Making trade great again: The misplaced reliance on the Asian consumer

ASEAN exports are showing signs of life after a dismal performance in 2016. However, the cyclical bounce aside, there are still significant structural issues that are likely to constrain its growth: The slowdown in the Chinese economy1 and its continued rebalancing away more import-intensive investment demand toward consumption; China’s greater on-shoring of production; and the maturation of global supply chains. Besides that, investment demand globally remains soft and that has been the biggest driver of ASEAN exports.

Moreover, protectionism has been on the rise and, if Mr Trump’s campaign rhetoric is to be believed, it will only rise further. Not surprisingly, global trade now grows at almost the same pace as global output, while a decade or so ago, it was growing at about twice the rate.

But this is not a report about exports per se; I will get to that later. It is about what will drive ASEAN economic growth as exports go through an adjustment. The usual answer is “consumption’ and the evidence provided is invariably anecdotal: cafes and bars full of young people, booming online shopping (hey! look at Alibaba), or simply the growth of services. If someone visits Ho Chi Minh City or Jakarta, the trip review usually has a “there is a buzz” embedded in it somewhere.

Is domestic consumption driving growth? Quantifying the claim

The evidence though is a little bit different. To make the case that “consumption is driving growth”, we need to try and quantify the claim, rather than simply eyeballing how many lattes appear to be selling at the local coffee shop. At the very least, consumption should be growing faster than GDP, or consumption as a percentage of GDP should be rising. That is the minimum requirement. But it doesn’t end there. Even if consumption as a percentage of GDP is rising, at least two more things need to be checked.

First, as it is possible that consumption’s share in GDP is rising not because consumption is doing great, but because some other part of the economy is doing poorly. As such, we need to see if the growth rate of consumption is actually increasing. And second, we need to check if the rise in consumption is sustainable. That, in turn, requires a couple of additional checks: As consumption is financed either out of income or savings, we need to check whether the share of labour in GDP is rising or if the savings rate is falling2.

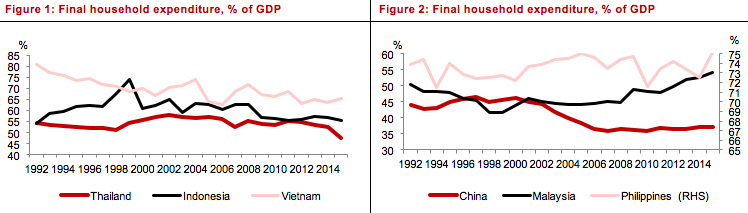

In Thailand and Indonesia, the consumption to GDP ratio has been steadily declining; continuously in Thailand and almost similarly in Indonesia though there was small upward bump between 2011 to 2013. Vietnam is a bit trickier where a declining medium term trend seems to have been interrupted and there has been a steady uptick from 2012 onward, with the ratio rising from 63.8% to 65.1%.

Source: World Bank

The ratio in China appears to be rising steadily, though very modestly, from 35.8% in 2007 to 37% in 2015. This may come as a surprise to some as the Chinese have consumption-led growth as an explicit goal, Moreover, consumption is starting from a low base, where the consumption ratio is comfortably below that of the other countries. As such, one would have expected a larger increase. If anything, the Chinese experience provides an uncomfortable hint about how difficult it is for an economy to move to consumption-led growth. More on that later.

There are two countries where the ratio has been rising meaningfully – Malaysia and Philippines – and let’s see if they pass the next test: How has consumption growth been behaving?

