Malaysia: 1Q18 GDP and current account

HIGHLIGHTS

1Q18 GDP and current account

- Malaysia’s economy expanded by 5.4% yoy in 1Q18 (+5.9% yoy in 4Q17), on the back of weaker growth in government consumption and investments.

- The policy environment has altered following Pakatan Harapan’s victory in GE14.

- A bias for fiscal expansion is seen as positive for growth prospects but may prompt BNM to reassess the impact of its monetary policy stance on the country’s policy mix.

- External financing conditions improved as both the current account and financial account surpluses widened.

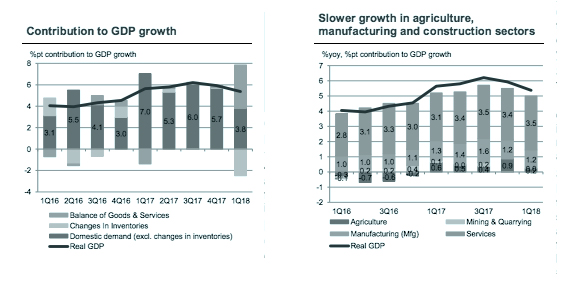

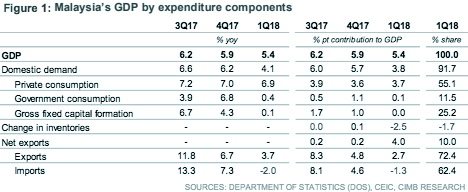

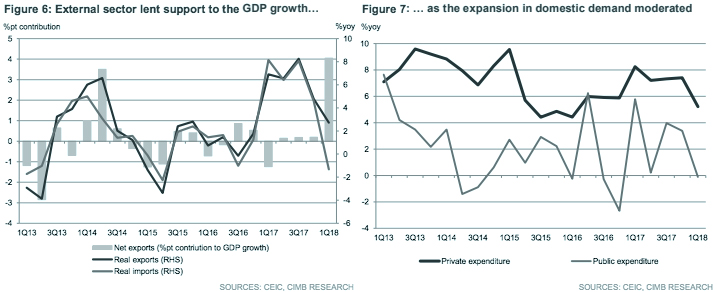

GDP growth moderates to 5.4% yoy in 1Q18

Malaysia’s GDP rose 5.4% yoy in 1Q18 (CIMB: +5.6%, consensus: +5.6%, 4Q17: +5.9%), on the back of slower domestic demand (+4.1% yoy in 1Q18 vs. +6.2% yoy in 4Q17), particularly government consumption (+0.4% yoy in 1Q18 vs. +6.8% yoy in 4Q17) and investments (+0.1% yoy in 1Q18 vs. +4.3% yoy in 4Q17). The bigger contribution from net trade in 1Q18 made a key difference to the topline, along with a sharp decline in imports.

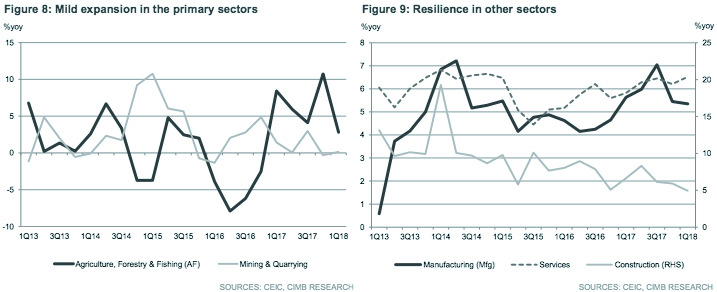

Drag from agriculture masks resilience in other sectors

Growth in agriculture buckled under the weight of a lofty benchmark in 2017, when palm oil and rubber production staged strong recoveries following El Nino in 2015-16. Contributions to headline growth were broadly similar in the other segments, suggesting that the economy is not losing steam, merely casting off the one-off boost from plantation crops in 2017. The service sector grew at a faster pace (+6.5% yoy in 1Q18 vs. +6.2% yoy in 4Q17) thanks to a pickup in the insurance sector.

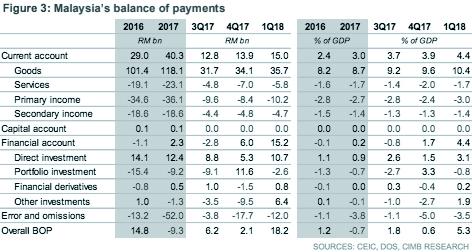

Strong trade position lifts current account

The current account (CA) surplus widened markedly to RM15.0bn or 4.4% of GDP in 1Q18 (+RM13.9bn in 4Q17) due to a higher goods surplus and a narrower services deficit. The financial account more than doubled qoq (+RM15.2bn in 1Q18 vs. +RM6.0bn in 4Q17) due to an influx of net direct investment and other investment. Conducive global market conditions encouraged Malaysians to invest overseas, which sank the portfolio account to a deficit of -RM2.6bn in 1Q18 (vs. +RM11.6bn in 4Q17).

Sea change after GE14

Following the upheaval in GE14, when Pakatan Harapan (PH) usurped Barisan Nasional, the only political coalition to have governed Malaysia since independence, the dust is settling on a changed policy landscape. On 16 May 2018, the Ministry of Finance announced the reduction of the Goods and Service Tax (GST) from 6% to 0%, and followed up with a statement on 17 May 2018 indicating that the Sales and Service Tax (SST) will be re-introduced, in addition to other revenue and expenditure measures which will be announced in due course. “Fiscal responsibility, transparency and governance will be a paramount consideration in the rolling out of fiscal reform,” said the ministry.

Macro forecasts unchanged while awaiting policy clarity

While awaiting the government’s announcements of further fiscal reforms, we maintain our 2018 GDP growth forecast of 5.2%. The GST cut is likely to shift inflation onto a shallower upward trajectory in 2H18, and reinforces our expectations for the OPR to remain unchanged at 3.25% in 2018. We are also keeping an eye out for the budget-balancing policies. If the government’s fiscal policy stance skews towards being too expansionary, Bank Negara Malaysia (BNM) may need to reassess the impact of its monetary policy stance on the country’s policy mix.

Originally published by CIMB Research and Economics on 17 May 2018.