Singapore: 2Q18 GDP growth (advance estimates)

HIGHLIGHTS

2Q18 GDP growth (advance estimates)

- Singapore’s economy lost speed in 2Q18, expanding 3.8% yoy (+4.3% yoy in 1Q18) and 1.0% qoq SAAR (+1.5% qoq SAAR in 1Q18).

- While manufacturing remains a key engine of growth, we see headwinds gathering in 2H18 amid easing electronics demand and retaliatory tariffs by the US and China.

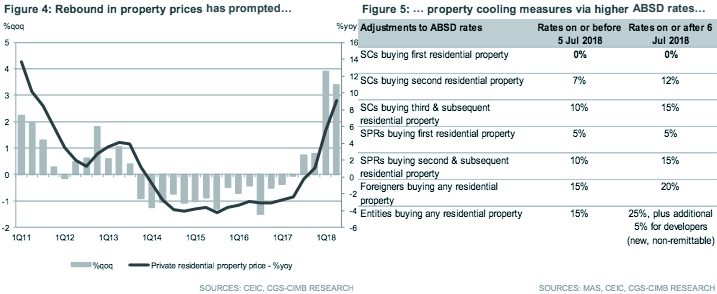

- Property cooling measures are a setback to our expectations of a quicker recovery in the construction sector, which extended its contraction streak to 8 straight quarters.

- Risks to the outlook are global trade tensions, tighter global financial conditions, slower growth in G3 and China as well as geopolitical uncertainty.

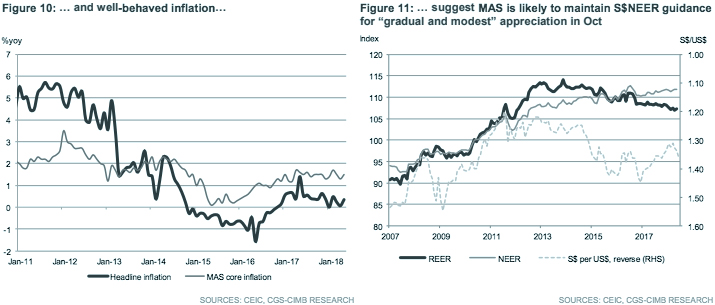

- We retain our forecast for MAS to maintain its current monetary policy stance, advocating a “gradual and modest” pace of appreciation for the S$NEER.

GDP growth slims down, marginally below expectations

Singapore’s economic expansion moderated to 3.8% yoy in 2Q18, based on the advance estimate from the Ministry of Trade and Industry (CIMB: +4.0% yoy, Bloomberg consensus: +4.1% yoy; +4.3% yoy in 1Q18). On a qoq seasonally adjusted annual rate (SAAR) basis, real GDP growth rose at a slower pace of 1.0% qoq, following a more robust reading of 1.5% qoq SAAR in the previous quarter.

and services sectors remain resilient

Production of electronics expanded by a slower 12.4% yoy in March (+17.9% yoy in February), on moderating growth for semiconductors (+18.8% yoy vs. +27.4% yoy in February), amid softening demand for smartphones. Output growth for computer peripherals remained stagnant (+0.2% yoy vs. +0.9% yoy in February) while contractions persisted in the data storage (-19.0% yoy vs. -21.8% yoy in February), consumer electronics (-7.7% yoy vs. -9.1% yoy in February) and other components (-0.5% yoy vs. -24.5% yoy in February).

Major revisions in pharma drags down headline IPI readings

Growth in the manufacturing sector remained healthy, albeit slower (+8.6% yoy vs. +9.7% yoy in 1Q18), on the back of strong performance in all segments within the sector, particularly led by electronics and biomedical manufacturing. Growth in the services sector eased to 3.4% yoy in 2Q18 (+4.0% in 1Q18), where momentum continued to be buttressed by wholesale and retail trade as well as the financial and insurance segments.

Property cooling measures to dampen construction turnaround

In contrast, the construction sector remained the underperformer as the sector contracted for the eighth consecutive quarter (-4.4% yoy vs. -5.2% yoy in 1Q18), weighed down by private sector construction activity due to the contraction in contracts awarded, which fell 67.5% yoy in May (+39.1% yoy in Apr). In a setback for the residential construction segment, the government recently announced property cooling measures, namely adjustments in the Additional Buyer’s Stamp Duty (ABSD) rates and Loan-to-Value (LTV) limits following a sharp rebound in land prices and en-bloc sales. Particularly for the developers, the additional 5% ABSD rate could raise the cost of land acquisition and reduce the bullishness of tender bids.

Growth outlook remains positive but downside risks gather

Singapore’s economy remains on track to meet our 3.2% GDP growth forecast for 2018, which is broadly in line with the Ministry of Trade and Industry’s (MTI) projection of 2.5% to 3.5%. We are wary of risks arising from disruptions to the trade cycle from incoming tariffs by the US and China, increased protectionist policies by major trade nations, higher interest rates and tighter financial conditions as a result of global monetary policy normalisation, geopolitical uncertainty, and a sudden loss of momentum in the advanced economies and China.

MAS to maintain monetary policy stance

Price pressures remain non-threatening as we forecast headline inflation to moderate to 0.6% in 2018F (+0.6% in 2017), aligned with MAS’s expected range of 0% to 1%. Headline inflation edged up to 0.4% yoy in May (+0.1% yoy in April) due to higher food prices as well as healthcare and education costs. As the balance of risks has tilted towards downside to growth, we expect MAS stay the course on its current guidance for a “gradual and modest appreciation” of the S$NEER at the upcoming Oct policy review. However, if global trade momentum slows sharply as the US and China step up trade threats, we expect MAS to stand ready to recalibrate policy settings to support the economy.

Originally published by CIMB Research and Economics on 13 July 2018.