cuts are unlikely to address supply-driven energy shocks linked to Middle East tensions. The Bank of Thailand’s Assistant Governor said monetary policy is a demand-side tool and may not effectively manage oil-driven inflation, with targeted fiscal and regulatory measures viewed as more appropriate. The central bank indicated it is unlikely to ease policy further following a February rate cut, while leaving open the possibility of tightening if inflation proves persistent. Headline inflation is projected to return to the 1%–3% target range earlier than expected due to rising oil prices and supply disruptions, despite prices having remained negative for 11 consecutive months. Thailand remains highly exposed to energy shocks, with over half of oil imports sourced from the Middle East, including shipments through the Strait of Hormuz. Rising energy and logistics costs are creating downside risks to growth, affecting tourism and exports. Early indicators show weakening business sentiment in March, declining airport arrivals and reduced shipping volumes. The baht has depreciated 6% this month, marking its largest monthly decline in three years, with further weakness expected due to higher energy import costs and dividend repatriation. The government is preparing measures to mitigate rising fuel costs, including fuel excise tax cuts, increased welfare stipends and targeted fuel subsidies.

THE PHILIPPINES

The Philippines increases petroleum stockpile to 50.94 days as of 27 March

(30 March 2026) The Philippines increased its petroleum stockpile to 50.94 days as of 27 March, up from 45 days, according to the Philippines’ Energy Secretary. The inventory expansion includes gasoline, diesel and jet fuel, supported by procurement efforts from the Philippine National Oil Company. Recent deliveries include 142,000 barrels of diesel from Japan, with a further 900,000 barrels expected from Malaysia, Singapore, India and Oman. The government is actively seeking alternative suppliers outside the Middle East, including Colombia, Argentina, Canada and the United States. The Philippines, which relies heavily on Middle Eastern oil imports, is responding to supply disruptions linked to the ongoing war in Iran and has declared a national energy emergency. Petron Corp. has procured 2.48 million barrels of crude from Russia and may increase purchases if the conflict persists. These purchases were enabled by a US waiver permitting imports of Russian crude until 12 April. Additional supply signals include diesel and fuel cargoes exported by China to Southeast Asia over the weekend. The government stated that securing sufficient energy supply remains the primary objective.

VIET NAM

International shipping rates could increase by up to 80% due to Middle East conflict

(02 April 2026) Viet Nam’s international shipping rates could increase by 50% to 80% due to Middle East tensions disrupting supply chains, according to the Vietnam Maritime and Waterway Administration. Marine fuel prices have risen to USD 1,100–2,000 per tonne from USD 550–750 previously, with fuel accounting for 30%–40% of total shipping costs, prompting carriers to adjust freight rates. The increase in logistics costs is expected to raise import-export prices and weaken Viet Nam’s competitive position. Authorities have proposed stricter oversight of pricing and surcharges, alongside coordination with carriers to stabilise transport capacity and limit excessive price increases. Domestic container transport costs have risen by 7%–12% since mid-March. Rates on the Hai Phong to Ho Chi Minh City route have reached up to VND 2.8 million per 20-foot container and VND 5.3 million per 40-foot container, with higher pricing on return trips.

RCEP Monitor

CHINA

Chinese equities increasingly viewed as safe haven amidst Iran war

(31 March 2026) Chinese equities are increasingly viewed as a relative safe haven amid deteriorating global risk sentiment linked to the Middle East conflict and disruption to the Strait of Hormuz, which affects roughly one-fifth of global oil and gas flows and has driven a surge in crude prices. J.P. Morgan identified China as its most preferred regional market, citing low reliance on Gulf energy and strong fiscal support capacity. HSBC maintained an “overweight” stance, highlighting defensive characteristics supported by a predominantly domestic investor base and currency stability. China’s Shanghai Composite Index declined 6% in March, outperforming regional peers including South Korea’s market, which fell 18%, and Japan’s Nikkei, which dropped about 13%. BNP Paribas strategists expect China’s relative outperformance in Asia to strengthen if the conflict persists. Goldman Sachs stated that China is better positioned than several global peers to absorb the oil supply shock, supported by long-term energy diversification, expanding strategic oil reserves, and access to non-Middle East supply sources.

CHINA

Top Chinese airlines signal caution outlook for 2026 amidst rise in jet fuel prices

(31 March 2026) China’s three largest state-owned airlines, Air China, China Eastern Airlines and China Southern Airlines, signalled caution for 2026 as the Iran war drives a sharp rise in jet fuel prices and weakens industry outlook. All three carriers returned to losses in the fourth quarter of 2025, with China Eastern reporting a CNY 3.7 billion loss, Air China CNY 3.64 billion, and China Southern CNY 1.3 billion despite achieving a full-year profit. The airlines cited persistent geopolitical risks and weak global economic momentum, alongside domestic challenges including overcapacity, intensified competition, and pricing pressure from high-speed rail. Passenger volumes increased, but falling ticket prices constrained revenue growth. International operations remained a key revenue driver, with 2025 international passenger traffic rising 22.7% for China Eastern, 19.6% for China Southern, and 15% for Air China, although fourth-quarter capacity cuts to Japan and refund policies weighed on performance. Industry data showed a record 94 million passengers during the 40-day Spring Festival travel period in early 2026, up 4.7% year on year, but analysts warned rising fuel costs could offset demand gains. Jet fuel prices have more than doubled since February, threatening earlier global airline profit forecasts of USD 41 billion for 2026 and forcing network adjustments. Fuel accounted for 35% to 38% of operating costs in the first half of 2025, and China’s lagged fuel surcharge mechanism is unlikely to fully offset rising costs, compressing margins. Only China Eastern implemented fuel hedging in 2025, holding 500,000 barrels in hedged positions expiring in 2026, with a 5% fuel price movement estimated to impact profit by CNY 2.2 billion. Analysts expect deeper sector losses in 2026 before a recovery in 2027. Fleet expansion continues with deliveries of COMAC C919 jets, with China Southern raising its 2026 delivery target to 13 aircraft while China Eastern and Air China each maintain projections of 10.

SOUTH KOREA

South Korea to permit domestic oil refiners to swap crude supply from national reserve

(31 March 2026) South Korea will implement a policy permitting domestic oil refiners to swap crude supply from the national reserve, according to an industry ministry spokesperson on 31 March. The policy allows refiners to borrow crude oil from the reserve and return an equivalent volume once overseas shipments arrive. The measure was initially reported by Yonhap News Agency. The industry ministry stated that no disruption to national crude supply is expected before June. Local refiners have secured over 20 million barrels of crude oil for delivery by end-June. This figure was cited by YTN based on comments from a senior Industry Ministry official.

|

15 participating countries |

20 chapters |

2.2 billion |

US$26.2 trillion |

28% |

| ASEAN member states, Australia, China, Japan, South Korea, New Zealand | trade in goods and services, investment, intellectual property, e-commerce, competition, SMEs, economic and technical cooperation, and government procurement | combined population, 30% world’s population | combined GDP, 30% global GDP | global trade (based on 2019 figures) |