Thailand: Macro snapshot

HIGHLIGHTS

Macro snapshot

- A dip in agriculture exports and slower tourist arrivals weighed on the current account, but net financial outflows abated, relieving pressure on the balance of payments.

- Gains in consumer confidence and household spending were supported by wage growth as well as the recent recovery in farm incomes and agriculture prices.

- The NLA approved a narrower budget deficit of 2.6% of GDP in FY19 following the fiscal stimulus extended earlier this year and gradual economic recovery.

- As the output gap narrows and inflation picks up, we reiterate our end-2018 policy rate forecast of 1.5%. We project the next rate hike to take place only in early-2019.

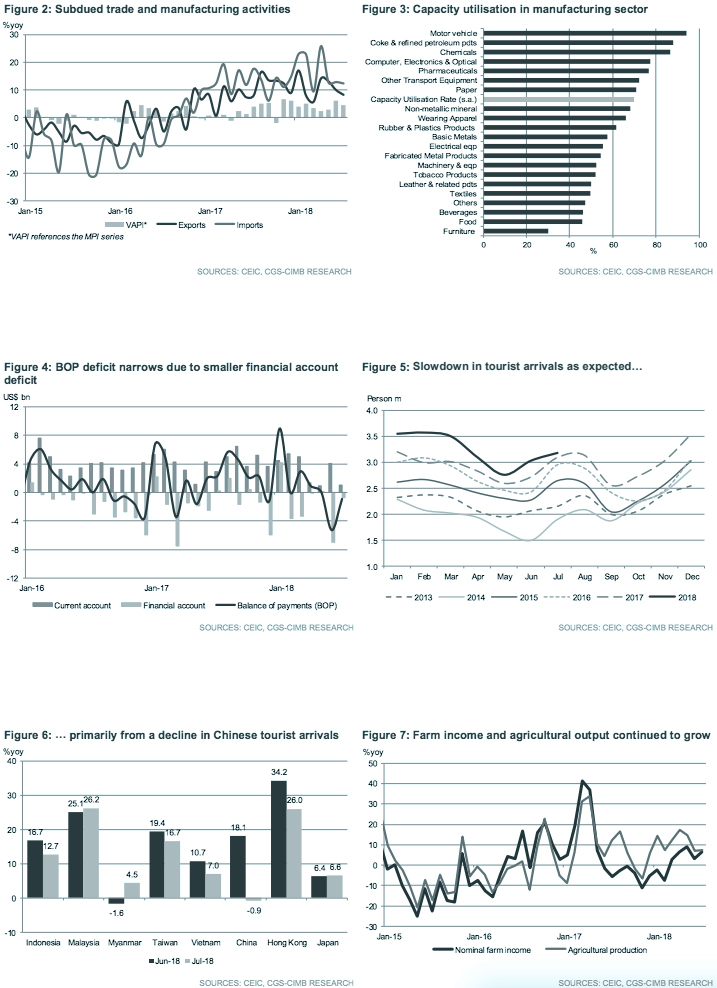

Trade and manufacturing expansion eases in July

Export growth eased to 8.3% yoy in July (+10.0% yoy in June), mainly due to a reversal in agricultural export growth (-4.3% yoy vs. +6.7% yoy in June). Import growth was also more modest in July (+12.4% yoy vs. +12.9% yoy in June) due to moderation in in-bound shipments of capital goods, particularly machinery & equipment (+3.4% yoy in July vs. +13.7% yoy in June). Manufacturing activity, measured by the Value Production Index (VAPI), toned down in July (+4.6% yoy vs. +5.0% yoy in June), dragged by lower production in food & beverages, cement & construction, electrical appliances and hard disk drives (HDD). Seasonally-adjusted capacity utilisation in the manufacturing sector decreased to 69.6% in July (70.1% in June).

Weaker current account offset by subsiding financial outflows

A narrower trade balance of US$0.9bn in July (vs. +US$2.9bn in June), alongside lower net inflows from services and income accounts (+US$0.2bn vs. +US$1.2bn in June) depressed the current account surplus (+US$1.1bn vs. +US$4.1bn in June). The financial account registered a smaller deficit (-US$0.7bn in July vs. -US$7.0bn in June) as net outflows in portfolio and other investments abated, resulting in a slimmer overall balance of payments (BOP) deficit in July (-US$0.9bn vs. -US$5.3bn in June).

Tourist arrivals show a slowdown

The number of international arrivals moderated sharply as expected in July (+2.8% yoy vs. +11.6% yoy in June), primarily affected by the decline in tourists from China (-0.9% yoy in July vs. +18.1% yoy in June) following the recent boat accident in Phuket. Arrivals from neighbouring countries, such as Malaysia (+26.2% yoy), Myanmar (+4.5% yoy) and Japan (+6.6% yoy), while encouraging, were unable to offset the drag on tourist spending.

Farmers’ incomes rise for fifth straight month

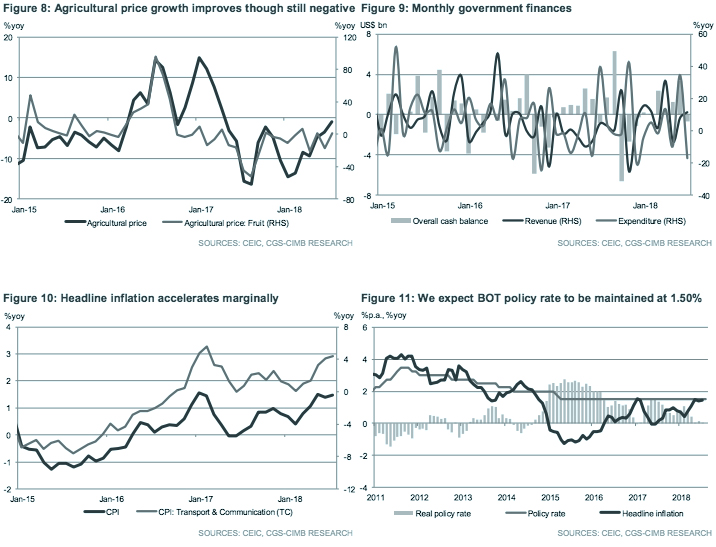

Nominal farm incomes continued to grow at a more steady pace in July (+6.5% yoy vs. +3.3% yoy in June), aided by diminished declines in agricultural prices (-0.9% yoy vs. – 3.5% yoy in June), spurred by higher fruit prices. While regional agricultural prices have risen due to adverse weather, we are monitoring the effects of recent floods on Thailand’s farm production, which continued to grow in July (+7.4% yoy vs. +7.1% yoy in June).

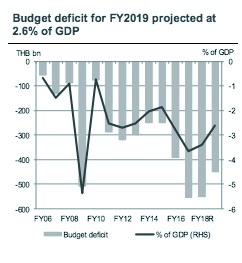

Less fiscal support in FY2019

On 30 August, the National Legislative Assembly (NLA) after the second and third readings approved the budget that will finance FY2019 beginning 1 October. Under the budget, revenue was estimated at THB2.55tr or 2% above FY2018R while current expenditures were projected at THB2.26tr (+1.1%) and capital expenditures at THB660bn (-2.4%). Following the stimulus package enacted earlier this year, the government intends to pull back on fiscal support, targeting a narrower budget deficit of THB450bn (-2.6% of GDP) in FY2019 (vs. THB550bn or -3.4% of GDP in FY2018). As the output gap wanes and inflation accelerates next year, we expect the Bank of Thailand (BOT) to begin tightening monetary policy in early-2019 and reiterate our end-2018 policy rate forecast at 1.50%.

Originally published by CIMB Research and Economics on 3 September 2018.