Indonesia: April 2018 Bank Indonesia meeting

HIGHLIGHTS

April 2018 Bank Indonesia meeting

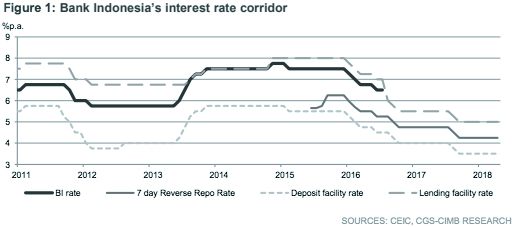

- Bank Indonesia (BI) maintained its 7-day Reverse Repo Rate at 4.25%, as widely expected.

- The central bank has turned more cautious about external uncertainties and the impact on the rupiah.

- BI reiterates its expectation of stronger GDP growth in 1Q18 vs. 1Q17 and downplayed inflation as domestic risk.

- No change in our year-end policy rate forecast of 4.25%, implying that BI will hold the rate through 2018.

7-day Reserve Repo Rate kept at 4.25%

Bank Indonesia’s (BI) decision to maintain its 7-day Reverse Repo Rate (7DRRR) at 4.25% was widely anticipated by the market, including us. Correspondingly, the Deposit Facility Rate and Lending Facility Rate were left at 3.50% and 5.00%, respectively.

Turning more cautious about external risks

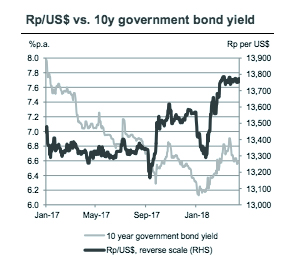

We think the central bank has turned more cautious about external risks, where it highlighted “external pressures begin to build.” Key risks arise from a potential escalation in US-China trade tensions, after both countries proposed to slap tariffs on the other’s imports earlier this month, as well as on expectations of further interest rate hikes by the US Federal Reserve, which could impact risk sentiment as well as exchange rate movements. The rupiah stabilised below Rp13,800 per US$ in the first half of April but at the expense of foreign exchange reserves, which fell further in March (-1.6% mom to US$126bn), amid continued intervention by BI to stabilise the currency.

Striking a more positive tone on private consumption

BI reiterated its expectation of stronger GDP growth in 1Q18 compared to 5.0% yoy in 1Q17. We concur with its expectation given improving domestic demand and resilient growth in the trade volume surplus (+14% yoy in 1Q18 vs. +12% yoy in 1Q17) despite a significantly narrower trade value surplus (US$0.3bn in 1Q18 vs. US$4.1bn in 1Q17). Encouragingly, the central bank’s tone on private consumption has turned more positive as it now expects private consumption to increase amid improving household purchasing power, compared to “stable private consumption is backed by maintained public purchasing power” in its previous statement.

No change in its CAD projection

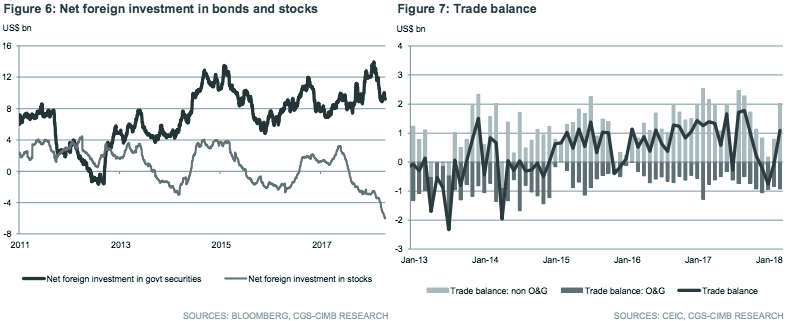

While ongoing infrastructure projects and non-building investments will continue to drive import growth, BI maintained its current account deficit (CAD) projection at 2.0-2.5% of GDP for 2018 as higher imports are expected to be accompanied by stronger exports. Commodities exports are the key driver, alongside stronger outbound manufacturing shipments spurred by sustained global economic growth momentum. We had expected 1Q18 CAD to widen to 2.5% of GDP and we reckon our full-year projection of 1.8% of GDP might be too low.

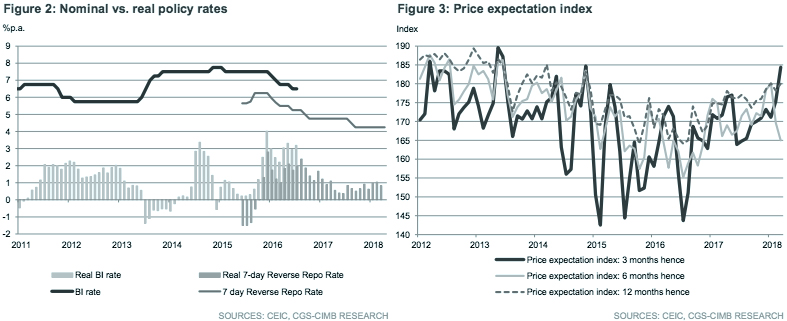

Inflation rate to remain under control

BI did not highlight inflation pressure as a domestic risk. Policy adjustments, like the coal price cap at US$70 per metric tonne and the imposition of an approval process to raise non-subsidised fuel prices, have reduced upward price pressures and hence inflation expectations remain stable.

No change in our year-end policy rate forecast of 4.25%

Despite its cautious tone amid external uncertainties, we expect BI to leave the policy rate unchanged to ensure continued recovery in economic growth momentum. Hence we reiterate our policy rate forecast of 4.25% until end-2018.

Originally published by CIMB Research and Economics on 20 April 2018.