Thailand: January macro snapshot

HIGHLIGHTS

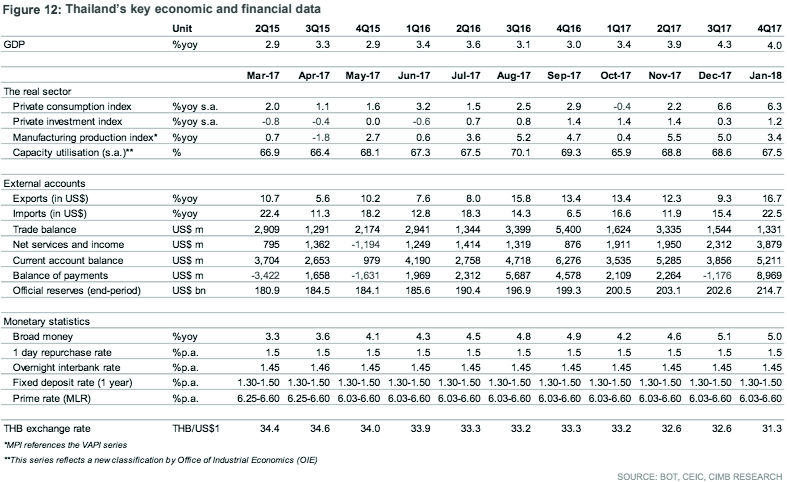

January macro snapshot

- Manufacturing activity took a breather in Jan (+3.4% yoy) after strong gains in Dec, but the opposite was true for export growth, which romped to a five-year high.

- A strong external sector casts the more subdued gains in domestic demand in starker light, prompting government action to boost consumption and investment.

- With the domestic recovery far from assured and inflation well below the policy target of 1-4%, BOT will be in no hurry this year to raise the policy rate, currently at 1.50%.

Manufacturing activity drifts lower

The expansion in the manufacturing production index (MPI) moderated to 3.4% yoy in Jan (+5.0% in Dec), with a broad swath of industries, including autos, rubber & plastics and hard disk drives, hitting a bumpy patch. The seasonally-adjusted capacity utilisation in the manufacturing sector moved down a rung to 67.5% in Jan, from 68.6% in Dec.

Goods and services buoy external sector

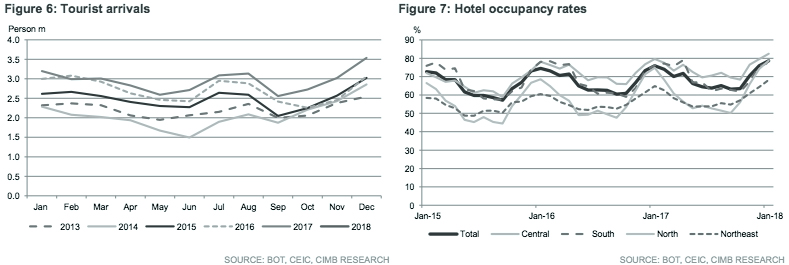

Exports, on the other hand, enjoyed a rebound to 16.7% yoy in US$ terms (+9.3% yoy in Dec), spurred by increased pre-Lunar New Year shipments, higher commodity prices and FX translation gains as the THB strengthened 2.3% mom against US$ in Jan. We remain optimistic Thailand will achieve an export growth of 9.4% in 2018 (9.7% in 2017). The growth in tourist arrivals moderated to 10.9% yoy in Jan to 3.5m (vs. +15.5% yoy in Dec), but we expect Feb numbers to improve as Lunar New Year beckons more inbound travel.

