Thailand: Macro snapshot

HIGHLIGHTS

Macro snapshot

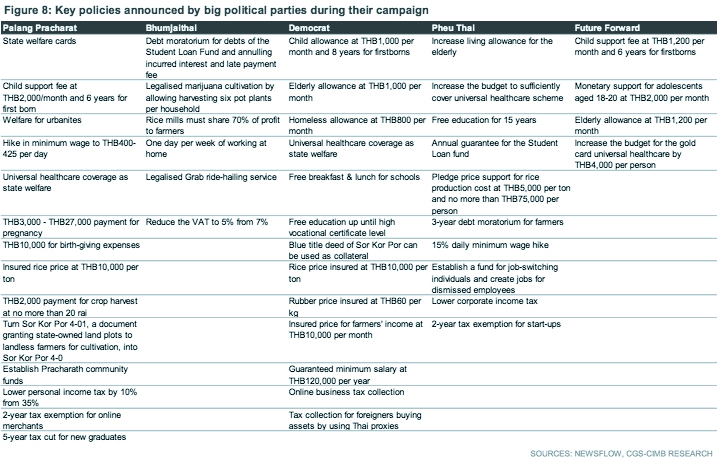

- Thailand’s trade balance came in healthier at a surplus of US$3.5bn in February as a result of a sharp contraction in imports

- Better-than-expected election results for pro-junta coalition raises likelihood of pro-poor policies and continuity of key projects like EEC and SEC

- Political stability in the immediate term is expected to encourage private consumption and investment, supporting the GDP growth outlook at 4.0%.

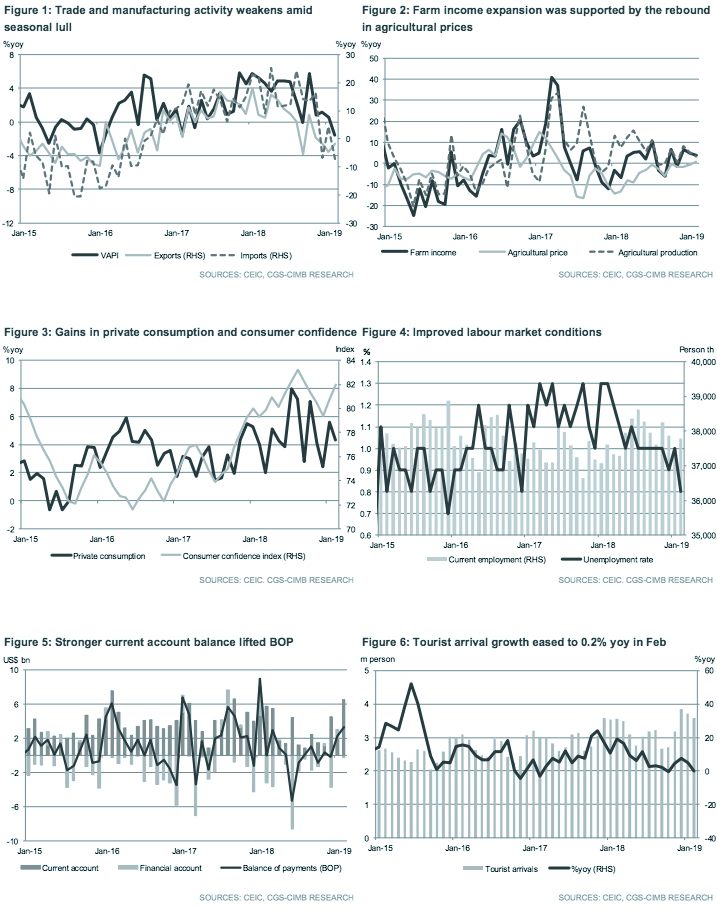

Trade balance returned to a healthy position as imports plunge

Thailand’s exports contracted albeit at a slower pace in February (-1.7% yoy vs.-4.8% yoy in January) while imports waned 7.3% yoy (+4.2% yoy in January), resulting in a trade surplus of US$3.5bn (-US$0.2bn in January). The dip in industrial activity (-1.6% yoy in February vs. +0.6% yoy in January) was due to pronounced slippages in textiles & apparel, chemicals, rubber & plastics, electrical appliances and hard disk drive segments, in conjunction with one less working day this year.