Source: World Bank

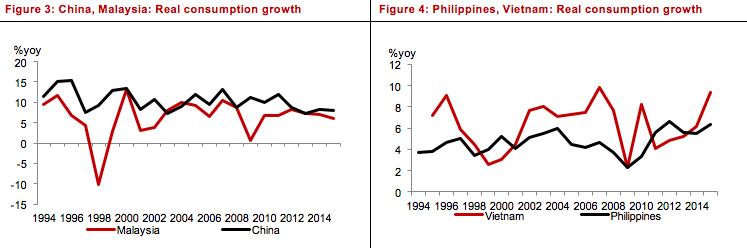

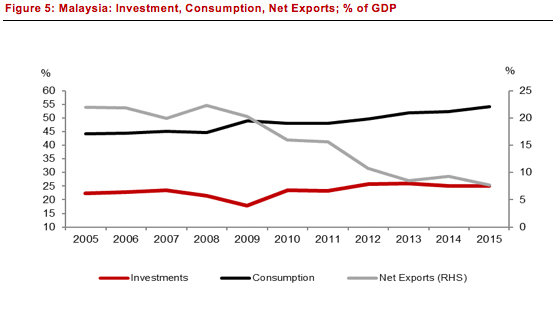

Judging by the second criteria, Malaysia drops out as consumption growth has been moderating over the past few years. Consumption to GDP ratio has been rising largely because trade has been floundering. The importance of exports to the economy has declined since the Global Financial Crisis (GFC) and the end of the commodity boom and is down to approximately 70% from over 110% in 2009. Similarly, imports have also declined, albeit by less, and consequently, as the chart below shows, there has been a huge fall in the share of net exports.

Consumption and investment growth have not been robust, but their share in GDP has gone up largely because the share of net exports has declined. Consumption is not driving growth, though one can legitimately say that it has been resilient in the face of external shocks and has helped cushion overall growth.

Source: World Bank

In China, after a post crisis decline in growth, consumption growth has held steady. The two countries where consumption growth is actually booming are the Philippines and Vietnam. In the former, barring a small hiccup in 2013, the trend has been for a rising growth rate since 2009. In Vietnam, consumption is thriving with the current growth rate about double what it was in 2011.

In short, by the criteria used, we can detect modest consumer-led growth in China and in the Philippines. Consumption is flourishing in Vietnam, though it doesn’t necessarily mean that is what is driving growth. More likely, given the declining/steady consumption to GDP ratio, it is trade and direct investment that are driving growth. That, in turn, is generating income growth, which is supporting consumption.

The next question: Is it sustainable?

In different ways, the consumption stories in the Philippines and Vietnam can continue.

Source: World Bank

The savings rate has been holding steady in the Philippines, which is a good thing as it is much too low for it to start declining from its current level. Without a fall in the savings rate, the share of labour in national income needs to rise for consumption to drive growth, but there isn’t good enough data to be able to draw any strong conclusion. Our optimism comes from the current pace of growth in income and that the Philippine household is tremendously underleveraged. Both should help consumption. High household debt is also likely to constrain consumption in Malaysia and Thailand.

Source: CEIC, CIMB Research

For Vietnam, the story isn’t about consumption driving growth but more of a booming consumer, with income coming from other areas of activity. An increasing savings rate shows that the future is being secured. The demographics are good and the middle class is growing, both of which help generate consumption demand.3

A small warning though. The thriving middle class that we see and mention as anecdotal evidence is more a change in the consumption basket as countries are getting richer. It doesn’t mean that, relatively speaking, there is more consumption expenditure. We are observing economic development, changing demographics and hence changing taste (the young want more services, less goods), but you’re not observing consumption-driven growth. This “new” kind of demand is affecting businesses who are catering to these changing tastes. But, it is not driving the overall economy.

Can consumption abroad drive growth in ASEAN?

Here is the other common myth: Even as China rebalances away from investment and exports, the more vigorous Chinese consumer will drive ASEAN exports. This is wrong at many levels. First, as noted above, there is no booming Chinese consumer. In real terms, consumption as a percentage of GDP has barely risen. Second, consumption growth is holding steady and can hardly be considered a driver. Third, consumption is much less import intensive than both investment and exports. 4The truth is most of ASEAN exports are in intermediate goods whose final demand typically lies in investment, rather than consumption. To the extent that it is consumption, it has more to do with the consumer in the US, Eurozone and Japan, rather than in Asia.

A paper from the Ministry of Trade and Industry, Singapore, brings it out. To quote: “Of the VA (value added) derived from external final demand, only one-quarter was attributable to the direct exports of goods and services to final demand markets. The remaining three-quarters of the VA from external final demand were generated through global value chain effects”. 5 While this result is for Singapore, it is illustrative of the nature of demand for ASEAN exports.

Besides, as the report shows, that 25% of value added relates to all external demand. If we consider only consumption, the number is much smaller.

Moving to a consumption-led economy?

It sounds easier than it is. China has been trying for years — and they have had two natural advantages – and yet have barely moved the share of consumption in GDP. First, in the near 10% growth years, policy measures had been set up to boost investment, all they had to do was reverse some of these decisions to try and boost consumption. Second, China’s consumption to GDP ratio is extremely low and thus easier to nudge upward.

