Thailand: 2Q18 GDP

HIGHLIGHTS

2Q18 GDP

- Thailand’s economy expanded by 4.6% yoy in 2Q18 after an upwardly-revised GDP growth reading of 4.9% yoy in 1Q18.

- Domestic demand rebounded strongly, led by private consumption and investments.

- Subdued inflation, ample FX reserves and orderly THB adjustments had underpinned our view that BOT may delay increasing the policy rate until early-2019.

- However, our upgraded 2018 GDP growth forecast (+4.5%) suggests output gap is fast narrowing which could compel BOT to speed up a rate hike if growth outperforms.

GDP growth eases but still ahead of expectations

Thailand’s real GDP grew 4.6% yoy in 2Q18 (CIMB: +4.3% yoy, Bloomberg consensus: +4.4% yoy), while growth in 1Q18 was bumped up to 4.9% yoy from an initial estimate of 4.8% yoy. On a seasonally adjusted basis, the economy expanded by 1.0% qoq (+2.1% qoq in 1Q18). Domestic demand accounted for 3.5% pts or 91.7% of headline GDP growth in 2Q18 (+2.8% pts or 84.1% in 1Q18), the highest ratio since 2Q16, due to the progressive recovery in private consumption and investments.

Recovery in consumer spending augmented by surge in car sales

The recovery in private consumption extended to 4.5% yoy in 2Q18 (+3.7% yoy in 1Q18) due to sustained increases in household purchasing power, government transfers, a nascent turnaround in farm incomes (+6.1% yoy vs. -2.3% yoy in 1Q18), and consumer confidence reaching a 13-quarter high. In a sign household finances are on a firmer footing, demand for durable goods rose, particularly car purchases, which surged following the end of the 5-year ownership requirement under the first car buyer scheme. However recent floods in Thailand may disrupt the income recovery in agriculture-based regions if farm property and produce are damaged.

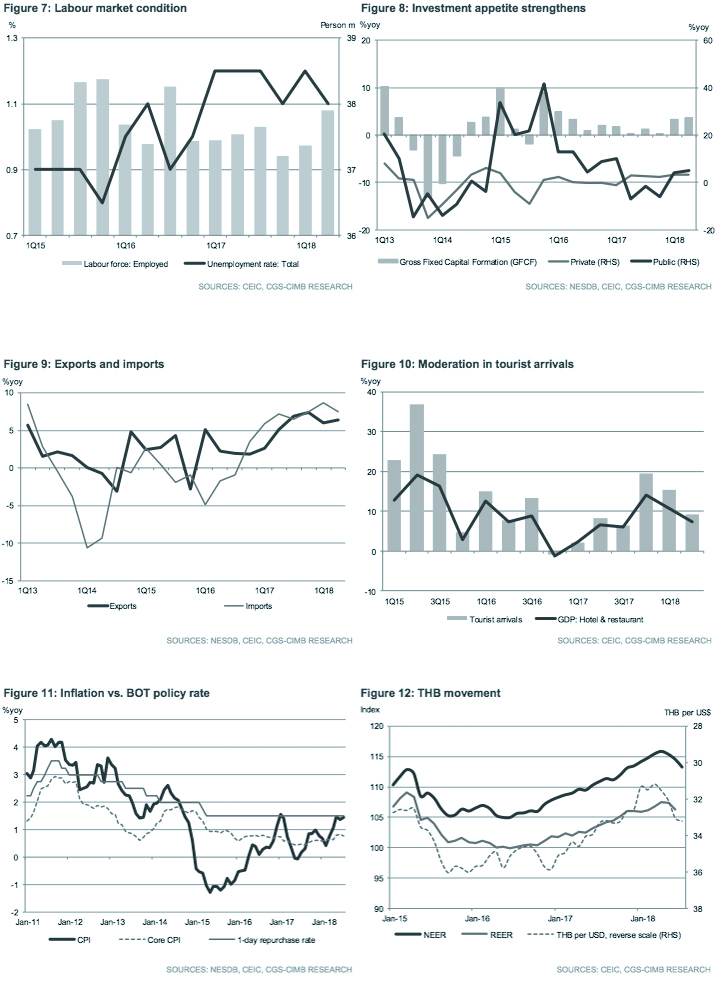

Investment appetite strengthens

The erosion of producer spare capacity, new measures to spur the SME sector, Eastern Economic Corridor (EEC)-centric investments and a ramp-up in government development expenditure are key factors supporting gross fixed capital formation (+3.6% yoy in 2Q18 vs. +3.4% yoy in 1Q18). The pipeline of investments in Thailand remains strong, with the value of projects approved by the Board of Investment (BOI) reaching THB118bn. Recently, the government lifted the year-long freeze on electric vehicle (EV) applications with the approval of THB30bn EV investments to be located in the EEC.

External sector weighed down by services deficit

Net exports declined for the second consecutive quarter (-0.2% pts in 2Q18 vs. -0.9% pts in 1Q18), albeit a shallower contraction on the back of an improved goods trade surplus. The external sector was weighed down by a trade deficit in services due to a moderation in tourist arrivals (+9.1% in 2Q18 vs. +15.4% yoy in 1Q18), which corresponded with slimmer gains in the hotel & restaurant sector. The Phuket boat accident in Jul that claimed the lives of 41 Chinese nationals may dampen tourist sentiment in the near term but we expect Thailand’s resilient tourism sector to eventually weather the storm.

Positive growth surprises may accelerate timing of policy rate hike

We revise our GDP growth forecast for the second successive quarter to 4.5% in 2018 (from 4.3%), which is the midpoint of the National Economic and Social Development Board’s (NESDB) 4.2-4.7% range. External trade uncertainty, subdued inflation, ample FX reserve buffers and the orderly manner of THB depreciation had underpinned our expectations that the Bank of Thailand (BOT) would not be rushed into an interest rate increase this year; however, back-to-back GDP outperformance suggests that the output gap in Thailand is fast narrowing. Hence, while we still expect the BOT to begin normalising monetary policy in early-2019, we would not rule out a potential policy rate hike in end-2018 if the growth trajectory continues to gather steam.

Originally published by CIMB Research and Economics on 8 August 2018.