Singapore: February 2018 trade

HIGHLIGHTS

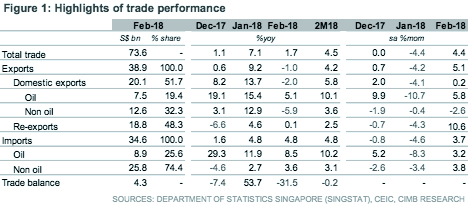

February 2018 trade

- Non-oil domestic exports (NODX) declined in Feb (-5.9% yoy vs. +12.9% yoy in Jan) on the back of weaker electronics and non-electronics shipments.

- Spillovers from US tariffs are contained so far, but broader threats aimed at China are a significant risk to Singapore, especially if they target key electronics clusters.

- Until these risks materialise, Singapore’s economic outlook remains intact, providing a sufficient base for MAS to allow a greater appreciation bias for the S$ NEER in Apr.

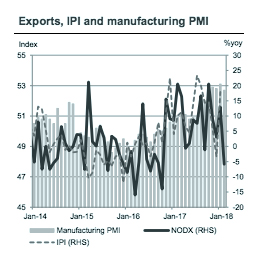

Sequential NODX declines are a slight concern

Non-oil domestic exports (NODX) declined 5.9% yoy in Feb, significantly below expectations of gains (CIMB: +3.0% yoy; Bloomberg consensus: +4.8% yoy; Jan: +12.9% yoy). Export activity declined in both the electronics sector (-12.3% yoy vs. -3.9% yoy in Jan) and non-electronics sector (-3.4% yoy vs. +20.7% yoy in Jan). Seasonal distortions from the Chinese New Year (CNY) break may have skewed exports to the downside, but we are monitoring signs of more persistent weakness in exports, as the seasonally adjusted NODX has registered three months of sequential contractions (-2.6% mom in Feb vs. -0.4% mom in Jan).

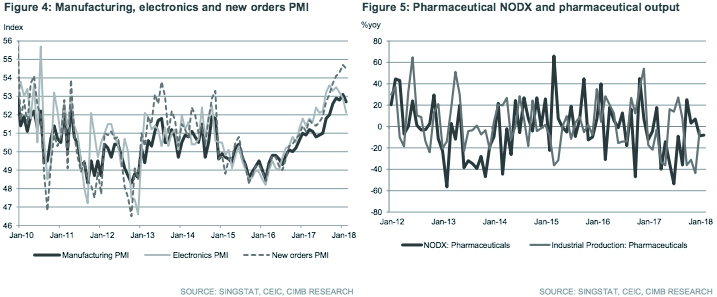

Third consecutive month of contraction in electronics exports

Drags to the electronics cluster were broad-based as the collective exports of the five largest electronics items fell 10.6% yoy in Feb (-4.5% yoy in Jan): integrated circuits (- 11.4% yoy vs. -10.2% yoy in Jan), PC parts (-48.1% yoy vs. -31.4% yoy in Jan), diodes and transistors (-25.6% yoy vs. +0.4% yoy in Jan), and telecom equipment (-13.4% yoy vs. +24.8% yoy in Jan). Only the PC segment recorded gains in Feb (+17.7% yoy vs. +30.9% yoy in Jan). Non-electronics NODX were hit by volatility in contributions from petrochemical shipments (-12.9% yoy in Feb vs. +11.3% yoy in Jan) and the pharmaceutical segment (-8.0% yoy in Feb vs. -8.7% yoy in Jan).

PMI indicates slower expansion in manufacturing sector

Singapore’s official manufacturing PMI fell 0.4 pts to 52.7 in Feb (53.1 in Jan) due to slippages in output, new orders, new export orders, imports, employment and order backlogs. The electronics PMI decreased 0.8 pts to 52.1 in Feb (52.9 in Jan), the lowest level in eight months, as the sub-indices for production and new orders declined further.

Activity dropped as Asia celebrated the new lunar year

Singapore saw a sharp dip in exports to a number of key trading partners that broke for recess over CNY in Feb: China (-23.6% yoy), Taiwan (-18.6% yoy), Hong Kong (-14.7% yoy), Thailand (-13.0% yoy), Malaysia (-5.7% yoy) and Indonesia (-4.4% yoy). The exceptions – Japan, South Korea and the US – were driven by higher non-electronics NODX, which is typically less exposed to the Asian manufacturing supply chain.

Global trade outlook tainted by Trump tariff talk…

We are cognisant of the downside risks posed by a more protectionist US trade stance. US President Donald Trump recently threatened to impose tariffs on up to US$60bn of Chinese imports targeting the technology, consumer electronics and telecommunications sectors. This would have significant ramifications on Singapore’s trade outlook if they come to pass as electronics account for about 30% of NODX.

… but not enough to deter MAS normalisation process

Despite increasingly feisty exchanges between the major trade nations, spillovers have so far been contained. We maintain our NODX forecast of 6.7% for 2018F, and Singapore’s economic growth prospects remain intact. We continue to expect the Monetary Authority of Singapore (MAS) to tweak its policy stance to allow for more S$ nominal effective exchange rate (NEER) appreciation at its policy review next month.

Originally published by CIMB Research and Economics on 16 March 2018.