Potential boost in consumer spending with government assistance

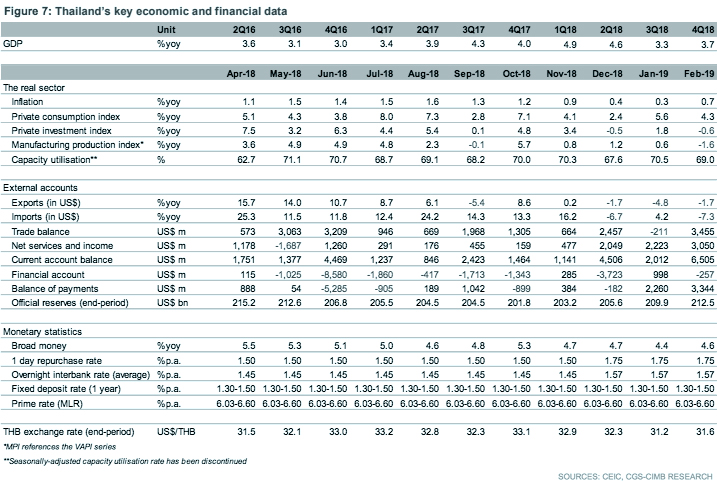

Overall private consumption grew 4.3% yoy (+5.6% yoy in January), complemented by higher consumer confidence (82.0 pt vs. 80.7 pt in January) and labour market improvements. Nominal farm income rose 3.9% yoy in February (+4.8% yoy in January), supported by an uptick in agricultural prices (+0.7% yoy vs. -0.4% yoy in January). The THB87bn cash handouts to the low-income earners since Dec 2018 possibly supported household spending. Extensive measures promised by pro-junta Palang Pracharat Party (PPR) to maintain state welfare cards, hike daily minimum wage and lower personal income tax are anticipated to lift consumer spending going forward, if the party leads the new government.

Stronger current account lifted BOP balance

The balance of payments (BOP) surplus widened (+US$3.3bn in February vs. +US$2.3bn in January), supported by a healthier current account surplus (+US$6.5bn vs. +US$2.0bn) driven by the goods surplus and services & income accounts (+US$3.1bn vs. +US$2.2bn in January). Tourist arrival growth eased to 0.2% yoy in February (+4.9% yoy in January), attributable to the decline in Chinese tourist arrivals due to last year’s higher base.

Major investment plans remain on track after elections

Infrastructure projects in the Eastern Economic Corridor (EEC) are expected to broadly continue as planned, with Gen Prayut of PPR widely tipped as the new Prime Minister. The winning bidders for the five mega-projects are on track to be unveiled by April, with China and Japan bids expected to be frontrunners. Both countries have agreed to coinvest as well as offer loan arrangements to fund the EEC projects. Besides that, the Southern Economic Corridor (SEC), a master plan spanning four years (2019-2022), is due to be launched soon with a budget of THB107bn, as approved by the cabinet in January.

Clearing of political clouds brightens economic prospects

The better-than-expected election results for the pro-junta coalition raises likelihood of pro-poor policies and continuity of key infrastructure projects. Political stability could also provide a breakthrough on efforts to boost private investments, which had turned cautious following the 2014 coup d’état. We retain our GDP growth outlook for Thailand (CGSCIMB: +4.0% in 2019F), which may still prod the Bank of Thailand (BOT) into one policy rate hike to 2.00% by the end of 2019. Risks to this view include a downturn in global growth, protracted US-China trade tensions and monetary policy easing by the US Federal Reserve.

Originally published by CIMB Research and Economics on 29 March 2019.

This article has been edited to reflect its time-sensitivity.