Singapore: July 2018 industrial production

HIGHLIGHTS

July 2018 industrial production

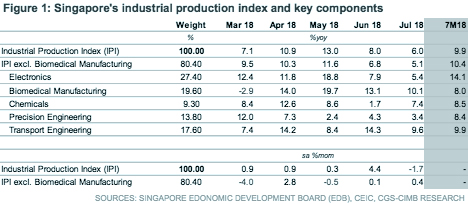

- The industrial production index (IPI) came in ahead of our forecast at 6.0% yoy in July due to resilient pharmaceutical and chemicals output growth.

- However the prognosis for the electronics cluster, which accounts for 27% of the manufacturing sector, remains weak in 2H18.

- We cut our Singapore GDP growth forecast for 2019 from 2.8% to 2.6% (2018 forecast intact at 3.2%) owing to slowing cyclical drivers and negative trade spillover.

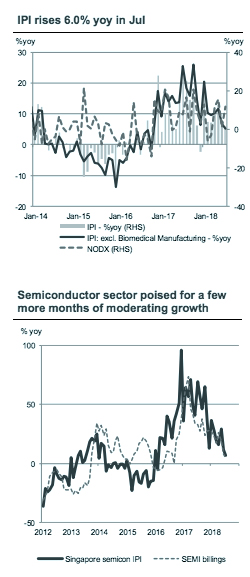

IPI growth slowed less than we expected…

The IPI beat our forecast, rising 6.0% yoy in July (CIMB: +4.9% yoy, Bloomberg consensus: +6.0% yoy), and was accompanied by an upward revision in June’s pace to 8.0% yoy. Manufacturing activity, excluding the volatile biomedical sector, grew 5.1% yoy in July (+6.8% yoy in June), mirroring the headline trend. On a seasonally-adjusted basis, the IPI declined 1.7% mom, breaking a four-month streak of increases that ended with a 4.4% mom gain in June.

… due to resilient biomedical production …

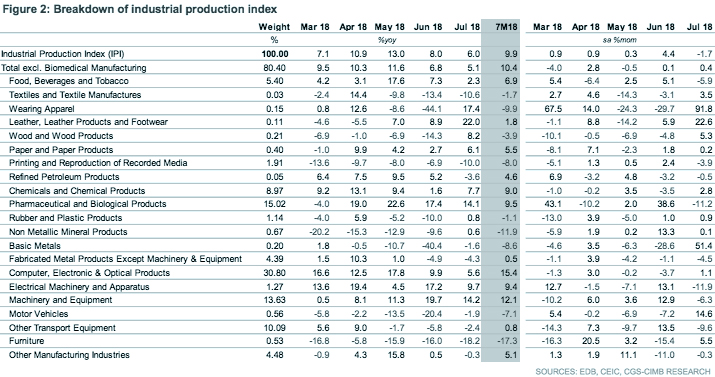

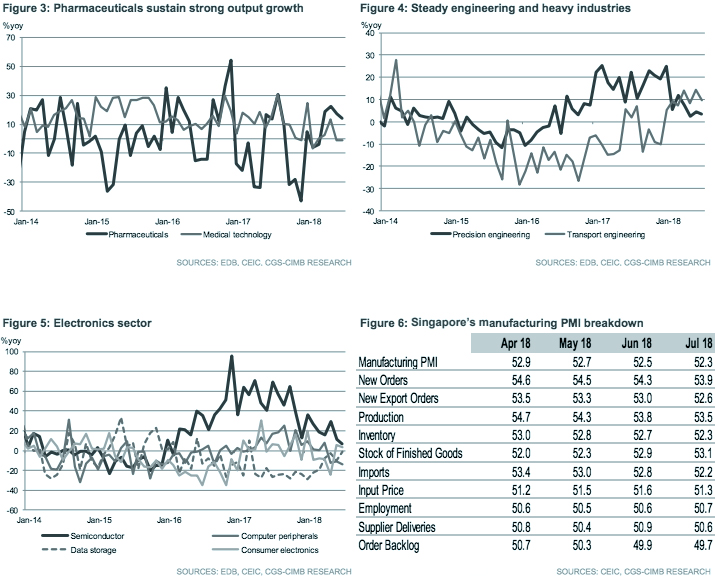

Biomedical manufacturing sustained double-digit growth for the fourth consecutive month (+10.1% yoy in July vs. +13.1% yoy in June). Despite traditionally being volatile, pharmaceuticals – which stand out as the second largest sub-cluster in the manufacturing sector – has sustained strong output growth at 14.1% yoy in July (+17.4% yoy in June) and 9.5% yoy in 7M18.

… and a stronger showing in the chemicals cluster

The chemical sector’s activity improved in July (+7.4% yoy vs. +1.7% yoy in June) mainly boosted by robust demand for other chemicals (+15.8% yoy vs. -6.0% yoy in June) and specialty chemicals (+1.9% yoy vs. -2.6% yoy in June). Petrochemical output growth eased to 7.8% yoy in July (+14.4% yoy in June) while petroleum output contracted for the first time since a year ago (-3.6% yoy vs. +5.2% yoy in June) due to the closure of a plant for maintenance.

Steady engineering and heavy industries

The precision engineering segment registered growth of 3.4% yoy (+4.3% yoy in June) despite a more challenging base. Transport engineering growth moderated to a stillrobust 9.6% yoy (+14.3% yoy in June) as a pickup in aerospace (+23.5% yoy vs. +4.9% yoy in June) cushioned cooling marine & offshore activity (+1.4% yoy vs. +32.1% yoy in June).

Electronics IPI growth to remain weak until late 2018

Expansion in the electronics sector (+5.4% yoy in July vs. +7.9% yoy in June) was weighed down by a challenging base arising from last year’s demand surge. We expect the yoy trend in the electronics sector to only bottom in late 2018, as global demand for semiconductors (+7.0% yoy vs. +11.3% yoy in June), which make up 62% of the sector’s production, stagnates.

Manufacturing sector bracing for more headwinds

We expect Singapore’s GDP growth to moderate to 2.3% yoy in 2H18 (+4.2% yoy in 1H18) as cyclical drivers that spurred demand last year have waned. Negative spillover from the US-China trade spat on demand for Singapore’s exports is emerging as a significant risk to the economic outlook for 2019, following the impasse in trade negotiations between the two countries this week. We have moderated our GDP growth estimate for 2019 accordingly from 2.8% to 2.6%. Our 2018 GDP forecast is intact at 3.2%.

Originally published by CIMB Research and Economics on 24 August 2018.