Malaysia: First election promise delivered as GST struck down

HIGHLIGHTS

First election promise delivered as GST struck down

- The government will reduce the GST from 6% to 0% effective 1 Jun 2018.

- Sparse details on budget-balancing measures may spook markets as we estimate the shortfall could widen the fiscal deficit by 0.4% to1.0% of GDP in 2018.

- Oil revenue and trimming fat in opex of selected ministries are the low-hanging fruits.

- An expanded budget deficit could be mildly stimulative for the economy, particularly for households, perhaps at the expense of investment, and dampen inflation in 2018.

GST drops to 0% effective 1 Jun 2018

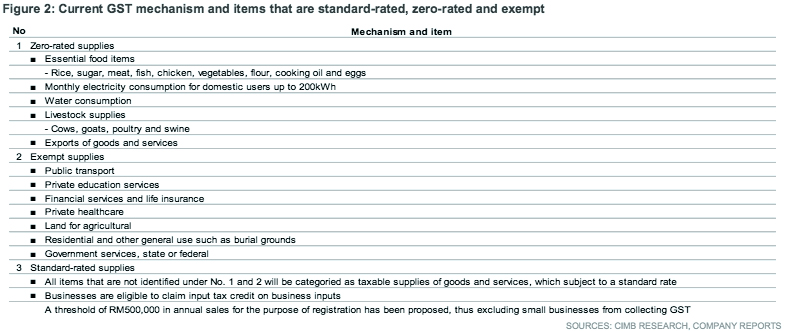

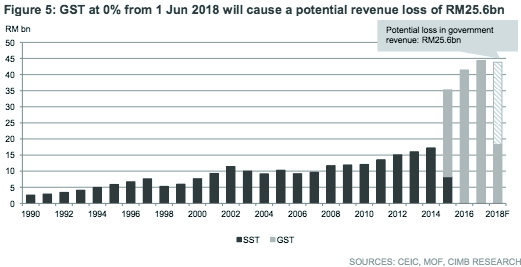

The Ministry of Finance announced that the Goods and Services Tax (GST) will be cut from the current rate of 6% to 0% with effect from 1 Jun 2018. We understand that ‘zerorating’ the GST will not require Parliamentary approval as the GST Act 2014 will be retained, together with the reporting system to improve income tax collection and reduce tax evasion. We estimate the revenue shortfall from GST removal at RM25.6bn.

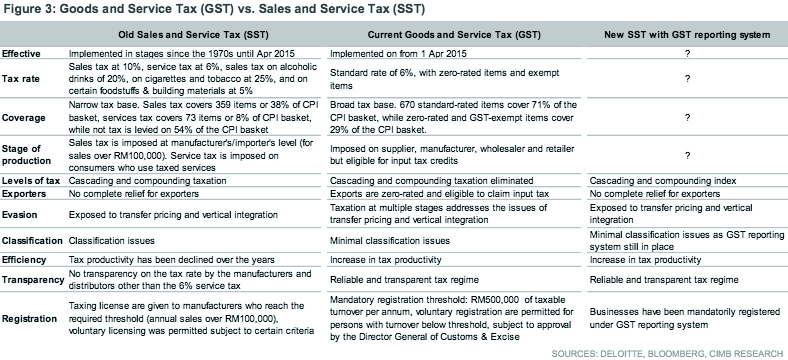

What about the Sales and Services Tax?

We were surprised by the early implementation of GST abolishment and the lack of details on budget-balancing measures. Mention of a return of a Sales and Services Tax (SST) as outlined in the Pakatan Harapan (PH) Manifesto was conspicuously absent. We believe the SST is likely to follow, though implementation and Parliamentary approval may take up to Sep, limiting revenue contribution to an estimated RM7.6bn.

