Indonesia: 4Q17 GDP growth: An investment-led expansion

Originally published by CIMB Research and Economics on 6 February 2018.

HIGHLIGHTS

- 4Q17 real GDP growth surprised marginally on the upside (5.2% yoy vs. 5.1% yoy in 3Q17), despite weather disruptions.

- The outperformance was lifted by robust investment expansion, but private consumption growth remained sluggish.

- Net exports contributed negatively to GDP growth as domestic demand supported import growth, while export growth halved on slower non-O&G shipments.

- Maintain GDP growth forecast at 5.3% yoy for 2018F (5.1% yoy in 2017).

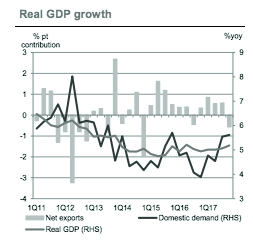

GDP growth accelerated to 5.2% yoy in 4Q17…

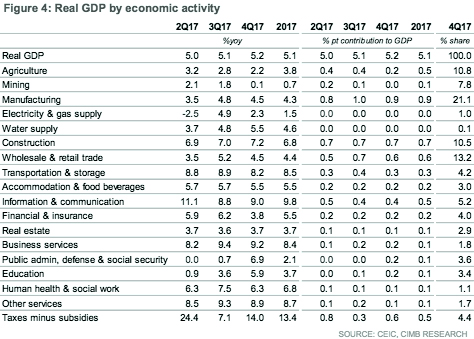

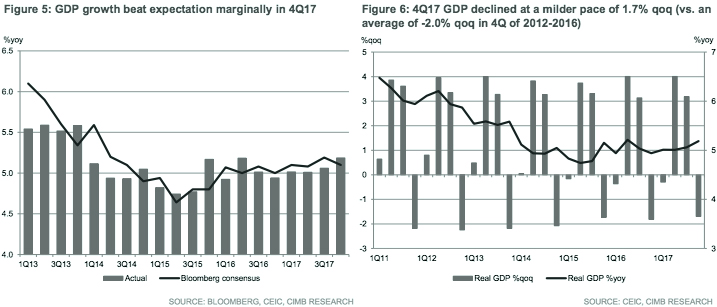

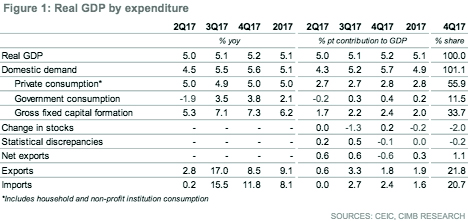

Indonesia’s GDP growth improved to 5.2% yoy in 4Q17 (5.1% yoy in 3Q17), marginally higher than our and Bloomberg median consensus forecasts of a 5.1% yoy gain. The yoy expansion has quietly gained momentum, approaching the pace last seen in 2Q16. On a quarterly basis, GDP fell at a milder pace of 1.7% qoq (+3.2% qoq in 3Q17), compared to an average 2.0% contraction in the corresponding quarters in 2012-2016. For the full year, the GDP rose 5.1% yoy (5.0% in 2016), in line with our and market expectation.

… lifted by robust investment growth

Despite weather disruptions (i.e. floods and volcano eruption) during the quarter, domestic demand growth was sustained (5.6% yoy in 4Q17 vs. 5.5% yoy in 3Q17), and contributed 5.7% pts to GDP growth (vs. 5.2% pts in 3Q17). An upside surprise came from further acceleration in investment growth in 4Q17 after an already strong performance in 3Q17 (7.3% yoy vs. 7.1% yoy in 3Q17), as a better business climate and massive infrastructure projects boosted outlays in machinery & equipment (22.3% yoy vs. 15.2% yoy in 3Q17) and buildings & structures (6.7% vs. 6.3% yoy in 3Q17).

No notable improvement in private consumption

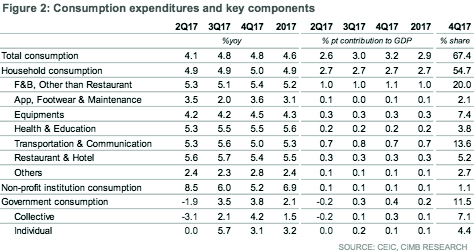

Low base effects, coupled with decent realisation of domestic government revenue collection, lifted public consumption growth higher in 4Q17 (3.8% yoy vs. 3.5% yoy in 3Q17). Nonetheless, private consumption growth remained sluggish (5.0% yoy in 4Q17 vs. 4.9% yoy in 3Q17). While the moderating inflation rate contributed towards the collective improvement in household spending on F&B, footwear and equipment, it has yet to translate into stronger discretionary spending. As such, the expansion in household consumption of transport & communications slowed amid lower auto sales, although disrupted transport services due to poor weather could also be a contributing factor, we think.

