Indonesia: 2Q18 direct investments

HIGHLIGHTS

2Q18 direct investments

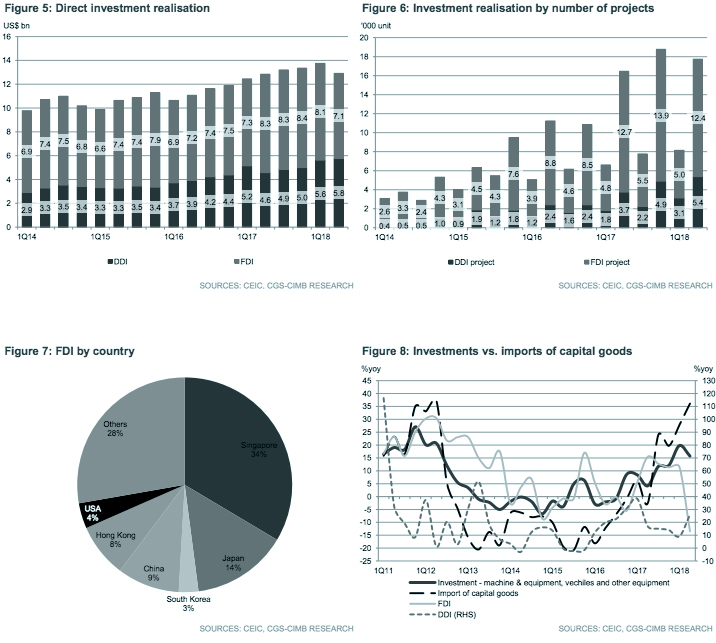

- Direct investments (DI) grew 0.6% yoy to US$12.9bn in 2Q18 as gains in DDI (+25.9% yoy to US$5.8bn) offset the decline in FDI (-13.5% yoy to US$7.1bn).

- The key growth drivers were mining (ex O&G), transport, storage & communications, real estate and utilities.

- Falling capital investments from Japan, China, South Korea, Hong Kong and the US contributed to the decline in FDI.

- No change to our 2018F GDP growth forecast of 5.3%.

Mildest annual increase since 3Q15

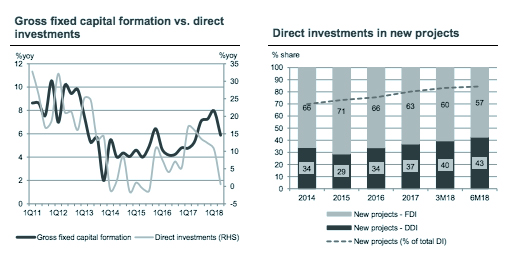

Total direct investments (DI) grew 0.6% yoy to US$12.9bn in 2Q18 but was 6.1% qoq lower compared to US$13.8bn in 1Q18. The slower growth in DI coincided with the moderation in gross fixed capital formation (+5.9% yoy vs. +7.9% yoy in 1Q18). Domestic direct investments (DDI) increased 25.9% yoy to US$5.8bn (+9.1% yoy to US$5.6bn in 1Q18). Foreign direct investments (FDI), however, fell 13.5% yoy to US$7.1bn in 2Q18 (+11.5% yoy to US$8.1bn in 1Q18), for the first time since 4Q16.

Record capital outlays in mining industry

Of the three sectors, DI in the primary sector recorded the strongest growth in 2Q18 (+22% yoy to US$2.9bn in vs. -4% yoy to US$2.4bn in 1Q18) as improving commodity prices attracted investment in mining (FDI -1% yoy/DDI +90% yoy). The quarterly capital outlays in mining (ex O&G) industry exceeded the US$2bn mark for the first time ever.

DDI supports investments in tertiary sector

Within the tertiary sector (+20% yoy to US$5.7bn in 2Q18 vs. +44% yoy to US$6.7bn in 1Q18), DI in transport, storage & communications (FDI +148% yoy/DDI +272% yoy) took the lead, supported by the government’s infrastructure projects, which also spurred imports of capital goods during the quarter. Other drivers included real estate (FDI +145% yoy/DDI +2% yoy) and electricity, gas & water supply (FDI -9% yoy/DDI +44% yoy).

Decline in FDI and DDI drags investment in secondary sector

The pace of contraction of DI in secondary sectors deepened in 2Q18 (-24% yoy to US$4.3bn vs. -12% yoy to US$4.7bn in 1Q18), dragged by weaker investments in metal, machinery & electronic (FDI -31% yoy/DDI unchanged yoy), chemical & pharmaceutical (FDI -33% yoy/DDI +36% yoy) as well as food (FDI -49% yoy/DDI +24% yoy).

FDI from East Asia and the US declined

34% of FDI came from Singapore, followed by Japan (14%), China (9.4%), Hong Kong (8%) and Malaysia (5%). Nonetheless, in terms of growth, capital investments from Japan, China, South Korea, Hong Kong and the US declined during the quarter amid the escalating US-China trade war and weakening rupiah.

No change to our 2018F GDP growth forecast of 5.3%

Investments in new projects continued to increase (84.4% of DI in 2Q18 vs. 83.2% in 1Q18) on the back of improving ease of doing business. Looking ahead, we expect investment growth to be supported by ongoing infrastructure projects. The Committee for Acceleration of Priority Infrastructure Delivery (KPPIP) has estimated that 13 projects worth Rp46.8tr and 25 projects worth Rp118.8tr will be completed in 2018 and 2019, respectively. We maintain our GDP growth target of 5.3% for 2018F.

Originally published by CIMB Research and Economics on 15 August 2018.