Malaysia: Economic Focus

HIGHLIGHTS

Striking the right balance

- Key elements to watch in Budget 2019: Detailed fiscal framework, spending adjustments and revenue enhancements, like asset sales and taxes.

- Budget deficit to widen to 3.5-3.7% of GDP in 2018-19 due to one-off tax refunds, which mask sustained fiscal consolidation from expected cost cuts.

- Fiscal constraints are transitory, as budget deficit set to narrow briskly after 2020 (11MP target: -3.0% of GDP) if fiscal adjustments are implemented.

- 11MP GDP growth target revised lower but still-resilient at 4.5-5.5% in 2018- 20 as government maintains pro-growth policy stance.

Budget 2019 to reflect dual priorities of fiscal discipline and growth

Budget 2019, the first under the new Pakatan Harapan (PH) government, will be tabled on 2 November 2018. While billed as a “difficult budget”, the Ministry of Finance (MOF) has stated that the government in not pursuing austerity and is maintaining a pro-growth stance, which it aims to achieve by balancing cost reductions with more targeted spending, efficiency gains and governance reforms. Detailed adjustment plans backed by a strong fiscal framework can instil market confidence that government will remain financially disciplined. Markets are also watching for potential revenue enhancements, including asset sales and new taxes.

Fiscal space can be created through determined spending cuts

In our view, the government has room to make fiscal adjustments via spending cuts without hurting growth prospects unduly if wastages and leakages are curbed. We think operating and development expenditures can be trimmed by RM7bn in Budget 2019 due to tighter procurement procedures, zero-based budgeting, reviews or deferment of infrastructure projects, more targeted subsidies and cash transfers, and revisions in supply and services contracts, which could limit the need for aggressive revenue-raising measures and steeper cuts to productive areas of spending.

Don’t miss the forest for the trees

GDP growth prospects, despite being lowered to 4.5-5.5% in 2018-2020F in the MTR (CIMB: +4.7% in 2018 and 2019) remain supportive of economic activity and labour market conditions. We argue that near-term fiscal adjustments should not detract from the reforms undertaken to reduce total public debt, strengthen government finances and address structural bottlenecks that form the basis of sustainable long-term growth.

GOVERNMENT FINANCE

Bracing for a difficult Budget 2019

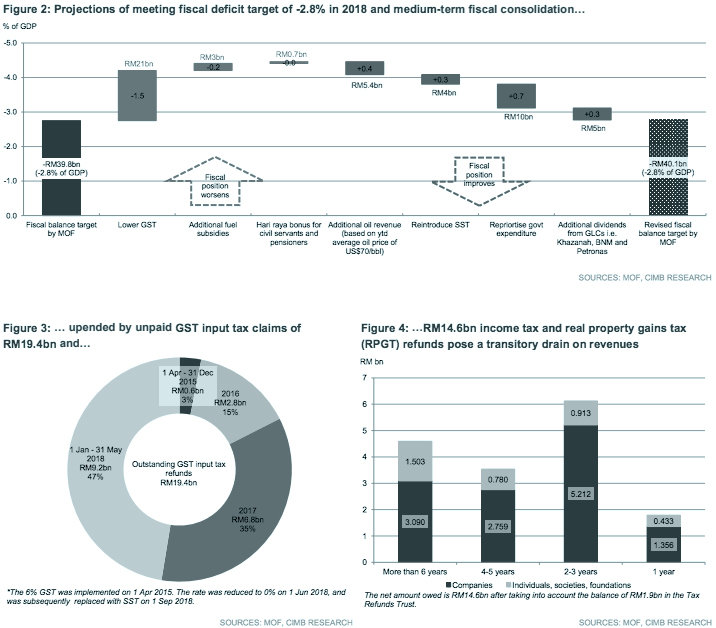

Budget 2019, the first under the new Pakatan Harapan government, will be tabled on 2 November 2018 in what the Minister of Finance Lim Guan Eng has billed a “difficult budget”, as the Ministry of Finance (MOF) normalises government finances a period of two to three years. The MOF may miss initial projections in May to maintain the 2018 budget deficit target of -2.8% of GDP, which were based on the assumptions that additional oil-related revenue, higher GLC dividends, proceeds from the Sales and Service Tax and expenditure cuts would offset the impact from the zero-rating of the GST, petrol subsidies and the Hari Raya Special Assistance (see Fig 2). The pro-rated fiscal deficit as at 8M18 stood at -3.4% of GDP (82.7% of 2018B target) as revenue collection had fallen behind projections (60.6% of 2018B target) while reducing operating expenditure has proven tricky in the short term (76.1% of 2018B target). Barring a sharp reversal in 4Q18, divergent revenue and operating expenditure trends may cause the current balance to dip into a deficit in 2018.

Our base case scenario projects the budget deficit widening to -3.7% of GDP in 2018F and -3.5% of GDP in 2019F, due principally to the post-GST revenue adjustments and the recognition of one-off GST and income tax refunds.

- The zero-rating of the Goods and Services Tax (GST) on 1 Jun 2018 will slash fiscal revenue collection by RM21bn in 2018. The introduction of the Sales and Services Tax on 1 Sep is expected to result in the collection of RM4bn. In 2019, we estimate the shortfall between GST and SST revenue to be RM22bn.

