Malaysia: February 2018 trade

HIGHLIGHTS

February 2018 trade

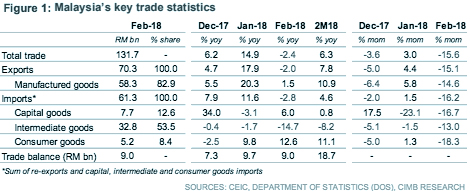

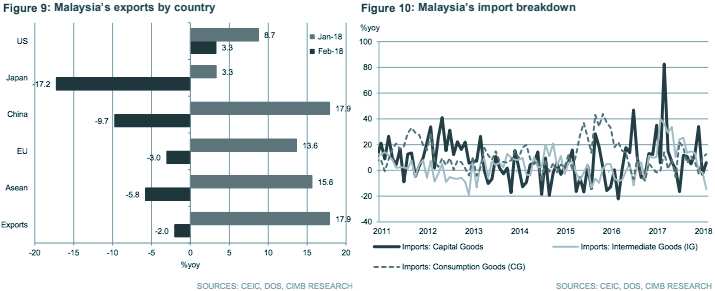

- Malaysia’s trade surplus narrowed to RM9.0bn in Feb as exports (-2.0% yoy) and imports (-2.8% yoy) recorded the first contractions in 16 months.

- While seasonal shutdowns and a high base for commodity prices had exaggerated Feb’s deterioration in exports, underlying trends in external demand growth are easing.

- Our export growth forecast of 9.8% for 2018F is unchanged assuming that US-China trade tensions de-escalate and a compromise is reached on the announced tariffs.

Trade surprises on the downside

Total trade activity in Feb surprised on the downside (-2.4% yoy vs. +14.9% yoy in Jan), as the seasonal impact of a shorter working month was more pronounced than expected. Gross exports fell 2.0% yoy (CIMB: +4.2% yoy, Bloomberg consensus: +8.0% yoy; Jan: +17.9% yoy), the first decline in 16 months, but milder than the 2.8% yoy decline in gross imports (CIMB: +4.5% yoy, Bloomberg consensus: +7.1% yoy, Jan: +11.6% yoy). A smaller gap in the growth rates between the two led to a narrower trade surplus of RM9.0bn in Feb (CIMB: +RM8.9bn, Bloomberg consensus: +RM8.5bn, Jan: +RM9.7bn).

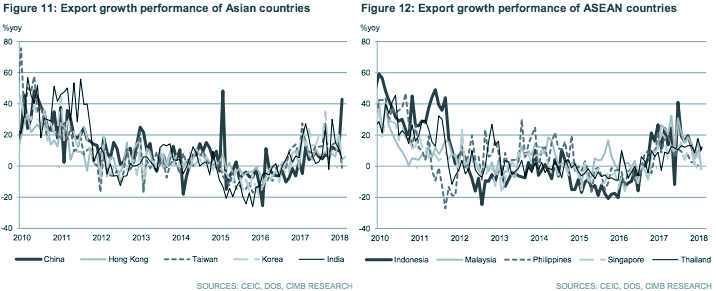

Second-worst performer among the Asian countries

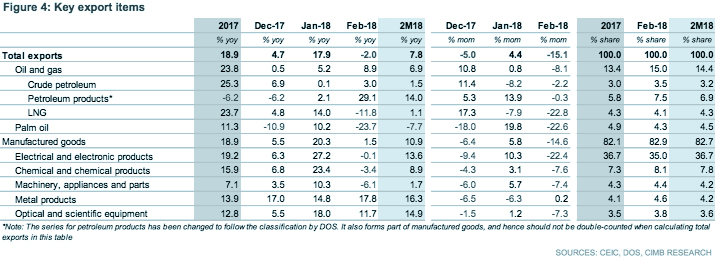

Malaysia’s export deterioration was sharper than those of its Asian peers, led by a slowdown in the manufactured segment, of which about 60% of sub-segments recorded negative growth in Feb: electrical and electronics (E&E, -0.1% yoy in Feb vs. +27.2% yoy in Jan), chemicals (-3.4% yoy vs. +23.4% yoy in Jan) and machinery (-6.1% yoy vs. +10.3% yoy in Jan). That said, Malaysia was one of the better-performing exporters in Jan.

