Singapore: March 2018 industrial production

HIGHLIGHTS

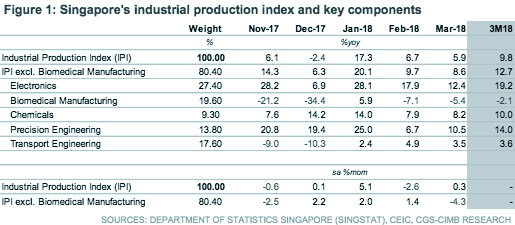

March 2018 industrial production

- IPI growth eased to 5.9% yoy in March, shy of our forecast due to disappointments in semiconductor and pharmaceutical production.

- The pharmaceutical sector saw unusually large revisions in its February data, as an initial reading of a 15.2% yoy increase was revised to a decline of 7.4% yoy.

- The sharper-than-expected moderation in external demand had led us to revise our projections of Singapore’s GDP growth to 3.2% in 2018 from 3.6%.

- We expect MAS to maintain its current monetary settings at the Oct policy review.

IPI growth corrects following February surge, but still ahead of forecasts

Expansion in the manufacturing sector, as measured by the industrial production index (IPI), moderated to 5.9% yoy in March (CIMB: +6.2% yoy, Bloomberg consensus: +5.7% yoy), following a downwardly revised increase of 6.7% yoy in February. IPI excluding the volatile biomedical sector increased 8.6% yoy (+9.7% yoy in February). On a sequential basis, the manufacturing sector notched a 0.3% mom gain in seasonally adjusted terms; however, Feb’s decline was revised significantly lower to -2.6% mom from an initial reading of -0.5% mom.

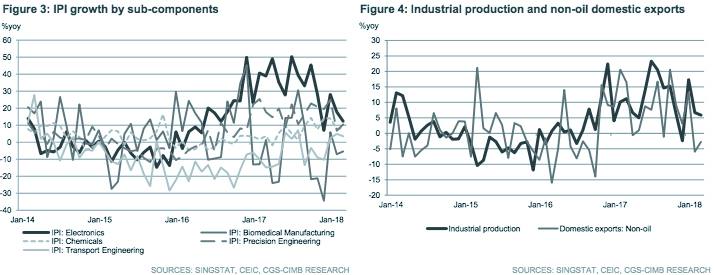

Electronics output moderates as smartphone cycle peaks

Production of electronics expanded by a slower 12.4% yoy in March (+17.9% yoy in February), on moderating growth for semiconductors (+18.8% yoy vs. +27.4% yoy in February), amid softening demand for smartphones. Output growth for computer peripherals remained stagnant (+0.2% yoy vs. +0.9% yoy in February) while contractions persisted in the data storage (-19.0% yoy vs. -21.8% yoy in February), consumer electronics (-7.7% yoy vs. -9.1% yoy in February) and other components (-0.5% yoy vs. -24.5% yoy in February).

Major revisions in pharma drags down headline IPI readings

Activity in biomedical manufacturing turned out to be weaker than expected in March, contracting 5.4% yoy on the back of declines in pharmaceuticals (-7.2% yoy) and medical technology (-0.4% yoy). Notably, February’s biomedical manufacturing data saw unusually large downward revisions, from an increase of 8.4% yoy to a decline of 7.1%, principally due to adjustments made to pharmaceutical output from an increase of 15.2% yoy to a decline of 7.4%.

Return from holidays spurs factories into action

The return from the CNY break spurred production across many sectors, including chemicals, precision engineering, transport engineering, F&B, apparel and basic metals. Meanwhile, general manufacturing activity contracted for a second consecutive month due to printing and miscellaneous industries.

Slower export and manufacturing activity dims our growth outlook

The sharper-than-expected moderation in external demand had led us to revise our projections of Singapore’s GDP growth recently. We now expect the Singapore economy to expand by 3.2% in 2018 against an initial forecast of 3.6% and at the upper end of the Ministry of Trade and Industry’s (MTI) estimated range of +1.5-3.5%.

Catalysts for further policy tightening still out of sight

Following the decision to tighten monetary policy by raising the slope of the S$NEER policy band on 13 April to allow for a ‘modest and gradual appreciation’, we expect the Monetary Authority of Singapore (MAS) to tread more cautiously due to heightened trade tensions between the US and China, the tightening of global financial conditions arising from expectations of further US interest rate hikes, the still-nascent recovery in the domestic economy and tepid core inflation. Hence, we maintain expectations for monetary settings to remain on hold at the next scheduled policy review in October.

Originally published by CIMB Research and Economics on 26 April 2018.