Originally published in Advancing ASEAN in the Digital Age Book, 14 November 2017.

Getting E-FIT: From Workforce to Thinkforce

ASEAN has much to celebrate on its 50th birthday – it is the fifth largest economy worldwide1; and it has raised its citizens’ standards of living steadily in a largely peaceful environment. ASEAN’s success has been built on strong fundamentals. With the world’s third largest work force, and globally competitive wages, ASEAN has benefited greatly from the diffusion of technology and the migration of work to the most efficient locations. However, fundamental changes in the paradigm of global competitiveness are afoot. The advantage of low labor costs is being eroded by technological advances such as natural language processing, machine learning, big data analytics, and connectivity between humans and machines. In order to make the next 50 years just as celebration-worthy, ASEAN will need to rely on more diverse pillars of growth capitalising on technology.

In fact, the future is here already. There are Chinese clothing manufacturers opening factories manned by robots (and some human supervisors) in Arkansas, USA – much closer to US markets than competitors in ASEAN. Automation is not limited to manufacturing – Amazon and Alibaba have launched cashier-free stores. About four of every five Wall Street firms have already implemented, or plan to use, some form of AI2, and some law firms are automating client name checking and document drafting.

Looking ahead, the changes in the nature of work require ASEAN to transform its workforce into the world’s third largest “think force”. To do this, ASEAN needs to get “E-FIT”, improving its education, finance, infrastructure and technology.

Education

The transformation from workforce to thinkforce starts with education.

ASEAN needs to continue to improve its compulsory education (i.e., up to 15 years old). In OECD’s PISA, Singapore was #1 across science, reading and mathematics, and encouragingly, Vietnam was #8 in science, and average on reading and mathematics. Thailand and Indonesia were below the OECD average in all 3 areas, and other ASEAN countries were not covered.

The future challenges extend to higher education. In terms of researchers per million of population3, Singapore ranks #6 worldwide, Malaysia #37, while Indonesia, the Philippines, Thailand and Vietnam rank below #50. Ranking in research foretells levels of innovation. For example, Singapore leads ASEAN ranking at #13 in patent applications per million of population4, Malaysia next at #36, while Indonesia, the Philippines, Thailand and Vietnam rank below #70.

Even if students do not work in laboratories upon graduation, education in science and mathematics is important as they build skills that allow humans to interface with and improve the functions of machines. These skills include problem solving, critical thinking, interpretation and openness towards new ideas, and the willingness to challenge old ideas. Education that strengthens communication and develops relationship skills will also be needed.

Improving on all those fronts will require greater investments in education – private and public, for-profit and charitable – and in every stage of a child’s life, from early childhood development, through to compulsory education and higher education. It also requires opening up the playing field for different parties to participate and new modes of individualized learning taking advantage of mobile technology.

Finance

The financial industry is not only one of the largest employers of skilled workers; its development also attracts capital and funds long-term investments.

While ASEAN’s savings rates are generally high, most savings are in cash, bank deposits or property. Capital markets (stocks, bonds and money markets) are critical to channel the savings into long-term productive investments. These include physical infrastructure (such as transport and communications), social infrastructure (such as schools and hospitals), and funds to grow business and industry, including new ventures.

ASEAN’s capital markets are less mature relative to developed economies. The ratio of floated book value of equity and bonds outstanding to GDP – a measure of capital markets maturity – was only 34 percent in Indonesia, 36 percent in Vietnam and 65 percent in the Philippines in 2016. The same ratio was 262 percent in the US and UK, 282 percent in Japan and 191 percent in South Korea5.

Long-term planning from the government and concerted, multi-year effort from both private and public stakeholders are required to speed-up capital markets development, from establishing benchmark assets, promoting a deep and broad investor base, encouraging issuance, to setting transparent rules and friendly taxation policies. This will allow ASEAN to attract capital, support development and enable all aspects of the economy to flourish.

Interconnectivity for Competitiveness

Strengthening intra-region infrastructure and interconnectivity will lower production costs, create a larger market, and encourage inward investments in supply chains. Closing the infrastructure gap through public and private efforts will be critical in information connectivity. This includes not only ports, rail, roads and power but also telecommunications and data. In 2016, only 40 percent of ASEAN’s population had internet access6.

