Indonesia: 4Q17 balance of payments

Originally published by CIMB Research and Economics on 19 February 2018.

HIGHLIGHTS

4Q17 balance of payments

- The current account deficit (CAD) widened to US$5.8bn or -2.2% of GDP in 4Q17 as lower primary income deficits were not sufficient to offset a smaller trade surplus.

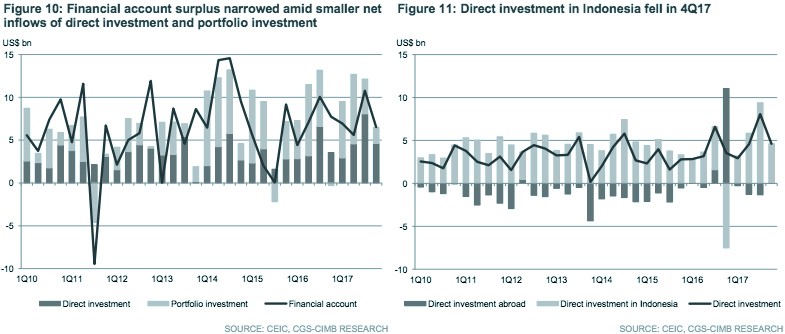

- The surplus in the financial account narrowed amid FDI outflows in the O&G sector and smaller portfolio inflows in government bonds.

- High foreign holding of government bonds (41.3% as of Jan 2018) may present a risk to BOP and currency when capital flows reverse.

- We maintain our CAD forecast at -1.8% of GDP for 2018. We expect higher inbound tourist receipts to mitigate the narrower trade surplus and rising interest payment.

CAD in 4Q17 at 3-year high…

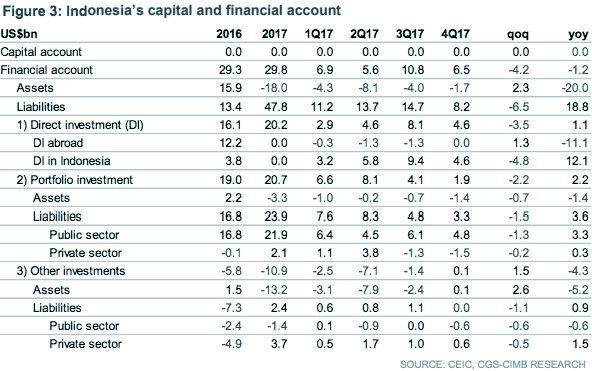

The current account deficit (CAD) widened to US$5.8bn or -2.2% of GDP in 4Q17 (US$4.6bn or -1.7% of GDP in 3Q17), matching our forecast. The financial account (FA) surplus narrowed to US$6.5bn or 2.5% of GDP (US$10.8bn or 4.1% of GDP in 3Q17) but was more than enough to offset the CAD. As a result, the balance of payment (BOP) remained in surplus (US$1bn or 0.4% of GDP vs. US$5.4bn or 2.0% of GDP in 3Q17) and the international reserves rose US$0.8bn qoq to US$130.2bn at end-2017.

… primarily led by lower trade surplus

The higher CAD was mostly driven by a lower surplus on the goods account (US$3.2bn in 4Q17 vs. US$5.3bn in 3Q17). Weaker expansion of manufactured exports contributed to a lower non-O&G surplus whereas rising oil prices drove O&G deficits to a 3-year high. The deficit in the services account rose slightly (US$2.3bn in 4Q17 vs. US$2.1bn in 3Q17) amid underperformance of travel receipts as tourism activities were disrupted by Mt. Agung’s eruption. Travel service exports accounted for 25% of the annual total in 4Q17 vs. 27-28% in 4Q of 2010-2016.

Deficit in primary income were lower but…

The deficit in the primary income improved US$1.1bn qoq to US$7.8bn or 3% of GDP amid a lower interest payment on debt (typically higher in 1Q and 3Q). Nonetheless, interest payment will rise further on the back of continued government bond issuance to finance fiscal deficits as well as high foreign shareholding in government debt. As the government welcomes more foreign direct investments (FDIs), net income payment on direct investment (which exceeded US$5bn in the 3Q17 and 4Q17) may also increase.

FA surplus narrowed on lower DI and portfolio inflows

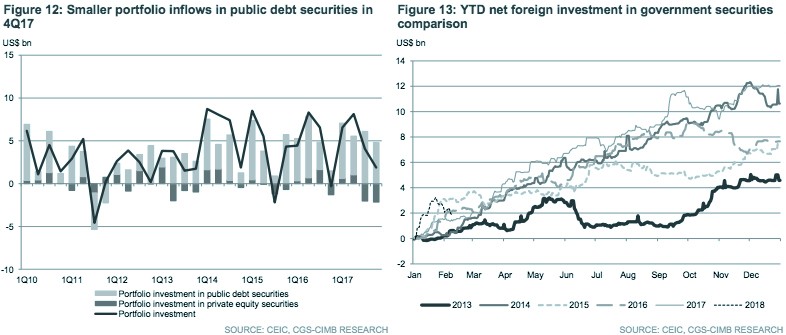

Net direct investment inflows were lower (US$4.6bn or 1.8% of GDP in 4Q17 vs. US$8.1bn or 3.1% of GDP in 3Q17) amid FDI outflows in the O&G sector. Lower foreign inflows into government bonds and continued outflows in the equity market led to smaller net inflows in portfolio investment (US$1.9bn or 0.7% of GDP in 4Q17 vs. US$4.1bn or 1.5% of GDP in 3Q17). High foreign shareholding of government bonds (41.3% as of Jan 2018) could be a risk to BOP and the rupiah exchange rate as it is sensitive to the direction of global monetary policy and market sentiment.

Maintain 2018 CA deficit forecast at -1.8% of GDP

We maintain our CAD forecast at US$19.7bn or -1.8% of GDP for 2018 (vs. deficit of US$17.3bn or -1.7% of GDP in 2017). We expect higher travel surpluses, led by higher tourist arrivals and travel spending during the Asian Games, to mitigate the impact of primary account deficits amid rising interest payment as well as a lower trade surplus, driven by stronger import expansion relative to exports.

The current account deficit rose to a 3-year high of US$5.8bn in 4Q17 as a lower deficit in the primary income was not sufficient to offset the smaller trade surplus.

The goods account recorded a lower surplus on the back of slower manufactured exports whereas rising oil prices led to higher O&G trade deficits (Indonesia is a net O&G importer).

The deficit in the services account rose US$0.2bn in 4Q17. Travel service exports, typically the highest in 4Q (about 27-28% oftotal in 2010-2016), were disrupted by Mt. Agung’s eruption.

The lower deficit in the primary income account (US$7.8bn in 4Q17 vs. US$8.9bn in 3Q17) coincided with lower debt interest payments (typically higher in 1Q and 3Q).

The financial account recorded a lower surplus in 4Q17 (US$6.5bn vs. US$10.8bn in 3Q17) due to lower net inflows in direct investment and portfolio investment.

Net direct investment inflows declined on the back of lower FDI inflows in the manufactured sector and FDI outflows in the O&G sector.

Net inflows in portfolio investment more than halved to US$1.9bn (vs. US$4.1bn in 3Q17) amid lower foreign investment inflows to government bonds during the quarter.