Singapore: MAS monetary policy review

HIGHLIGHTS

MAS monetary policy review

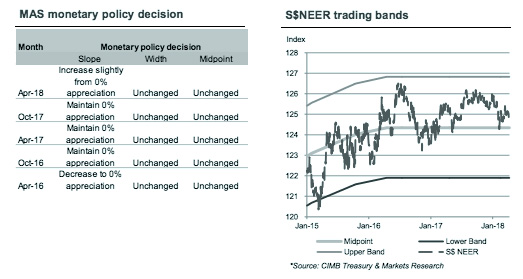

- MAS has shifted to an appreciation bias for the S$NEER by increasing the slope of the policy band slightly but retaining its width and mid-point.

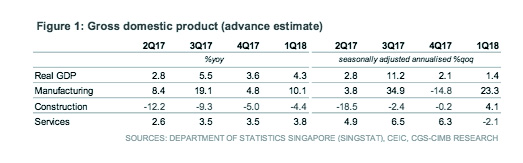

- Flash GDP estimates showed Singapore’s economy registering an expansion of 4.3% yoy in 1Q18, led by the manufacturing and services clusters.

- Following the adjustments made on 13 April 2018, MAS is likely to adopt a prudent stance in view of heightened uncertainties surrounding the global trade environment.

- We expect monetary settings to remain on hold at the next scheduled policy review in October.

MAS adopts tighter stance by raising slope of S$NEER policy band

At its bi-annual monetary policy review, the Monetary Authority of Singapore (MAS) increased the slope of its policy band, advocating a “modest and gradual appreciation” of the S$ nominal effective exchange rate (NEER) but left the other two parameters – the width and the mid-point of the policy band – unchanged. 16 of 24 forecasters surveyed by Bloomberg had forecast the decision, including us. The decision marks the first shift in its exchange rate policy stance since Apr 2016 and the first tightening since Apr 2012. Policymakers cited improving economic and labour market conditions as well as budding inflation as factors in favour of the decision.

Modest and gradual appreciation

CIMB Treasury & Market Research’s proprietary S$NEER has generally trended 0-1% above the mid-point in the past three months, reflecting optimism of a turnaround in Singapore’s growth prospects and broad US$ weakness. Going forward, we expect the pace of appreciation to remain gradual. Our base case expects the S$NEER to continue trading 0-1% above the mid-point in the next six months.

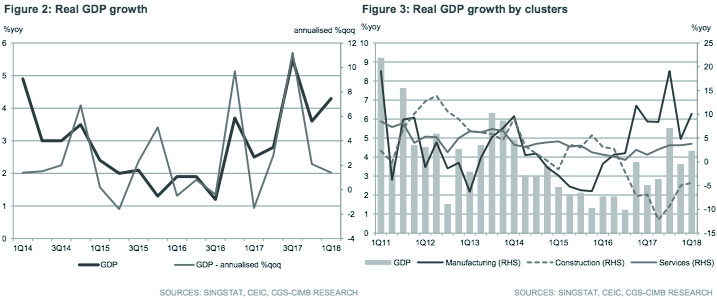

GDP growth accelerates to 4.3% yoy…

The policy decision came alongside the release of advanced estimates of Singapore’s real GDP growth by the Ministry of Trade and Industry (MTI), which showed the economy expanding by a healthy 4.3% yoy in 1Q18 (CIMB: +4.5% yoy, Bloomberg consensus: +4.3% yoy, 4Q17: +3.6% yoy). On a qoq seasonally adjusted annual rate (SAAR) basis, real GDP growth advanced 1.4% qoq SAAR (CIMB: +1.8% qoq, Bloomberg consensus: +1.2% qoq, +2.1% qoq in 4Q17). We have tweaked our full-year GDP growth forecast to 3.2% for 2018F (from 3.6% earlier), in line with MAS’ expectations that growth will land towards the top half of its forecast range of 1.5% to 3.5%.

… on the back of gains in manufacturing and services

The manufacturing sector expanded 10.1% yoy in 1Q18 (+4.8% yoy in 4Q17), driven by the electronics and precision engineering segments. The services sector expanded 3.8% yoy in 1Q18 (+3.5% in 4Q17), primarily led by the finance & insurance and wholesale & retail trade segments. The construction sector remained a drag on headline growth, contracting 4.4% yoy in 1Q18 (-5.0% yoy in 4Q17), pulled down by a decline in both private sector and public sector construction.

Inflation has bottomed out

Headline (+0.5% yoy in Feb) and core inflation (+1.7% yoy in Feb) have gradually strengthened on the back of higher imported cost pressures, a recovery in domestic demand and a tightening labour market. We forecast headline inflation to trend higher to 1.4% in 2018F (+0.6% in 2017), ahead of MAS’ expected range of 0% to 1%.

External uncertainties gives MAS pause for thought

Following the adjustments made on 13 April 2018, MAS is likely to adopt a prudent stance in view of heightened uncertainties surrounding the global trade environment amid US-China tariff skirmishes and tightening financial conditions brought on by a further three interest rate hikes by the US Federal Reserve in 2018, while awaiting for more evident signs of accelerating wage and core inflation. Therefore, we expect monetary settings to remain on hold at the next scheduled policy review in October.

Originally published by CIMB Research and Economics on 13 April 2018.