Indonesia: May 2018 Bank Indonesia meeting

HIGHLIGHTS

May 2018 Bank Indonesia meeting

- Bank Indonesia (BI) raised its 7-day Reverse Repo Rate by 25bp to 4.50% and left the door open for further policy rate adjustments.

- The rate hike cycles in 2008 and 2013 suggest an average policy rate increase of 25bp for every 3-4% depreciation in the currency.

- We do not rule out the possibility of more increases should currency volatility heighten, but we maintain our year-end policy rate forecast of 4.50% for now.

First rate hike since Nov 2014

Bank Indonesia (BI) decided to raise its 7-day Reverse Repo Rate (7DRRR) by 25bp to 4.50%, in line with our and market expectations. Correspondingly, the Deposit Facility Rate and Lending Facility Rate were lifted by the same magnitude to 3.75% and 5.25%, respectively. This was the first rate hike since Nov 2014 and after the policy rate was reduced by 200bp between 2015 and 2017 to boost economic growth. The decision came as several external risks triggered capital outflows, which negatively impacted the rupiah movement. The rupiah has depreciated 3.4% YTD.

A slightly hawkish statement

By indicating it is “ready to implement stronger measures to maintain macroeconomic stability”, BI left open the possibility of further policy rate adjustments. We take note of the sensitivity of monetary policy responses to depreciating rupiah trends in the past. Back in 2008 and 2013, the policy rate was raised by 150bp and 175bp in the respective years amid sharp currency depreciation (by ~20%), translating into an average 25bp increase in the policy rate for every 3-4% depreciation in the currency.

International reserves remain ample despite recent contraction

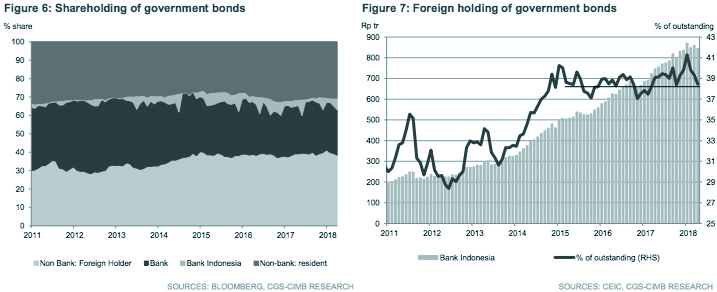

BI’s intervention in foreign exchange and bond markets has led to a US$7bn decline in the country’s international reserves in the past three months. At US$124.9bn, the reserves level remains comfortable as it is sufficient to cover 7.7 months of imports. Following the foreign portfolio outflows, the foreign shareholding of government bonds of 38.4% in Apr was in line with the average of ~38.7% in the past three years.

Macroeconomic conditions remain stable

The assessments of the domestic macroeconomic conditions were little changed. The central bank is willing to tolerate a wider current account deficit (BI projection: 2.0-2.5% of GDP; CIMB forecast: 2.0% of GDP; 2017: 1.7% of GDP) as long as the deficit stays within the 3% of GDP threshold, as stronger imports are a reflection of the recovery in economic growth (BI projection: 5.1-5.5%; CIMB forecast: 5.3%; 2017: 5.1%). The inflation rate remained in check despite the weaker currency in recent months. The volatile food pressure eased, although the seasonally higher demand could lead to higher inflationary pressure again. Based on BI’s consumer confidence survey, the short-term price expectation index rose in anticipation of the festive season while the long-term price expectation index remained steady.

We expect the policy rate to stay for now

Although we do not rule out the possibility of further rate adjustments if rupiah volatility heightens, for now we expect the current policy rate level to stay to allow the growth recovery to gain further momentum. We reiterate that a drastic cycle of rate increases and a sharp currency depreciation are not our base-case scenarios.

Originally published by CIMB Research and Economics on 18 May 2018.