Windfall from higher oil prices partly funds fixed petrol prices

Fortuitously, oil prices have rallied strongly this year, with YTD Brent at US$70/bbl, yielding an additional RM5.4bn in oil revenues for the government. Data from OPEC shows that the global oil glut has been largely eliminated and producers are exceeding output reduction targets, putting a floor on global prices. We estimate the directive to freeze retail fuel prices indefinitely will cost the government about RM2bn-3bn in 2018.

Parsing clues from PH Alternative Budget for next course of action

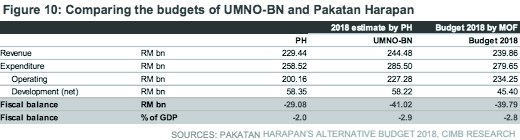

The government exceeded actual non-oil revenue collection targets in 1Q18 on sustained economic growth and aggressive tax collection tactics. While the PH Alternative Budget 2018 [PDF] has promised to ease up on raids targeting the rakyat, non-oil revenue could still exceed the target by RM4bn-5bn through higher interest and investment income, particularly from Khazanah (+RM1.5bn) and other investments (+RM2.3bn). That said, some revenue targets look too ambitious, particularly those linked to substantial hikes in property and car purchases (‘Others’ in Fig 1).

Trimming the fat may yield some near-term savings

Similarly, projections to eliminate operating expenditure (opex) of up to RM15.8bn appear stretched to us. Aiming for low-hanging fruits like trimming the fat from bloated ministries and agencies, such as the Prime Minister’s Department (see Fig 20-22), and eliminating duplication of functions among ministries and agencies could reasonably slash RM5bn6bn in opex. If PH struggles to prevent the current balance (revenues less opex) from widening, the blade may fall on the RM46bn allocation for development expenditure.

Prospects for fiscal savings are more promising in the medium term

Supplies and services, totalling RM33.6bn in 2018B, have ample scope for re-negotiation of concessions and contracts but are unlikely to be expedient enough to take effect this year. Likewise, recoveries from governance lapses and corruption could yield significant returns to the government but after potentially lengthy legal processes, if forced to ‘go by the book’. However they provide a high base from which to cut opex for Budget 2019.

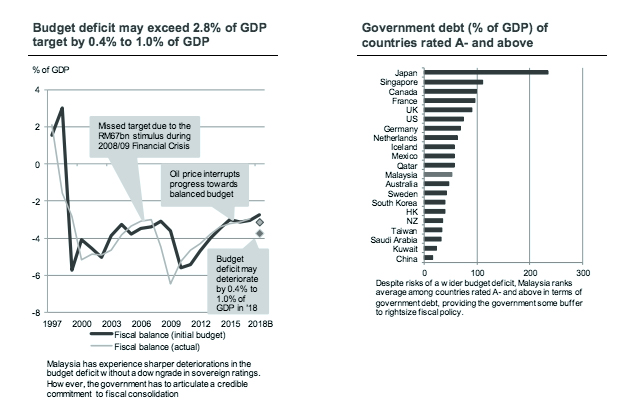

Neutralising GST impact is possible but hard to achieve

The policy change was announced via a one-page press release and the lack of details is likely to concern markets. The government has several avenues to balance the fiscal impact of GST and fuel subsidies but we think ultimately it will exceed the targeted 2.8% of GDP budget deficit by 0.4% to 1.0% of GDP (see Figs 1 and 17). The impact to our macro forecasts are subject to considerable policy uncertainty, but we generally expect an expanded budget deficit could be stimulative for GDP growth, particularly for households but perhaps at the expense of investment, and exert a one-off dampening effect on inflation, which could be enhanced by price-monitoring efforts.

APPENDIX 1: REVENUE AND EXPENDITURE ESTIMATES

Oil-related revenue:

The sensitivity of fiscal revenue to each US$1/bbl in excess of the Budget 2018 average oil price assumption of US$52/bbl is +RM300m, as provided by Ministry of Finance officials from the previous Barisan Nasional government. At the YTD average oil price of US$70/bbl, the government expects to collect additional O&G revenue of RM5.4bn.

