Indonesia: March 2018 trade

HIGHLIGHTS

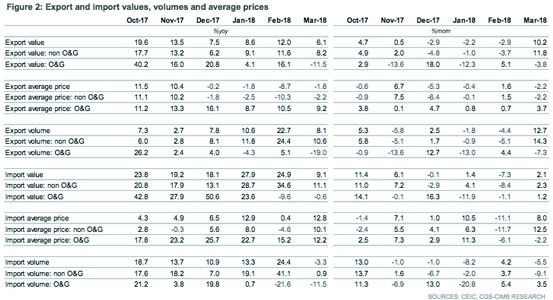

March 2018 trade

- Trade balance surprised on the upside in March, as import growth moderated at a faster pace compared to export expansion.

- O&G was a drag on exports, whereas slowdown in import growth was across the board after strong gains in January-February.

- A lower quarterly trade surplus suggests that the current account deficit may widen further to 2.5% of GDP in 1Q18F, in our view.

- We keep our 2018 trade forecasts unchanged (exports: +5.2% yoy; imports: +6.9% yoy; trade balance: +US$11.3bn).

Trade balance swings back into surplus in March

Indonesia’s trade balance unexpectedly swung back into surplus in March after three consecutive months of deficits (+US$1,092m in March vs. -US$53m in February; CIMB forecast: -US$351m; Bloomberg median consensus: -US$89m). The positive surprise was due to moderation in imports expansion (+9.1% yoy in March vs. +24.9% yoy in February; CIMB forecast: +16.7% yoy; Bloomberg median consensus: +13.5% yoy) that was steeper than that of export growth (+6.1% yoy in March vs. +12.0% yoy in February; CIMB forecast: +3.2% yoy; Bloomberg median consensus: +3.0% yoy). The pullback in non-O&G imports lifted non-O&G trade surplus to US$2,016m (+US$791m in February), while O&G deficit was marginally higher at US$925m (US$844m deficits in February).

Contraction in O&G shipments the key driver of slower exports

The contractions in O&G exports (-11.5% yoy in March vs. +16.1% yoy in February) was the key contributor to a slower export expansion, weighed down by base effects due to a brief surge in crude oil shipments in February 2017. Non-O&G commodity exports delivered mixed performances — palm oil and tin exports contracted, whereas exports of iron and steel, nickel, ores, slag and ash continued to expand. Ongoing expansion in global economic activity underpinned the 8.1% yoy gain in export volume in March, in line with the average growth in the past 1.5 years.

Broad-based slowdown across main import categories

The slowdown in imports was broad-based, with imports of consumer goods contracting in March after two months of exceptionally strong gains (-9.5% yoy in March vs. +55.0% yoy in February), whereas imports of raw materials recorded a milder gain of 9.0% yoy in March (+20.5% yoy in February). Imports of capital goods remained strong at 21.6% yoy (32.2% yoy in February), indicating that investment activity remained supportive of GDP growth.

Higher current account deficit projected for 1Q18F, at 2.5% of GDP

The surprise turnaround in March kept Indonesia’s 1Q18 trade balance in a surplus position (+US$283m vs. +US$997m in 4Q17). Nonetheless, as the quarterly trade surplus was at its smallest level since 4Q14, we expect the current account deficit (CAD) to widen to US$6.3bn, or 2.5% of GDP in 1Q18F (US$5.8bn, or -2.2% of GDP in 4Q17). Meanwhile, the trade surplus in volume terms grew 14.2% yoy in 1Q18 (+2.8% yoy in 4Q17), suggesting a potentially positive net trade contribution to GDP growth.

No change in our 2018 gross export forecast of 5.2% yoy

Given the relatively small trade exposure (42% of GDP in 2017) and low exposure to electrical and electronics (E&E)/machinery exports, Indonesia is relatively insulated from US-China trade tensions compared to other key ASEAN countries, we think. Hence, we maintain our gross export forecast of 5.2% yoy for 2018F.

Originally published by CIMB Research and Economics on 16 April 2018.