Indonesia: February 2018 trade

HIGHLIGHTS

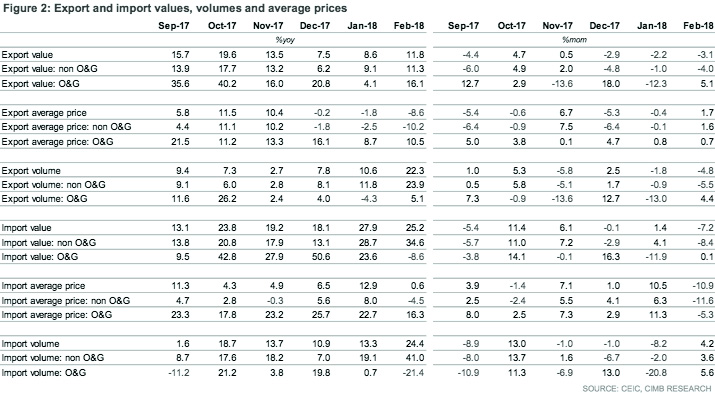

February 2018 trade

- The trade deficit narrowed to US$116m in Feb on the back of stronger export growth (+11.8% yoy in Feb vs. +8.6% yoy in Jan).

- Mining was the key driver of Feb’s export performance whereas the decline in palm oil exports may have been affected by India’s CPO import duty hike.

- Import growth remained strong across all segments as domestic activity gained traction.

- No change to our 2018 trade forecasts (exports: +5.2% yoy; imports: +6.9% yoy; trade balance: +US$11.3bn).

Trade deficit narrowed in Feb on stronger export growth

The trade deficit narrowed to US$116m in Feb (-US$756m in Jan, CIMB forecast: – US$437m; Bloomberg median consensus: -US$124m) as the recovery in export expansion to a three-month high (+11.8% yoy in Feb vs. +8.6% yoy in Jan; CIMB forecast: +12.1% yoy; Bloomberg median consensus: +12.4% yoy) was accompanied by a slight moderation in import growth momentum (+25.2% yoy in Feb vs. +27.9% yoy in Jan; CIMB forecast: +28.3% yoy; Bloomberg median consensus: +26.0% yoy). The non O&G trade surplus widened (+US$754m in Feb vs. +US$180m in Jan) while the improvement in the O&G trade deficit was marginal (-US$870m in Feb vs. -US$936m in Jan).

Mining sector was the key driver of stronger export growth

Resource-based segments, such as O&G (+16.1% yoy in Feb vs. +4.1% yoy in Jan), nickel (+41.2% yoy vs. -10.0% yoy in Jan), iron and steel (+121.4% yoy vs. +103.1% yoy in Jan), tin (+110.2% yoy vs. -72.3% yoy in Jan) as well as ores, slag and ash (>1,000% yoy vs. 20.5% yoy in Jan) propelled the stronger export performance. The lifting of the mineral ores ban in the previous year supported nickel shipments whereas the decline in palm oil exports may have been affected by an import duty hike on crude palm oil (CPO) by India, the largest consumer of Indonesia’s CPO, as well as festive holidays in China, which led to fewer working days.

Strong momentum across all import components

All import segments continued to grow at a strong pace. Investment activity, supported by ongoing infrastructure projects, continued to underpin strong imports of capital goods (+32.2% yoy in Feb vs. +30.2% yoy in Jan). As rolling stocks are expected to be delivered for railway projects (i.e. Jakarta MRT, Palembang LRT) over the next few months, we expect the growth momentum to be sustained. Imports of consumer goods accelerated further (+55.3% yoy in Feb vs. +34.0% yoy in Jan) as the government resorted to importing about 346,000 tonnes of rice between late-Jan and 28th Feb to curb soaring prices due to domestic supply shortages.

Manufacturing PMI in Feb rose to the highest level in 20 months

Imports of raw materials grew 20.7% yoy in Feb (+26.7% yoy in Jan), in line with Indonesia’s manufacturing Purchasing Managers’ Index (PMI) survey, which indicated that purchasing activity improved as production levels and new orders rose amid higher domestic demand. The manufacturing PMI improved to 51.4 in Feb from 49.9 in Jan.

Stable inflation in other CPI components

Slower core inflation was contributed by a milder increase in clothing price (3.9% yoy in Feb vs. 4.1% yoy in Jan), while healthcare and education, recreation and sports inflation were unchanged at 2.8% and 3.4%, respectively.

Maintain 2018 export growth forecast at 5.2% for 2018

The imposition of tariffs on imports of solar panels, washing machines, steel and aluminium by the US is expected to have a minimal impact on Indonesia, whose main exports to the US are apparel, rubber products and footwear. Indonesia, nonetheless, will not be spared as the impact of the trade war spills over to the rest of the world. We maintain our forecasts for export growth of 5.2% and trade surplus of US$11.3bn for 2018.

Originally published by CIMB Research and Economics on 16 March 2018.