External financing conditions improve

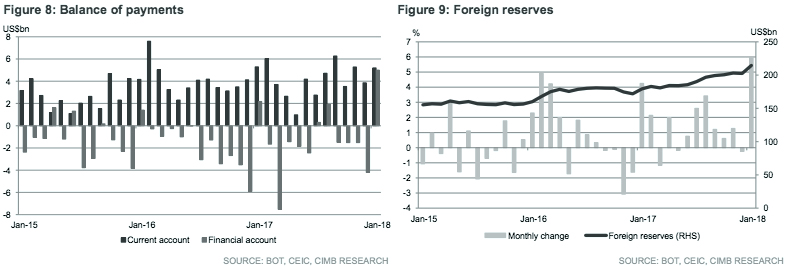

Thailand’s current account recorded a larger surplus of US$5.2bn in Jan (+US$3.9bn in Dec) on the back of higher net inflows from the services and income accounts (+US$3.9bn vs. +US$2.3bn in Dec). The trade surplus was flat at US$1.3bn in Jan (+US$1.5bn in Dec). Deficits gave way to a surplus in the financial account, (+US$5.0bn in Jan vs -US$4.2bn in Dec), thanks to positive net inflows of direct and portfolio investments.

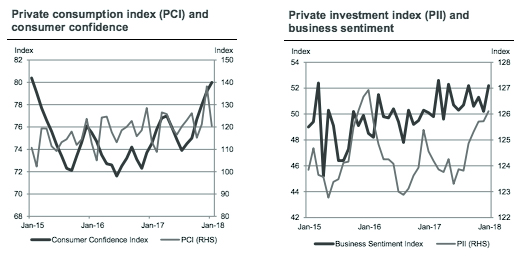

Diffusing gains to broader economy is still a work in progress

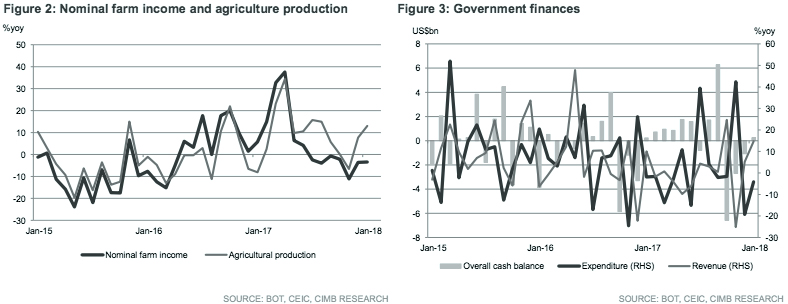

Consumer confidence improved in Jan (80.0 vs. 79.2 in Dec), but hard indicators were less upbeat. The private consumption index weakened in Jan, while farm incomes (-3.4% yoy in Jan) were set back by a decline in agriculture prices. The government has stepped up efforts at lifting household purchasing power, particularly among the low-income, with recent announcements to 1) regulate non-bank finance and reduce punitive interest rates to indebted households, 2) amend banking agent regulations to improve banking access in remote areas, and 3) speed up farm sector reforms, particularly in rice and rubber.

Approval of Eastern Economic Corridor bill

In Feb, the Eastern Economic Corridor (EEC) Act received legislative approval, which is expected to eventually attract a new wave of foreign investments via perks such as: 1) personal income tax reductions of up to 15% for local and foreign investors, 2) 0% corporate tax for up to 15 years, 3) 99-year land leases, and 4) 5-year work permit visas for foreign workers. The EEC Committee has also greenlighted a THB200bn high-speed rail project connecting key airports, which is expected to begin the tender process in Apr, with contract signings targeted for Dec.

Too early to stop the monetary medicine

Headline inflation drifted lower to 0.7% yoy in Jan (+0.8% yoy in Dec) owing to muted gasoline inflation and depressed meat and egg prices. Inflation is expected to reach an inflection point in 2Q18, accelerating to 1.5% in 2018 (+0.7% in 2017), but not enough to warrant a tighter monetary policy stance by the Bank of Thailand (BOT), even as the government steps up fiscal support. As such, we expect BOT to maintain the one-day repurchase rate at the current level of 1.50% throughout 2018 to facilitate the recovery in domestic demand.

Originally published by CIMB Research and Economics on 28 February 2018.