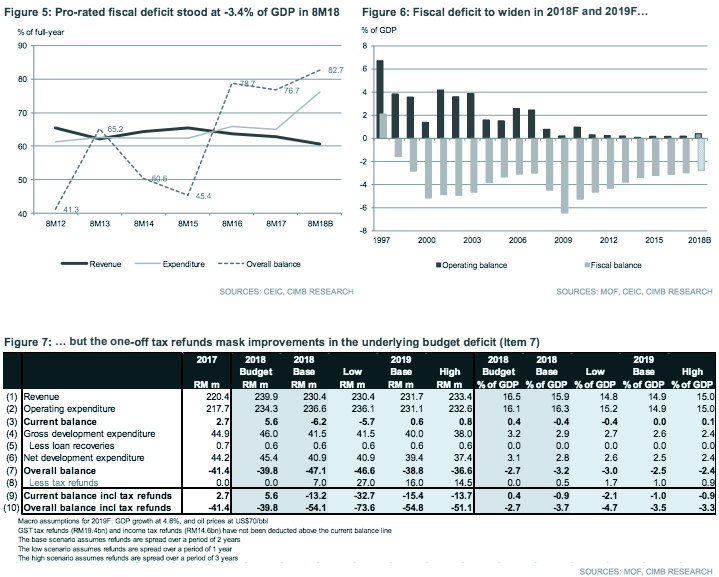

- GST input tax refunds of RM19.4bn spread over 2-3 years.

- Corporate, personal income and real property gains tax refunds totaling RM14.6bn as at end-May 2018. The Ministry of Finance has allowed applications for the claims to be offset against income tax payable in FY2018, reducing tax collection in 2018F and 2019F.

The temporary deviation has been necessary to repair public finances and should not be mistaken as a sign of profligacy. In fact, if the tax refunds were excluded, our estimates suggest that the government would have adhered to its fiscal rule of running a positive current balance in 2019F (item 3 in Fig 7), while curtailing the budget deficit to -3.2% of GDP in 2018F and -2.5% of GDP in 2019F (item 7 in Fig 7). In particular, our projections for Budget 2019 assume:

- Opex rationalisation (-RM5.5bn in 2019F), which we expect to materialise more prominently in 2019 following the implementation of zero-based budgeting, tighter procurement procedures, more targeted subsidies and cash transfers, and revisions in supply and services contracts. Efficiency gains and lower fiscal leakages would diminish the need for aggressive revenue-raising measures and steep cuts to productive areas of spending. The Public Finance Committee (PFC), consisting of Minister of Finance Lim Guan Eng, Minister of Economic Affairs Datuk Seri Azmin Ali and BNM Governor Datuk Nor Shamsiah, has been tasked with steering the medium term fiscal consolidation effort.

- Lower development expenditure (-RM1.5bn in 2019F). Under the MTR, the government has cut the development expenditure budget by RM40bn to RM220bn in 2016-2020. The delays or cancellations of infrastructure projects are likely to reduce development expenditure. Allocations are likely to skew in favour of policies promoting inclusive income growth, welfare spending, affordable housing, infrastructure upgrades, healthcare and education.

- Revenue optimisation and taxes (+RM3.0bn in 2019F). Our projections suggest that oil-related revenue (based on a Budget 2019 oil price assumption set at US$70/bbl), GLCs dividends, and asset monetisation can make up a large portion of the revenue shortfall from the GST rollback. However, to create revenue contingencies, the government may opt to introduce certain types of taxes to align industry incentives or even the playing field (digital or e-commerce tax) or promote desired social and economic outcomes (sin taxes, soda or sugar tax, carbon or congestion tax). In our view, other taxes aimed at facilitating income redistribution (inheritance tax, property taxes, and income tax hikes for the rich and capital gains tax) may be more appropriately considered as part of a holistic tax reform under the Tax Reform Committee (TRC), to ensure such taxes do not reduce the incentives to invest, create wealth, and promote entrepreneurship in Malaysia. The TRC Tax Reform Committee has been tasked to review and reform Malaysia’s tax regime into a more efficient, neutral and progressive system.

The revenue-expenditure projections suggest that a budget deficit target of – 3.0% of GDP in 2020, recently revised in the 11MP Mid-term Review (MTR), and subsequent fiscal consolidation are achievable, in our view. Importantly, debt dynamics remain favourable, with the public debt to GDP ratio expected to gradually decline over the long term, even if federal net borrowing increases in 2018F and 2019F, as the growth rate of contingent liabilities is likely to moderate amid ongoing reviews of off-balance sheet financing in government-initiated projects.

MID-TERM REVIEW OF 11TH MALAYSIA PLAN

Key takeaways

- Downward revision in 2018 growth targets to 4.5-5.5% in 2018-2020F from original target of 5.0-6.0% in 2016-2020 (CIMB: +4.7% in 2018 and 2019), due to lower contributions from private investments and the public sector, which were partly offset by higher projections for household consumption. By industries, growth forecasts were downgraded across all sectors, except the consumer-driven wholesale and retail trade, accommodation and restaurants.

- Capital contribution to growth expected to decline, partly offset by labour and multifactor productivity.

- Development expenditure. Government to build 200,000 affordable homes, and upgrade education and healthcare facilities. Upgrading 1,500km of rural roads. More allocation to promote development in Sabah, Sarawak, Kelantan, Terengganu, Kedah and Perlis. Proposal to establish National Healthcare Policy, including Healthcare Financing Scheme for B40 group.

- National Policy Framework on Fourth Industrial Revolution (4IR) to increase productivity and competitiveness of manufacturing sector.

- Government to improve market efficiency by streamlining state-owned enterprises and monopoly entities.

- Governance reforms. Two-term limit on Prime Minister, Chief Minister and Menteri Besar to deter excessive concentration of power. Lowering of voting age to 18 from 21. Separation of Attorney General’s office from Public Prosecutor’s office to strengthen jurisprudence. Ombudsman Malaysia to be established to independently investigate complaints against government agencies.

- Human capital. Reduce dependency on foreign workers via automation and multi-tiered levies. Reviewing National Policy on Science, Technology and Innovation. Increase women’s participation in workforce.

Originally published by CIMB Research and Economics on 19 October 2018.