Strengthening interconnectivity in ASEAN is not just about infrastructure. It also requires increasing commitment to remove trade barriers and frictions. Doing so is estimated to increase GDP by 9.3 percent7. This will boost ASEAN’s share of global trade – critical as both total merchandise export and inflow of foreign direct investment peaked in 20148. Although work is underway to address issues such as non-tariff barriers, customs procedures and trade facilitation, standards harmonization and intellectual property rights protection, speedier integration across the region are needed to stay competitive.

Technology

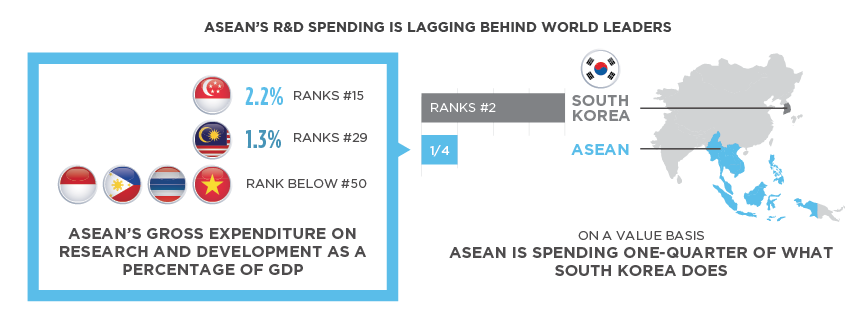

Innovation and the digital economy are driven by research and technological breakthroughs. However, ASEAN’s gross expenditure on research and development (R&D) as a percentage of GDP is low9. While Singapore ranks #15 with 2.2 percent and Malaysia #29 with 1.3 percent, Indonesia, the Philippines, Thailand and Vietnam rank below #50. On a value basis, these six ASEAN countries are spending just one-quarter of what South Korea (ranked #2) does and roughly the same as Israel (ranked #1).

ASEAN only received 1.5 percent of the global total [new venture funding], less than the amount received by Israel, which has just 1 percent of ASEAN’s population and just one-eighth of ASEAN’s GDP.

Another measure to consider is new venture funding (including angel, venture capital and corporate venture capital funding). While venture funding for Asia increased dramatically from US$9.5B or 6 percent of the global total in 2012 to US$98B or 28 percent in 201610, this was dominated by China. ASEAN only received 1.5 percent of the global total, less than the amount received by Israel, which has just 1 percent of ASEAN’s population and just one-eighth of ASEAN’s GDP. Today, Israel has the third most companies listed on the tech-focused NASDAQ stock exchange after the US and China11.

Both increasing the level of R&D investments and coordinating and concentrating the spending is key to innovation of new technology. This means ASEAN should work on policies to encourage investment, whether domestically or by foreign companies, and also develop an overarching strategy to create the interrelationships among global technology companies, local education and research institutions, and government resources and incentives.

Conclusion

ASEAN has made exceptional progress in its first 50 years, but it must become an innovation center and equip its people to compete effectively in the digital economy. With continued focus on becoming E-FIT – improving education, developing financial markets to mobilise long-term capital, building inter-connectivity and investing in technology and research — ASEAN can fulfill its potential and become a leading source of global growth in the next decade.

1 “GDP (current US$)”, World Bank (as of 12 Oct 2017). ASEAN #5 after US, EU, China and Japan

2 Greenwich Associates

3 Global Innovation Index 2017

4 The World Economic Forum Global Competitiveness Index 2016

5 Floated book value from Bloomberg; Bonds outstanding from Asia Bonds Monitor

6 ITU 2016 statistics ”Percentage of Individuals using the Internet”

7 “Enabling Trade Valuing Growth Opportunities”, World Economic Forum, 2013

8 ASEANStats as of 30 June 2017

9 Global Innovation Index 2017

10 CB Insights. Only has data for 8 ASEAN countries: Cambodia, Indonesia, Malaysia, Myanmar, the Philippines, Singapore, Thailand and Vietnam

11 “Israel is a tech titan. These 5 charts explain its startup success”, The World Economic Forum. 19 May 2017

![]() Download Advancing ASEAN in the Digital Age e-book

Download Advancing ASEAN in the Digital Age e-book

About Donald Kanak