Non-oil commodity exports dragged down by weaker prices

Furthermore, weaker volumes and prices dragged down palm oil (-23.7% yoy in Feb vs. +10.2% yoy in Jan), liquefied natural gas (LNG) (-11.8% yoy vs. +14.0% yoy in Jan) and natural rubber (-40.1% yoy vs. -26.0% yoy in Jan) shipments. On the bright side, strong oil price continued to support export performance of crude petroleum (+3.0% yoy in Feb vs. +0.1% yoy in Jan) and refined petroleum products (+29.1% yoy vs. +2.1% yoy in Jan). As the gains in oil exports dominated those of gas, oil and gas (O&G) exports accelerated further in Feb (+8.9% yoy vs. +5.2% yoy in Jan).

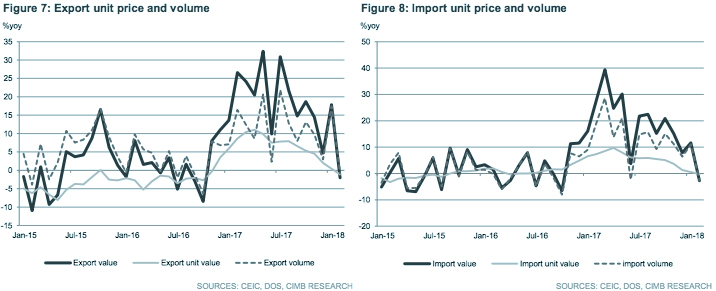

First dual contraction in export prices and volumes since Oct 2016

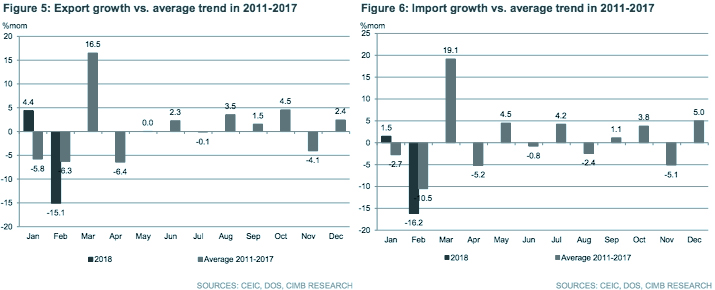

Declines in the export unit value (-1.1% yoy) and volume indices (-0.8% yoy) weighed on Feb exports. Export prices declined yoy in Feb on weaker non-oil commodity prices, while the volume contraction coincided with seasonal downtime for large swathes of Asia’s supply chain over the Chinese New Year. We are not overly concerned about the export contraction as we expect seasonal effects to fade in Mar. Nonetheless, YTD export growth, which smoothens out the seasonal distortions, indicates momentum is slowing (+7.8% yoy in 2M18 vs +12.4% yoy in 4Q17). Malaysia’s manufacturing PMI declined to a 5-month low of 49.5 pts in Mar (49.9 pts in Feb), reflecting weaker output and new orders. The new export orders index fell further in Feb to a 15-month low, reinforcing recent trends of moderating external demand growth.

We expect calmer heads to prevail in US-China trade conflict

We maintain our 2018F export growth forecast of 9.8% (+18.9% in 2017) on the basis of: 1) moderating global demand growth for electronics, 2) commodities’ terms of trade headwinds, 3) normalisation of plantation crop production growth, and 4) the translation effects of a stronger ringgit. Trade tensions between the US and China is a possible downside risk, although Malaysia’s diversified export structure offers some degree of protection against targeted tariffs. Our base case scenario assume that the US and China will reach a compromise, resulting in a de-escalation of tariff threats.

Originally published by CIMB Research and Economics on 05 April 2018.