Start with China’s policy settings when investment and exports were driving growth. Primary among these has been a real interest rate kept below its market-clearing level and an undervalued exchange rate. Both of these measures have been changing.

Interest rates have now been liberalised, in particular the ceiling on deposit rates has been scrapped. Artificially low rates, with a large spread between deposit and lending rates, were effectively a transfer away from household income to banks and that hurt consumption.

The exchange rate has also actively been aiding rebalancing. Since 2005, the RMB has appreciated by about 40 % in real trade weighted terms. As a stronger currency helps consumption – rise in real incomes – while a weaker currency helps investment – cheaper for foreigners to invest – clearly policy settings have been moving in favour of rebalancing.

Source: CEIC, CIMB Research

Besides the exchange rate and interest rates, there were at least two other issues that have contributed to a high investment (low consumption) ratio.

The first is Chinese labour policy. From the start of reforms to until about the late 1990s, in real terms, wages grew at around 5.9% compared with GDP growth of 9.9%. With wages not keeping pace with GDP growth, household income growth did not keep pace with GDP growth and consumption as a percentage of GDP declined from about 50% of GDP to about 35% of GDP in the mid-2000s. That has now completely changed and labour’s share in income has been rising for several years.6

Source: ILO, CIMB Research

The second is the provision of social safety nets or lack of it. Initially there weren’t many safety nets, so as incomes increased, the Chinese did not go out and spend. Instead the savings rate rose from 35% in 1980 to about 50% by the mid-2000s.

But this policy too has been changing. The World Bank and Development Research Center report states that since 1990, China has been putting in social protection programs at a pace that is unprecedented internationally. The report notes that “these include pension programs for urban and rural residents; pension, unemployment, sickness, workplace injury, and maternity insurance for urban sector workers; and a national social assistance scheme that now covers more than 70 million people, among others”.7

The change in policy settings have also been helped as a consumption to GDP ratio of less than 40% is one of the lowest in the world, Yet, despite all this, and a decade of trying, the ratio of consumption to GDP has hardly moved.

In short, moving to a consumption-led growth model is not easy. Expecting the consumer to pick up the slack when trade, and consequently income growth, are struggling is unlikely. For ASEAN economies, at their current stage of development and their external orientation, the old trade-investment virtuous circle remains true.

Conclusion

Domestic consumption demand is not driving growth in ASEAN. Nor is it likely to any time soon. While consumption abroad does have a positive effect on ASEAN exports, it is not as much as investment abroad and the presence of value chains. From a structural perspective, trade remains ASEAN’s main driver of growth. And while ASEAN economies cannot really affect global demand they can decide how they respond to it and that involves continuous trade-boosting measures. There needs to be a move away from protectionism. Indeed, barriers to trade need to continue being lowered, while making sure that those who are dislocated by trade are adequately compensated, so as to make the reforms sustainable. Trade deals such as the Trans-Pacific Partnership (TPP), even without the US, are to be encouraged.

1 The Chinese economy grew at a 6.7% pace in 2016. The official target for 2017 is 6.5% and history suggests the actual rate of growth will come very close to that.

2 Technically speaking, the gross savings rate is simply 1 minus the consumption to GDP ratio and so if we know one of them, we automatically know the other. Still, the savings rate is worth looking at from a policy perspective.

3 Vietnam: The Next ASEAN Tiger

4 Joong Shik Kang and Wei Liao, “Chinese Imports: What’s Behind the Slowdown?”, IMF Working Paper, May 2016

5 Feature Article: Analysis of Singapore’s External Sources of Final Demand

6 International Labor Organization, Global Wage Report 2016 / 17, “Wage inequality in the workplace”.

7 China 2030: Building a Building a Modern, Harmonious, and Creative High-Income Society by The World Bank and the Development Research Center of the State Council, the People’s Republic of China, 2012.

Disclaimer: All rights reserved. No part of this report may be reprinted or reproduced or utilised in any form or by any electronic, mechanical or other means, now known or hereafter invented, including photocopying or recording, or in any information storage or retrieval system without proper acknowledgement of CIMB ASEAN Research Institute.

The views, responsibility for facts and opinions in this publication rests exclusively with the authors and their

interpretations do not necessarily reflect the views of CIMB ASEAN Research Institute.