Indonesia: April 2018 CPI inflation

HIGHLIGHTS

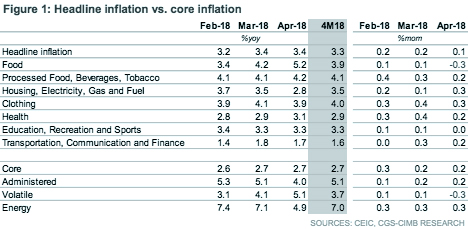

April 2018 CPI inflation

- Headline inflation was stable at 3.4% yoy in April, a tad above our expectation but lower than market consensus.

- The stable reading was aided by balancing forces between volatile food (lifted by low base effect) and administered price inflation (weighed down by high base effect).

- As food inflation is expected to tick higher, the government’s commitment to keep fuel prices unchanged will be key for inflation rate to stay within the official target.

- We keep our average inflation forecast at 3.4% for 2018F, and expect Bank Indonesia to maintain its policy rate at 4.25% at its next meeting on 16-17 May.

Stable headline inflation in April

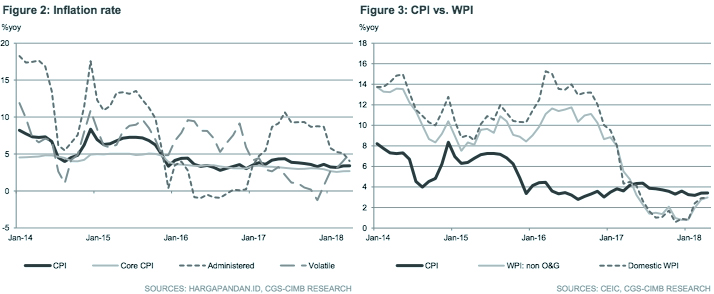

Headline inflation stood steady at 3.4% yoy in Apr (+3.4% yoy in Mar; CIMB forecast: 3.3%; Bloomberg median consensus: 3.5%), as the 0.1% mom increase in consumer price index in Apr 2018 matched that of Apr 2017. Furthermore, core inflation was unchanged at 2.7% yoy in Apr, as milder administered price inflation (+4.0% yoy in Apr vs. +5.1% yoy in Mar) removed the effect of higher volatile food inflation (+5.1% yoy in Apr vs. +4.1% yoy in Mar).

Food price pressures eased month-on-month

The acceleration in annual food inflation, despite a 0.3% mom decline, was the result of a low base effect, which is likely to drive the yoy change higher until year-end given an extremely benign price pressure during most of 2017. Nonetheless, the sequential mom decline implied easing price pressures, coming from rice, red chilies, pepper, and fresh & preserved fish. Rice prices have declined for two consecutive months as harvest season and rice imports relieve inflationary pressures triggered by supply shortage.

Step-up in base effect sent administered price inflation lower

Easing administered price inflation was led by waning electricity and water services inflation (+4.9% yoy in Apr vs. 8.4% yoy in Mar) due to a step-up in base effects arising from a second upward adjustment of postpaid 900VA electricity tariffs in Apr 2017. Transport inflation was unchanged at +2.5% yoy in Apr, as the government extended fuel price controls to non-subsidised fuels and required fuel retailers to seek approval on future fuel price adjustments. These measures were introduced to mitigate the risk of rising global oil prices on consumer inflation. We estimate that every 1% increase in global oil prices and/or 1% depreciation in Rp/US$ would raise market prices by an average of 0.92% for solar diesel, and 0.87% for premium gasoline.

Balancing clothing and health inflation kept core inflation in check

Among the core inflation components, declining inflation rate for clothing (+3.9% yoy in Apr vs. +4.1% yoy in Mar) cancelled out a sharper increase in health costs (+3.1% yoy vs. +2.9% yoy in Mar), while education, recreation and sports costs rose at a stable pace of 3.3% yoy.

Maintain average 2018 inflation forecast at 3.4% yoy

Balancing forces between volatile food and administered price inflation again kept overall inflation stable in Apr. Given that food price pressures are expected to rise as the festive season approaches, the government’s policy of not changing the fuel price will be crucial in keeping the inflation rate within the central bank’s target range of 2.5-4.5%. We maintain our forecast for average inflation to moderate to 3.4% yoy in 2018F (+3.8% yoy in 2017).

Originally published by CIMB Research and Economics on 2 May 2018.