Domestic demand led to negative contribution of net exports

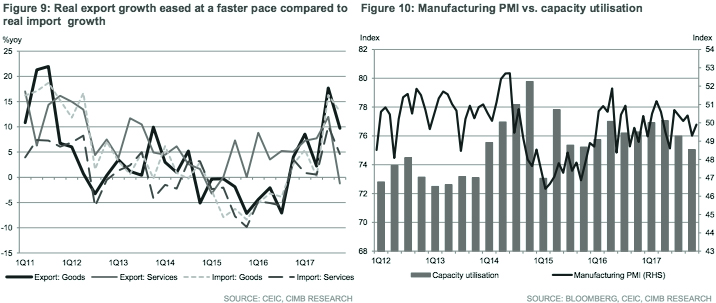

Resilience in domestic demand supported import performance in 4Q17 (11.8% yoy vs. 15.5% yoy in 3Q17). Nonetheless, as real export growth halved (8.5% yoy in 4Q17 vs. 17% yoy in 3Q17) on the back of slower non-O&G outward shipments, net exports contribution to real GDP growth declined for the first time since 3Q16 (-0.6% pts in 4Q17 vs. +0.6% pts in 3Q17).

Reiterate 2018 GDP growth forecast of 5.3% yoy

With a couple of key events scheduled for 2018, namely regional elections and the Asian games, we expect domestic demand to remain the key driver of GDP growth in 2018F. A gradual recovery in private consumption could be in sight amid a stable inflation rate, higher minimum wage growth, firmer commodity prices and falling lending rates, whereas investment growth will continue to ride on the improved investment climate and infrastructure spending, in our view. We reiterate our GDP forecast of 5.3% yoy for 2018.

Household consumption growth remained sluggish in 4Q17 (5.0% yoy vs. 4.9% yoy in 3Q17). As inflation rate moderated further, household spending on F&B, footwear and equipment recovered during the quarter. Nonetheless, discretionary spending remained soft, as reflected in slower household consumption on transport & communication (5% yoy in 4Q17 vs. 5.6% yoy in 3Q17) amid lower auto sales.

Stronger government consumption was due to the low base effect and decent realisation of tax revenue collection, which lent support to government expenditure.

Another outperforming quarter for gross fixed capital formation growth (7.3% yoy vs. 7.1% yoy in 3Q17) as investment in machine & equipment as well as buildings & structures quickened.

Growth acceleration driven by tertiary sectors

The stronger growth momentum in construction and services sectors offset the slowdown in manufacturing and resource-based sectors (i.e. agriculture, mining).

- Agriculture GDP grew 2.2% yoy in 4Q17 (2.8% yoy in 3Q17) as the decline in farm food crops (-4.7% yoy vs. -0.3% yoy in 3Q17) and slower output expansion in livestock (0.4% yoy vs. 4.2% yoy in 3Q17) dampened the stronger output of plantation crops (5% yoy vs. 2.7% yoy in 3Q17).

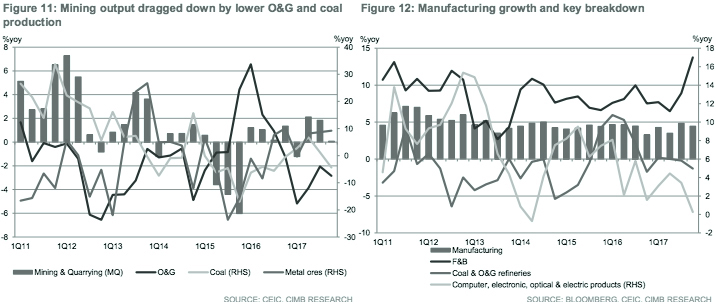

- Mining GDP only grew marginally (0.1% yoy in 4Q17 vs. 1.8% yoy in 3Q17) as collective declines in O&G and coal productions (affected by poor weather conditions), which accounted for two-third of mining GDP, offset the stronger growth in other mining products i.e. metal ores.

- The manufacturing sector expanded at a slower pace of 4.5% yoy in 4Q17 (4.8% yoy in 3Q17), as weaker upstream activities negatively affected O&G and coal refineries (-1.3% yoy vs. -0.2% yoy in 3Q17), alongside lower output for tobacco (-7.6% yoy vs. +1.1% yoy in 3Q17), leather products and footwear (-2.7% yoy vs. -1% yoy in 3Q17), paper products and printing (- 4.5% yoy vs. -0.3% yoy in 3Q17) as well as chemical products, pharmacy and traditional medicines (-5.5% yoy vs. +5.3% yoy in 3Q17). Nonetheless, consumer industries such as F&B (13.8% yoy in 4Q17 vs. 8.9% yoy in 3Q17) and textiles & apparels (6.4% yoy vs. 4.6% yoy) recorded stronger growth.

- Construction activity continued to gather steam in 4Q17 (+7.2% yoy vs. +7.0% yoy in 3Q17), in line with stronger investment in buildings and structures (6.7% yoy vs. 6.3% yoy in 3Q17).

- The services sector was supported by public administration, defence & social security (6.9% yoy in 4Q17 vs. 0.7% yoy in 3Q17) amid stronger government spending during the quarter, in addition to education (5.9% yoy vs. 3.6% yoy in 3Q17), and information & communication (9% yoy vs. 8.8% yoy in 3Q17).