Trump’s America and the Asian Spillover

Summary

With the upcoming Trump presidency and Republican control of the House and Senate, this article looks at the possible changes to US policy and how that might affect Asia. It focuses on fiscal, trade, and foreign policy and, as a corollary, how that may affect monetary policy. It is safe to say, there is tremendous uncertainty now and most commentators are guessing just how much of Mr. Trump’s campaign promises will be implemented.

My view is that the first half of next year could be particularly difficult for Asia as tax cuts boost US consumption and hence put upward pressure on inflation and hence bond yields. However, Asian exports do not benefit much as they are more reliant on US investment demand. So, there is a limited trade boost for Asia but they must deal with the consequences of higher rates abroad and a stronger dollar. Expected rate cuts in Indonesia and Malaysia may get delayed and moderated, while nearly all Asian currencies may have to deal with both volatility and weakness.

Over the medium term, as US spending on infrastructure kicks in, and perhaps crowds in private capital, Asia will benefit. Of course, that assumes (or at least hopes) that the US and China are not in a trade war at that moment for that is unambiguously negative for not only Asia, but also for those two countries.

The US fiscal deficit is likely to get bigger, inflation is likely to creep up and the Fed may get more aggressive in the second half of the year. That would put some pressure on Asia not only via higher rates but also a stronger US dollar. But, as that scenario will likely come with higher Asian export growth, the region should be well prepared to deal with these external changes.

New Realities

The short term market reaction to the upcoming Trump presidency and Republican control of both the House and Senate has been pro-growth in the US but more mixed abroad. In the US, equity markets have rallied, bonds have sold off, and the USD has strengthened. Industrial commodities, such as copper have recovered, possibly in the hope of more construction activity while oil has sold off due to fears of greater supply.

Moreover, in the US, based on expectations of future policy the markets have been discerning. For example, financial stocks have picked up in part due to a steepening yield curve and possibly, in part, due to expectations of changes in regulation. Technology stocks have lost ground; this is perhaps due to fear of tariffs disrupting supply chains or the fear of being able to outsource less easily or impediments to international hiring.

Emerging markets have shown no such selectivity. Equities, bonds, and currencies have all sold off. A variety of fears are plaguing ASEAN markets, the greatest of which is the future US relationship with China. Indeed, over the medium term, three areas will merit more focused attention: US fiscal policy, trade policy and foreign policy. A corollary of this would be the conduct of US monetary policy if there are significant shifts in other policy areas.

The Medium – Term Outlook

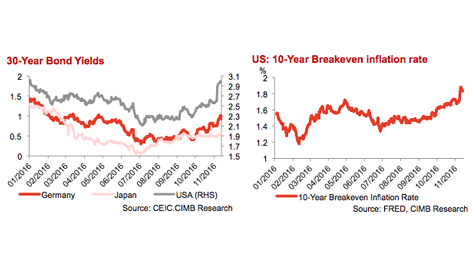

There is an ongoing re-pricing of the US macroeconomic outlook. Clearly, growth and inflation are both expected to rise. To be sure, the markets had been expecting this for some time – the yield on the 30-year Treasury bill has been rising since July as has the breakeven inflation rate in the US – but the elections have accentuated it.

To some extent, the outlook is being driven by policy expectations, so let us consider each policy initiative in turn:

Fiscal policy. Mr. Trump has promised to invest in infrastructure, about $500 billion over 5 years1. While this would undoubtedly benefit Asian exports, three details are important. First, it will depend crucially on where the money is spent; second, on how it is financed; and third, what reforms are done on the revenue side.

With regards to the sphere of spending, if expenditure takes place in areas such as roads, bridges, or air transport, it not only would directly boost Asian exports but also would help crowd in private investment providing a further impetus to Asian trade. As most of Asian trade is in intermediate goods catering to investment abroad, the benefits are obvious.

Besides that, it would provide a boost to supply chains and that should get trade multipliers going. All very good.

The second detail is about how this expenditure is likely to be financed. If tax reform – a drop in the corporate tax rate – will get enough funds to be repatriated to finance the stimulus, then well and fine. If, however, the hope is that policy measures will suddenly get the US economy growing at 4% or more, then there is likely to be not only disappointment, but also higher deficits.

Moreover, a 4% plus growth rate achieved through pure demand-side measures, without a commensurate improvement on the supply side, would mean overheating and would likely be met by higher rates. Ultimately, it would be unsustainable2.

A couple of years ago, when there were significant unemployed resources in the economy, a rising fiscal deficit did not necessarily mean higher inflationary expectations and hence higher yields. But today, with the economy near full employment, the outcome is likely to be different.

