Malaysia: April 2018 trade

HIGHLIGHTS

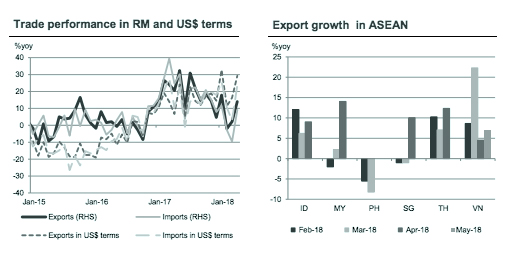

April 2018 trade

- Malaysia’s trade surplus remained strong at RM13.1bn in April, aided by pronounced gains in petroleum and manufacturing exports.

- Key risks to the trade outlook are slowing tailwinds in the global capex cycle and spillovers from US-China trade tensions, in our view.

- We lower annual export growth forecast to 7.7% (from 9.8%) and import growth by a larger margin to 5.5% (from 11%), resulting in larger trade surplus forecast for 2018F.

- The revisions boost our 2018F current account surplus estimate to 3.4% of GDP.

April’s trade growth surprised on upside…

Trade activity was resurgent in April (+11.7% yoy vs. -3.5% yoy in March) with gross exports delivering a stellar gain of 14.0% yoy (CIMB: +7.5% yoy, Bloomberg consensus: +6.3% yoy; March: +2.2% yoy). The rebound in import growth was equally sharp at +9.1% yoy (CIMB: +4.3% yoy, Bloomberg consensus: +3.8% yoy, March: -9.6% yoy), resulting in a healthy trade surplus of RM13.1bn (CIMB: RM11.4bn, Bloomberg consensus: RM12.8bn, RM14.7bn in March).

…with gains in downstream petroleum pad O&G exports…

A lumpy gain in refined petroleum products (+38.9% yoy vs. -8.6% yoy in March) due to a low base and stronger shipments of crude petroleum (+22.7% yoy vs. +18.4% yoy in March) from an increase in external demand and higher oil prices drove the improvement in oil and gas (O&G) exports (+17.0% yoy in April vs. +0.4% yoy in March). We expect the annual gain in refined petroleum products to moderate sharply in May. Meanwhile, the contraction of LNG exports deepened (-12.5% yoy in April vs. -3.3% yoy in March), reflecting: 1) lower volumes due to the ramp-up of output at several fields in 1H17 and production declines this year, and 2) falling unit prices.

… and recovery in manufacturing exports exceeding expectations

Key sectors, which have driven manufacturing exports (+16.8% yoy in April vs. +3.7% yoy in March) since 1Q17, rebounded convincingly after a lacklustre post-CNY recovery in March: E&E (+21.2% yoy in April vs. +8.8% yoy in March), chemicals (+17.8% yoy vs. -21.0% yoy in March), machinery (+6.2% yoy vs. +3.6% yoy in March), optical and scientific equipment exports (+7.7% yoy vs. -0.2% yoy in March). Apart from the usual suspects, exports for metal products, road vehicles and other transport equipment surprised on the upside.

Import performance lifted by capital goods

The imports of capital goods recorded a 4.8% yoy gain in April after a steep decline in March that was exacerbated by a high base effect. On the other hand, the pace of contraction eased for intermediate goods (-11.9% yoy in April vs. -14.5% yoy in March) and consumer goods (-1.8% yoy vs. -12.5% yoy in March). We think domestic demand for imports of consumer goods is likely to increase in the next few months due to seasonally higher demand during the Ramadan month and Hari Raya celebrations, as well as the spurt in consumer spending in the period between the reduction of the Goods and Services Tax (GST) to 0% on 1 Jun and the reintroduction of Sales and Services Tax (SST) on 1 September.

Revision to trade outlook boosts net export contribution in 2018F

Malaysia’s stronger export growth in April echoed similar trends in ASEAN (Indonesia, Singapore and Thailand) but was at odds with the weaker manufacturing PMI (47.6 pts in May vs. 48.6 pts in April) that pointed to drag from lower output and new export orders. We have pared our gross export estimate for 2018F to 7.7% (from +9.8% initially) to reflect a weaker prognosis for manufactured exports and spillover from global trade tensions in 2H18. However, even more aggressive downward adjustment to our gross import forecast to 5.5% (from +11.0%) implies higher net trade contribution in 2018F, underpinning a higher current account surplus forecast of +3.4% of GDP this year (from +2.8% of GDP).

Originally published by CIMB Research and Economics on 17 May 2018.