Sales and services tax (SST):

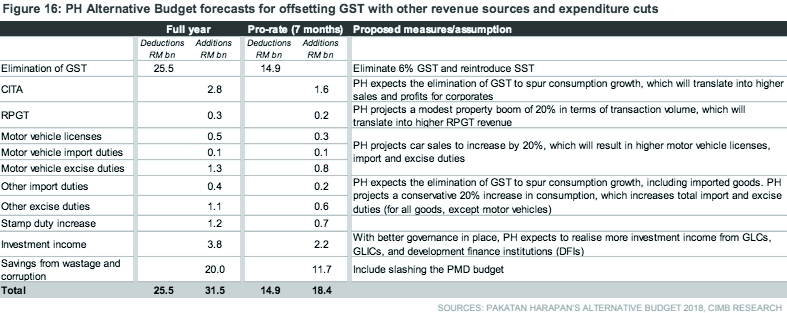

In the Pakatan Harapan (PH) Alternative Budget 2018, replacing the GST with an SST produces a shortfall of RM16.5bn (see Fig 12). Based on the Budget 2018 target GST collection of RM43.8bn, we estimate that the pro-rated GST collection in 5M18 is RM18.3bn. We think the government is likely to follow through with the introduction of an SST, though implementation and Parliamentary approval may take up to Sep, limiting revenue contribution to RM7.6bn. The sum was derived from the last available full-year collection of the SST in 2014, which totalled RM17.2bn. We then adjusted for the nominal GDP growth rate of 7.2% p.a. to obtain a full-year SST estimate in present value of RM22.8bn, or RM7.6bn when pro-rated to Sep-Dec 2018.

We expect the implementation to be much faster than the GST, which required a lead time of 1.5 years due to 1) preparations by the Royal Malaysia Customs Department and re-classification of tax codes for goods and services, and 2) substantial overhauls to financial bookkeeping processes by businesses.

Prime Minister’s Department:

The PH Alternative Budget 2018 identified potential savings of RM20bn from wastage and corruption, which includes slashing the Prime Minister’s Department (PMD) budget. While we think projections to eliminate operating expenditure (opex) of up to RM15.8bn annually appear stretched to us, we think substantial fat can be trimmed from the PMD, which has been allocated RM17.4bn in Budget 2018, comprising of RM5.2bn in operating expenditure and RM12.2bn in development expenditure. PH points to Tun Dr Mahathir’s last PMD budget as sitting prime minister of RM5bn in 2003, which adjusted for average CPI inflation of 3.5% p.a. adds up to RM8.4bn in today’s terms. Assuming the PMD has spent the proportional equivalent of the total in 5M18, it has an estimated RM10bn left to be rationalised. We estimate that the government can reasonably trim about half the amount, yielding savings of RM5bn-6bn in 2018.

Investment income:

Apart from additional dividends from Petronas due to higher oil prices, which we have factored in above together with oil-related revenue, PH believes it can increase contributions from 1) Khazanah dividends from RM1bn to RM2.5bn, and 2) other interest and investment income from RM1.7bn to RM4.0bn from returns on investments and deposits as well as asset sales (see Fig 14).

Corporate income tax and other taxes:

PH expects corporate and other tax collections to increase on the back of a virtuous cycle due to the stimulative effect that GST cuts will have on consumption and the broader economy. We are more conservative on factoring in an increase in corporate and personal income tax collection, as Prime Minister Tun Dr Mahathir has pledged to return taxes and penalties paid by businessmen and individuals as a result of “aggressive tax collection” methods under the previous government. Moreover, we believe the assumptions for significant recoveries from property transactions and car sales of 20%, underpinning an estimated revenue increase of RM4.9bn, may be too optimistic. These include the Real Property Gains Tax, stamp duties and duties on motor vehicles. Therefore, we have attached a lower probability to these sources of potential revenue increases.

Originally published by CIMB Research and Economics on 17 May 2018.