Malaysia: January 2018 consumer price inflation

Originally published by CIMB Research and Economics on 28 February 2018.

HIGHLIGHTS

January 2018 consumer price inflation

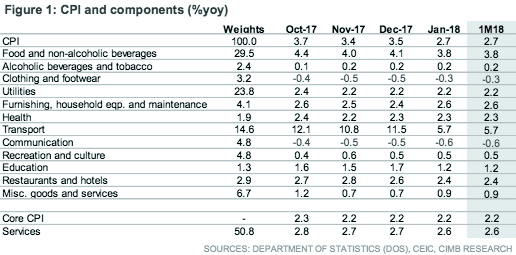

- Headline inflation eased sharply to 2.7% yoy in Jan (+3.5% yoy in Dec) largely due to lower fuel and food inflation.

- Our inflation outlook remains unchanged (+2.9% in 2018 vs. +3.7% in 2017), though risks are skewed to the upside.

- We expect no further OPR hikes this year if core inflation remains subdued, though a second hike in 2H18 cannot be ruled out if demand-pull price pressures surface.

Headline inflation moderated to 13-month low in Jan

Malaysia’s consumer price inflation eased sharply in Jan to 2.7% yoy (CIMB: +2.9% yoy, Bloomberg consensus: +2.8% yoy, +3.5% yoy in Dec). The moderation stemmed from currency gains and a higher base, as fuel prices and electricity tariffs were raised a year ago. Sequentially, headline inflation gained 0.3% in Jan (+0.1% mom in Dec). Underlying price pressures remained well contained, as core inflation plateaued at 2.2% yoy in Jan. CPI weights were tweaked slightly, with spending on transport, furnishing & household, health, recreation and education gaining a larger share of the consumption basket.

Uptick in global oil prices masked by ringgit strength

Transport inflation tumbled to 5.7% yoy in Jan (+11.5% yoy in Dec) despite a monthly rise in the fuel index (+0.5% mom), as this paled against a 10.2% mom fuel price hike in Jan 2017. We expect fuel inflation to subside further in Feb (-1.1% mom) as Brent oil prices fell by 4.8% mom in Feb after seven straight months of gains totaling 45.3% in Jul 2017- Jan 2018. Fluctuations in retail fuel prices have been less volatile amounting to just 12.9% over that period, partly cushioned by the appreciation in the ringgit against US$.

More modest food inflation ahead of CNY

Food inflation drifted lower despite the proximity to the festive season (+3.8% yoy in Jan vs. +4.1% in Dec), reflecting weaker price gains in meat, fish & seafood and fruit categories. Vegetable prices spiked (+7.6% yoy vs. +2.5% yoy in Dec) due to high demand, and a drop in supply arising from labour shortages and inclement weather. The cost of food imports was buffered by a strong currency, a reversal of the situation in early 2017 when the ringgit weakened precipitously.

Stretching the buck on education, communications and hotels

Households got a reprieve from rising costs as Jan saw milder school fee increases, discounts for smartphones & communication equipment and cheaper hotel rates. Lower home maintenance costs offset an upward revision in natural gas tariffs for the non-power sector, which kept housing & utilities inflation unchanged at 2.2% yoy.

Inflation poised to moderate in 2018, but risks skewed to the upside

Our inflation outlook remains unchanged (+2.9% in 2018 vs. +3.7% in 2017). Risks to the price outlook include:

- higher retail fuel prices due to an increase in global oil prices,

- higher electricity tariffs in 2H18 via the imbalance cost pass through (ICPT) mechanism,

- tightening labour market conditions and strong demand growth stimulating core inflation, and

- employers passing on higher costs from foreign worker levies and the implementation of the Employee Insurance Scheme (EIS).

Monetary policy on hold for now

The next Monetary Policy Committee (MPC) convenes on 6-7 Mar, where we expect BNM to maintain the Overnight Policy Rate (OPR) at 3.25%, following the 25bp hike in Jan. We reiterate our end-2018 OPR forecast of 3.25%, implying no further interest rate increases this year, on the condition that the core inflation outlook remains benign.