Malaysia: Mar Monetary Policy Committee meeting – A dovish posture

HIGHLIGHTS

Mar Monetary Policy Committee meeting – A dovish posture

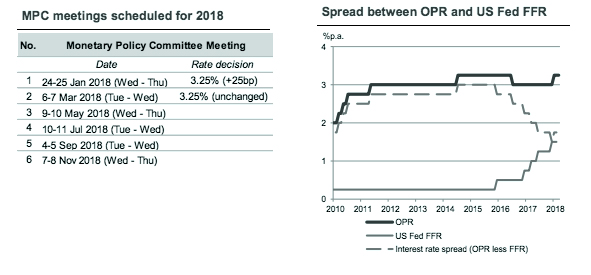

- Malaysia’s Overnight Policy Rate (OPR) was left unchanged at 3.25% on 7 March 2018, following the 25bp hike in Jan.

- BNM remained upbeat about Malaysia’s outlook in 2018 but flagged heightened global risks, citing the resurgence of market volatility and bubbling trade tensions.

- We expect BNM to be nimble in reacting to signs of overheating, but a lack of inflation catalysts advocates staying neutral, amid greater external unpredictability.

- We maintain our end-2018 OPR forecast of 3.25%, implying no further rate hikes this year.

BNM keeps the OPR unchanged at 3.25%

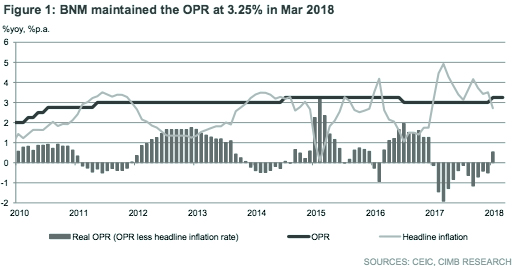

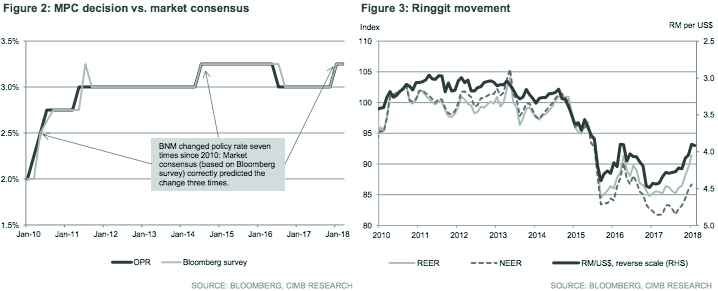

Bank Negara Malaysia’s (BNM) Monetary Policy Committee (MPC) maintained the Overnight Policy Rate (OPR) at 3.25%, following a 25bp hike at the previous meeting in Jan. The decision was in line with our forecast and widely expected by the markets.

Risks to the external outlook loom

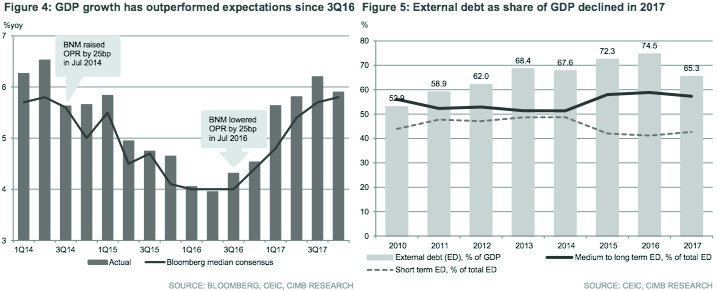

BNM maintained an upbeat assessment of Malaysia’s economic outlook in 2018, supported by firm domestic demand and a supportive external environment. While the central bank expects the global economy to strengthen, it removed a reference to the growth being “entrenched and synchronised”. Moreover, BNM flagged the recent financial market volatility and bubbling trade tensions as potential risks to the global outlook. We expect Malaysia’s economy to grow 5.2% in 2018, while BNM is set to release its forecasts alongside the BNM Annual Report 2017 at the end of Mar.

Core inflation kept in line by productivity and supply-side gains

Headline inflation moderated to 2.7% yoy in Jan, while core inflation was steady at 2.2% yoy. The central bank expects external drivers of inflation to ease in 2018 (CIMB: +2.9%), helped by meeker commodity price gains and a stronger ringgit. It was of interest to us that BNM felt core inflation remained in check due to “improving labour productivity and ongoing investments for capacity expansion”, as slack in the economy keeps the risks of overheating under wraps.

US becoming a source of uncertainty rather than stability

A hawkish testimonial by new Federal Reserve chairman Jerome Powell hinting at upside risks to the US growth and inflation outlook, following the passage of tax reforms, led to speculation that Fed monetary policy normalisation may be more aggressive than the official guidance of three rate hikes this year, which triggered volatility in the financial markets. We expect the US Federal Reserve to deliver another 25bp hike in the Federal Funds Rate (FFR) to 1.75% when it meets on 20-21 Mar, which would narrow the interest rate differential with Malaysia’s OPR to 150bp

More dovish than the previous MPC statement

We think MPC statement on 7 March 2018 leans more dovish than the previous statement in Jan due to the emergence of adverse risks to the global economy, tighter monetary conditions from a stronger ringgit, muted core inflation readings and the removal of a reference to preventing the buildup of risks from low interest rates, which suggest to us that for now, BNM is willing to tolerate the costs of keeping monetary policy accommodative. We reiterate our end-2018 OPR forecast of 3.25%, implying no further hikes this year; however, a nimble BNM means a second rate hike in 2H18 still cannot be ruled out if justified by an overshoot in price pressures.

Originally published by CIMB Research and Economics on 28 February 2018.