Indonesia: February 2018 Bank Indonesia meeting

Originally published by CIMB Research and Economics on 19 February 2018.

HIGHLIGHTS

February 2018 Bank Indonesia meeting

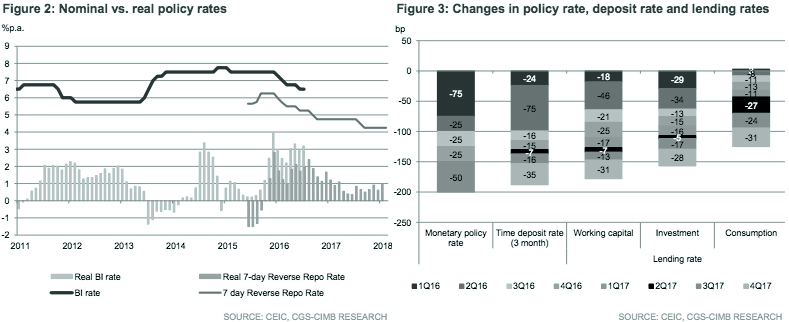

- Bank Indonesia left the 7-day Reverse Repo Rate unchanged at 4.25% and reiterated that the previous rate cuts were adequate to keep the growth recovery going.

- Recent volatility in the currency and financial markets has had the central bank shifting the policy focus towards ensuring macroeconomic stability.

- Citing volatile food prices as the key inflation risk, BI continues to foster closer policy coordination with the government to address supply-driven inflationary pressure.

- We maintain our year-end policy rate forecast of 4.25%.

Policy rate at status quo

As widely expected, Bank Indonesia (BI) maintained the 7-day Reverse Repo Rate (7DRRR) at 4.25%. The Deposit Facility Rate and Lending Facility Rate were also left unchanged at 3.50% and 5.00%, respectively. Reiterating that previous rate reductions were adequate to support the ongoing recovery in domestic economic growth, BI added that “maintained economic stability will be the backbone of stronger and more sustainable economic growth.”

Recovery momentum reflected in better 4Q17 GDP growth

The improvement in GDP growth for the past two quarters (5.2% yoy in 4Q17 vs. 5.1% yoy in 3Q17) lifted full-year growth to a four-year high of 5.1% yoy in 2017 and removed the need for further easing after an aggressive 200bp reduction in the past two years. Growth in the past year has been supported by rising investment activity, in tandem with continuous infrastructure development and FDI inflows, whereas exports were boosted by rising commodity prices and stronger global growth. BI envisages the aforementioned factors will continue to spur economic expansion at a rate of 5.1-5.5% in 2018 (vs. CIMB forecast of 5.3% yoy).

Cautious on rising external uncertainty

Against the backdrop of improving GDP growth, ensuring currency stability will be BI’s main focus. Recently, anticipation of more interest rate increases by the Fed (vs. official projection of three hikes) amid the faster-than-expected wage growth and inflation triggered volatility in global financial and currency markets. Portfolio outflows in the bond and equity markets led to a depreciation in the rupiah by 1.3% between 1 and 15 Feb, reversing all the gains in Jan and prompting the central bank to intervene by using foreign exchange reserves to stabilise the currency movement. As foreign holdings of government bonds (41.3% as of Jan 2018) remains high compared to its regional peers (29.3% for Malaysia and 15.7% for Thailand), currency volatility remains sensitive to reversals in portfolio flows.

Inflation risks stem from volatile food components

Inflation risks have arisen from volatile food components (CPI weight of 17.5%) given soaring rice prices in recent months on the back of supply shortages. Nonetheless, the inflation rate should remain manageable, in our view, cushioned partly by the base effect from the step-up in administered price inflation in 1H17. The base effect has kept headline inflation at the start of the year (3.3% yoy in Jan) under control and within the BI’s target range of 2.5-4.5%.

Reiterate our year-end policy rate forecast of 4.25%

With rising uncertainty in the global financial markets and BI’s outright statement indicating that the rate cut cycle is over, we reiterate our year-end policy rate forecast of 4.25%.