Malaysia: 2Q18 GDP and current account

HIGHLIGHTS

2Q18 GDP and current account

- Malaysia’s economy expanded by 4.5% yoy in 2Q18, the weakest since 4Q16, partly due to supply shocks in agriculture (palm oil and rubber) and mining (natural gas).

- We downgrade our forecast for GDP growth to 4.7% in 2018 (vs. +5.2% previously), which is lower than BNM’s revised estimate of 5.0% (vs. 5.5-6.0% previously).

- Fiscal and monetary options are constrained, putting the onus on the government to provide policy clarity and accelerate reforms to stimulate the economy.

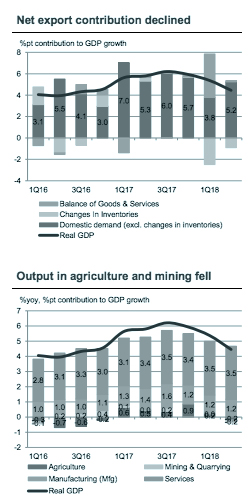

A big miss in 2Q18 GDP growth

2Q18 GDP growth upended market expectations at 4.5% yoy (CIMB: +4.9%, consensus: +5.2%, 1Q18: +5.4%), the slowest pace since 4Q16. The contribution of net exports narrowed sharply (+0.1% pt in 2Q18 vs. +4.0% pts in 1Q18) as imports rebounded to meet stronger domestic demand (+5.2% yoy in 2Q18 vs. +3.8% yoy in 1Q18). Improvements in private consumption and investments were reflected by sustained growth in the domestic-oriented manufacturing and services sectors. While election spending boosted public consumption, public investment stalled as several large projects neared completion while development expenditure and megaprojects stalled post GE14.

Supply shocks to plantation crop and O&G sector

Supply disruptions in agriculture and mining dented contributions from the primary industries in 2Q18. In the agriculture sector, production of palm oil and rubber fell by 6% yoy and 20% yoy, respectively, due to supply bottlenecks, shortage of workers and adverse weather. Weak palm oil output also cascaded down to the downstream edible oil manufacturing segment. Meanwhile, the oil and gas (O&G) sector was hit by natural gas production outages in East Malaysia.

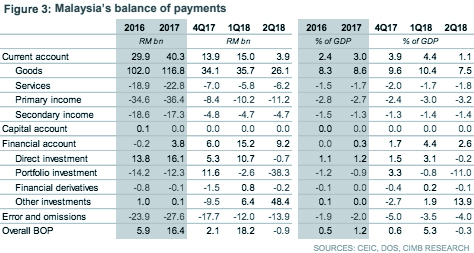

Stronger imports narrow the current account surplus

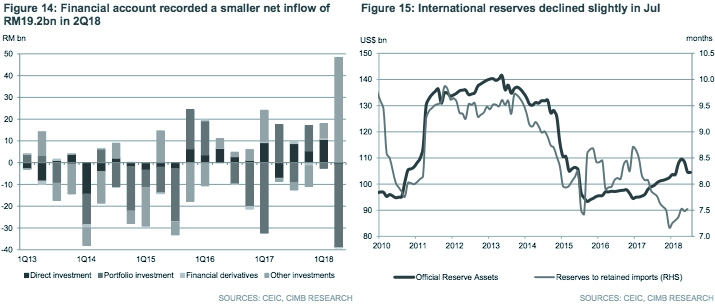

The pick-up in domestic demand resulted in the current account (CA) surplus falling sharply to RM3.9bn or 1.1% of GDP in 2Q18 (+RM15.0bn or 4.4% of GDP in 1Q18) on the back of a narrowing goods surplus and higher deficits in the services and primary income accounts. The financial account also recorded a smaller surplus (+RM9.2bn in 2Q18 vs. +RM15.2bn in 1Q18) as higher placements of currency and deposits with domestic financial institutions offset large net foreign portfolio outflows.

Growth trajectory slowing more than initially anticipated

Benefiting from a temporary tax holiday and labour market improvements, consumers are poised to take over the economic mantle as other growth engines lose velocity, particularly in the public sector. Apart from revenue forgone due from the Goods and Services Tax (GST), government spending will be further curtailed by recent revelations of unpaid GST claims to businesses amounting to RM19.4bn, which the Ministry of Finance has deferred until 2019. Moreover, supply disruptions in agriculture and mining are expected to linger for the rest of the year while the manufacturing outlook is clouded by external headwinds. To reflect these adverse developments, we have downgraded our GDP growth forecast to 4.7% in 2018 from 5.2% previously, shy of Bank Negara Malaysia’s (BNM) revised estimate of 5.0% (vs. 5.5-6.0% previously).

Tough choices lie ahead as policy space constrained

To maintain macroeconomic stability, BNM’s preference likely tilts to keeping the Overnight Policy Rate (OPR) unchanged for an extended period. Unless inflation remains weak, we think room for BNM to loosen monetary policy to stimulate demand is constrained by the uptrend in US interest rates and lower market tolerance for deteriorating current accounts. Fiscal options to stimulate Malaysia’s economy are limited amid budgetary constraints, placing greater urgency on the government to provide policy clarity and accelerate meaningful reforms to unleash productivity growth.

Originally published by CIMB Research and Economics on 3 August 2018.