Indonesia: 4Q17 direct investments

Originally published by CIMB Research and Economics on 1 February 2018.

HIGHLIGHTS

- Direct investments (DI) rose 12.3% yoy to US$13.4bn in 4Q17, led by DDI (+14.0%

yoy to US$5.0bn) and FDI (+11.4% yoy to US$8.4bn). - Close to 50% of DI went into tertiary sectors (i.e. transport & storage, construction,

utility), the key beneficiaries of government’s infrastructure and electrification plans. - Rising commodity prices continued to attract FDI into the mining industry, whereas DI

into the secondary sector declined for the fourth consecutive quarter. - We expect GDP to expand 5.1% yoy in 4Q17, and maintain our 2018 GDP growth

forecast at 5.3% yoy.

2017 a record year for direct investments at above US$50bn

Total direct investments rose 12.3% yoy to US$13.4bn in 4Q17 (+13.6% yoy to US$13.2bn in 3Q17) – 63% were from foreign direct investments (FDI) (+11.4% yoy to US$8.4bn in 4Q17) and 37% from domestic direct investments (DDI) (+14.0% yoy to US$5.0bn). For the full-year, direct investments gained 14.6% yoy to US$51.8bn, crossing the US$50bn line for the first time.

Direct investment dominated by tertiary sectors

DI in 4Q17 was driven primarily by tertiary sectors: transport, storage & communications (FDI +432% yoy / DDI +518% yoy), construction (FDI +139% yoy / DDI +119% yoy), real estate (+29.6% yoy / DDI +394% yoy) and utility (FDI +80% yoy). Most of these industries benefit from the government’s ambitious plans for infrastructure projects and power plant construction. On the back of improving commodity prices, FDI into the mining industry remained above US$1bn for the fifth consecutive quarter, whereas DDI into the mining sector fell to US$55m after three-quarters of exceptionally strong realisations ranging between US$326m and US$606m.

DI into manufactured sectors fell for the fourth consecutive quarter

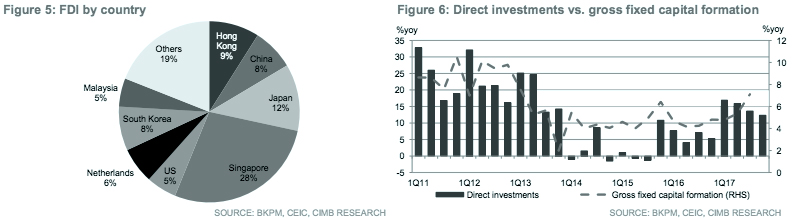

The contraction of DI into secondary sectors deepened to 22.9% yoy in 4Q17 (-11.8% yoy in 3Q17): motor vehicle & other transports (FDI -68% yoy / DDI -24% yoy), nonmetallic mineral (FDI –18% yoy / DDI -51% yoy), chemical & pharmaceutical (FDI -51% yoy / DDI -55% yoy) and wood (FDI –92% / DDI -50% yoy). Large Asian economies – Singapore (27.8% of FDI), Japan (11.9%) Hong Kong (9%) South Korea (7.9%) and China (7.5%) – contributed close to two-thirds of FDI in 4Q17.

Improved investment climate spurs new investments

DI has been rising by the double-digits in every quarter in 2017, and the full-year DI outperformed the government’s target by 2.1%, supported by an improving global growth outlook, commodity prices as well as better investment climate, i.e. greater ease of doing business, tax incentives, FDI liberalisation and upgrade in sovereign ratings. This was also reflected in the higher number of realised projects for the year (+49% yoy to 49,617 projects) as well as the improvement in DI in new projects to 80.2% of total DI (75.5% in 2016).

GDP growth to remain at 5.1% yoy in 4Q17

4Q17 GDP will be released on 5 Feb 2018, and we expect GDP to expand 5.1% yoy (5.1% yoy in 3Q17). With FDI liberalisation in sectors such as tourism, e-commerce and logistics, as well as ongoing massive infrastructure projects, we expect investment momentum to continue in 2018. We reiterate our GDP growth forecast of 5.3% yoy for 2018.