Malaysia: February 2018 consumer price inflation

HIGHLIGHTS

February 2018 consumer price inflation

- Headline inflation eased sharply to 1.4% yoy in Feb, due to diminishing food inflation and deflation in the clothing, transport and communication price indices.

- Our inflation outlook remains unchanged at 2.9% in 2018, as we think Feb’s headline print likely marks the trough for the year.

- We expect no further OPR hikes this year as core inflation remains subdued.

Lowest headline inflation since Oct 2016

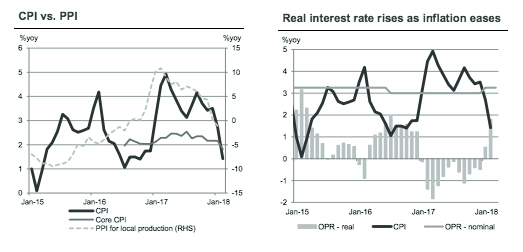

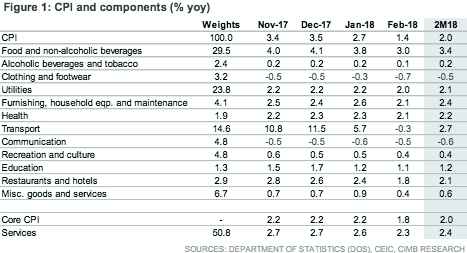

Malaysia’s consumer price inflation eased sharply again in Feb to 1.4% yoy (CIMB: +1.9% yoy, Bloomberg consensus: +1.9% yoy, +2.7% yoy in Jan), marking the lowest reading since Oct 2016. Sequentially, the seasonally adjusted headline CPI was flat in Feb (+0.3% mom in Jan). Core inflation cooled further to 1.8% yoy in Feb (+2.2% yoy in Jan), indicating that underlying demand pressures are not threatening yet.

Deflation in fuel prices a drag on headline inflation

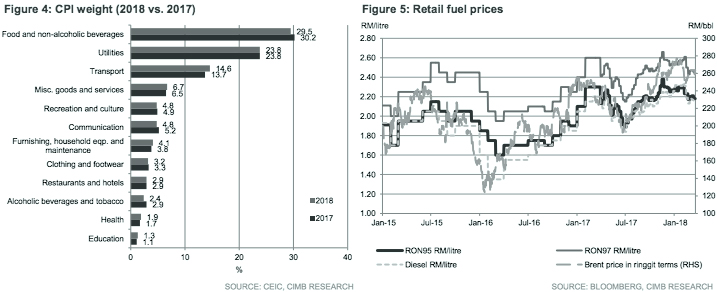

The transport index slipped into deflation in Feb (-0.3% yoy vs. +5.7% yoy in Jan), for the first time since Dec 2016 as the fuel index declined 1.6% yoy (+8.5% yoy in Jan). Fuel prices, which now account for 8.5% of the CPI in 2018 (7.8% in 2017), are expected to remain a drag on transport prices in Mar, as average retail fuel prices have fallen 2.6% to 3.2% mom over the period 1-21 Mar.

CNY food inflation more modest than recent years

Food inflation moderated to 3.0% yoy in Feb (+3.8% yoy in Jan), as price gains of food consumed at home and food away from home both eased. Ahead of this year’s CNY period, food prices rose by a cumulative 1.8% versus 3.2% in 2017 and 2.0% in 2016. Key grocery items that recorded more muted gains this year included rice, meat, fresh fish, vegetable oil, fruits, fresh vegetables and spices. Aside from the festive season price controls and government initiatives such as KR1M 2.0, the stronger ringgit (+13.5% yoy in Feb) was a major factor in helping to alleviate the cost of imported foods.

Broad-based moderation in non-food and transport inflation

Beyond the volatile food and transport price components, inflationary pressure also generally weakened across the economy. Prices of clothing and communication equipment remain mired in deflation. Services inflation moderated again to 2.3% yoy in Feb (+2.6% yoy in Jan), reflecting gentler mark-ups in costs of household services, healthcare, and education.

Feb potentially marks the trough for headline inflation in 2018

Feb’s print likely marks the lowest point for headline inflation in 2018, as we maintain our headline inflation forecast of 2.9% in 2018 (+3.7% in 2017). However, we believe the previously cited upside risks to our inflation outlook have moderated, including:

- higher retail fuel prices,

- higher electricity tariffs, and

- faster wage growth and core inflation.

Weak inflation pulls the brake on further OPR hikes

Muted inflation readings, coupled with less upbeat trends in the manufacturing sector, tones down Bank Negara Malaysia’s (BNM) appetite for a second Overnight Policy Rate (OPR) hike. The next policy decision is due on 10 May, where we expect the Monetary Policy Committee (MPC) to maintain the OPR at 3.25%. We reiterate our end-2018 OPR forecast of 3.25%, implying no further interest rate increases this year.

Originally published by CIMB Research and Economics on 21 March 2018.