Third, on the revenue side, Mr. Trump has signaled that he would like to cut the marginal tax rate for both individuals and corporations. History suggests revenue as a percentage of GDP is likely to decline, resulting in higher deficits. The effect of the cuts will be stimulative; the extent of the effect will depend on the magnitude and incidence of the cuts. The greater the income boost to individuals with a higher propensity to consume, the greater the stimulative impact.

In summary, Mr. Trump’s fiscal plans should provide much needed stimulus from the second half of 2017 and should add to GDP growth. The extent of improvement is difficult to predict at this stage. However, it will also result in tighter monetary conditions, via both higher rates and a stronger dollar.

For Asian economies, a boost to US growth is undoubtedly positive to the extent that it helps exports. The larger boost to trade would come via infrastructure spending given the nature of Asia’s exports to the US. While a rise in US consumption is welcome, it is not the main driver of Asia’s exports.

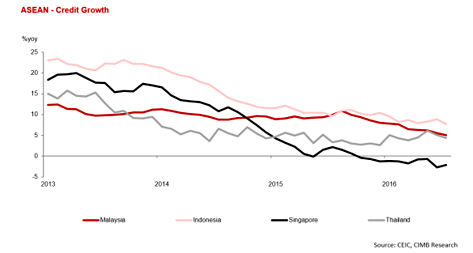

On the negative side, higher US rates will mean an end to rate cutting cycles that we have across Asia, notably in Indonesia, and a possible rise in longer term rates. That will have a contractionary effect on the economy but perhaps not significantly so as credit growth across many ASEAN countries had been poor to begin with. Countries with high household debt, such as Malaysia and Thailand, will probably feel the larger impact of higher longer-term rates.

A stronger dollar, especially if it is versus the Renminbi, will mean weaker ASEAN currencies. However, if they all weaken in tandem and trade-weighted impact is likely to much less. As such, the impact on trade, strictly due to currency moves, is unlikely to be great. Moreover, as most ASEAN countries have low dollar-denominated short-term debt, it should not meaningfully impact the external accounts either. Of course, all this depends on the magnitude of the various price movements and that, in turn, is likely to be more driven by Mr. Trump’s trade policy.

Trade policy. The hope for ASEAN is that Mr. Trump will not follow through on most his proposed changes to US trade policy. The most important ones are: The Trans Pacific Partnership (TPP) – labeled a “disaster” by Mr Trump; the second is the threat of tariffs on Chinese exports, ranging from between 25% to 45%, made in various speeches; and the third is his plan to label China a currency manipulator. All 3 measures would be negative for the region, though in differing degrees. Consider them in turn.

Labeling China a currency manipulator would be largely benign. First, very few people think China has an undervalued currency — it is, in fact, bleeding capital — so it’s a label that wouldn’t be taken seriously. Second, all it means is that the US Treasury would start having a dialogue with the Chinese authorities about revaluing the currency. It is a safe bet that the dialogue would not go very far. The larger issue is the negative signal it would send on US-China relations and the uncertainty that would cast on markets.

Although, abandoning the TPP would have negative implications, it would be losing something that ASEAN didn’t have anyway so the loss would be more of possible, rather than actual, benefits. Countries such as Vietnam, which would gain most from integration, have the largest potential loss. As such, market-driven variables are unlikely to respond. It could, however, recast relationships within the region. The TPP was an important part of President Obama’s “pivot” to Asia, in terms of building strategic and military alliances, that effort will undoubtedly come under strain.

Moreover, it is very likely that most Asian countries will tilt more strongly toward the Regional Comprehensive Economic Partnership (RCEP) that includes all ASEAN nations, China, Japan, India, Korea, Australia and New Zealand. It could potentially alter relationships within Asia and how ASEAN relates to China versus the US.

Tariffs on Chinese products could be a game changer for the global economy. Such tariffs would disrupt supply chains that have been functioning for many years and the effects would be felt all over ASEAN. We don’t know what the China’s response is likely to be, though it’s safe to say any response is unlikely to be positive. Retaliation would be almost certain.

The stated reason for the tariffs is that they would benefit the US worker but, in truth, that is not sure. Most likely some other country would replace China as the exporter to the US. What is true, is that the cost of US imported goods will rise, thereby imposing an implicit tax on US consumers and businesses, and the effect of Mr. Trump’s tax plan would be diluted. Furthermore, protectionism will constrain the growth of world income and that includes the US.

Tariffs would also lead to further rise in the US dollar and weakness in the RMB, both of which would have a negative impact on Asian currencies. Over the medium term, potential growth will suffer as efficiency gains from trade are lost. The countries that will feel the most pain are the ones that rely on open international markets to sell their products, and that includes almost all of ASEAN.

The monetary policy response. We are already seeing the market impact of an expected fiscal stimulus, higher expected growth and inflation, and possibly higher fiscal deficits: Yields on 10-year US treasuries have risen (yields on 30-year bonds have been rising since July), the USD is stronger and the breakeven inflation rate (the difference between the yield of a nominal bond and the yield of inflation-indexed bond – TIPS — of similar maturity), which started rising in July, has risen further. Will the US monetary policy outlook change? And what will be the Asian response?

In my view, any change in US Fed Funds glide path is likely to be minor, that is unless policy changes turn out to be much greater than I think. For starters, the consensus view has the Fed would raising rates once this December and probably another 2 times next year. In short, a shallow glide path for the Fed Funds rate is expected in what is believed to be a low growth, low inflation, and low rates world.

Some of that will change with fiscal stimulus, especially if it is large enough and sustained enough, being applied in an economy that is near full employment. But that time has yet to come. Meanwhile, there is still uncertainty about the current state of the economy and the case for a rate increase is hardly cut and dried. Indeed, while there is possibly incipient inflationary pressure – wages grew 2.8% yoy in October – the markets, with higher yields and a stronger dollar, may already have done the initial tightening for the Fed. And given the uncertainty about policy, the Fed may choose to hold back in December and see what unfolds.

Over the medium term though, rates should rise a bit more aggressively. But fiscal policy takes time to have an effect, and monetary policy is unlikely to work at cross purposes, so rate increases are probably more likely to be in the second half of the year and into 2018 rather than being imminent. The Fed needs to get inflation back in the system and even though the breakeven inflation rate has risen, it is still below the Fed’s target.

As such, I think the Fed may desist for a while and there is possibly only one rate hike of 25 bps until the middle of 2017 and perhaps two more after that until the end of the year. In 2018, there will be another wildcard as the Fed Chair is likely to change, possibly to someone more hawkish. With fiscal stimulus starting to show a greater effect, and hopefully trade policy not being too contractionary, another 3 rate increases of 25 bps each can be expected that year.

Looser fiscal policy in tandem with tighter monetary policy makes a textbook case for a stronger dollar and that is what I expect over 2017.

For ASEAN, it means we are possibly nearing the end of a rate cutting cycle. Monetary policy is not just about the Fed, but also about domestic economies, and how respective currencies are behaving and the signal that sends about overall stability. Bank Indonesia has cut rates 6 times this year and I had expected another 2 or 3 more cuts next year. Depending on rupiah (in)stability, and how aggressively the Fed moves, there may now be fewer cuts, but I don’t believe that the cutting cycle is fully over for Bank Indonesia.

I had also expected BNM to cut rates at their next meeting on November 23rd, but given the recent volatility of the ringgit, that cut might be put on the back burner. I emphasize that I think it is on the back burner, rather than off the table, as I believe that, given the opportunity, BNM will cut again. Depending on how the ringgit behaves, we could get one or two cuts in the first half of next year. After that, when the glide path of the Fed Funds rate becomes steeper, Malaysian rates are likely to stay stable.

Currency volatility is damped in Thailand because of the buffer of a large current account surplus. Moreover, policy rates have been steady despite low inflation, as the transmission mechanism is impaired and credit growth remains poor. I had believed that rates could have been modestly reduced next year once fiscal policy gained traction and monetary policy became more effective. That cut may be off the table if we start seeing an improvement in the external sector.

The Singaporean economy is highly reliant on trade and financial flows. Mr. Trump’s policies will not help it. Nonetheless, with monetary policy settings at neutral I do not expect a change. The SGD will probably bear the brunt of the adjustment and weaken along with other regional currencies.

Foreign Policy. If the TPP is scrapped, it would be a dilution of Mr. Obama’s pivot toward Asia and possibly portends an ASEAN pivot toward China. We have already seen the Philippines go that route and Malaysia too has been strengthening its bilateral relationship with China. Of course, relationships with China and the US are not mutually exclusive, but it looks possible that Mr. Trump may not be as engaged with the region as his predecessor.

There are, of course, larger issues such as the US relationship with its NATO allies, the relationship with Russia and opposition to the Russian position on Crimea, Ukraine and Syria, the continued presence of US troops in countries such as Japan and Korea, and possibly even nuclear proliferation. Time alone will answer how much of Mr. Trump’s campaign rhetoric will actually come to pass. In the meanwhile, there is uncertainty, higher risk premiums and volatility.

1 At current GDP, this is about 0.5% of GDP a year. In our view, the needs are greater not only from an infrastructure perspective but also in terms of a stimulus. That said, I welcome this initiative. I have, for some time now, believed that fiscal stimulus (not just in the US, but worldwide) as the most likely effective measure to get growth out of its slump.

2 Potential growth in US is currently measured at around 1.5%to 1.6%. FRED Economic Data.