Indonesia: 2Q18 balance of payments

HIGHLIGHTS

2Q18 balance of payments

- The 2Q18 current account deficit (CAD) hit a four-year high of -US$8.0bn or -3.0% of GDP, led by the trade account slipping into deficit and higher dividend repatriations.

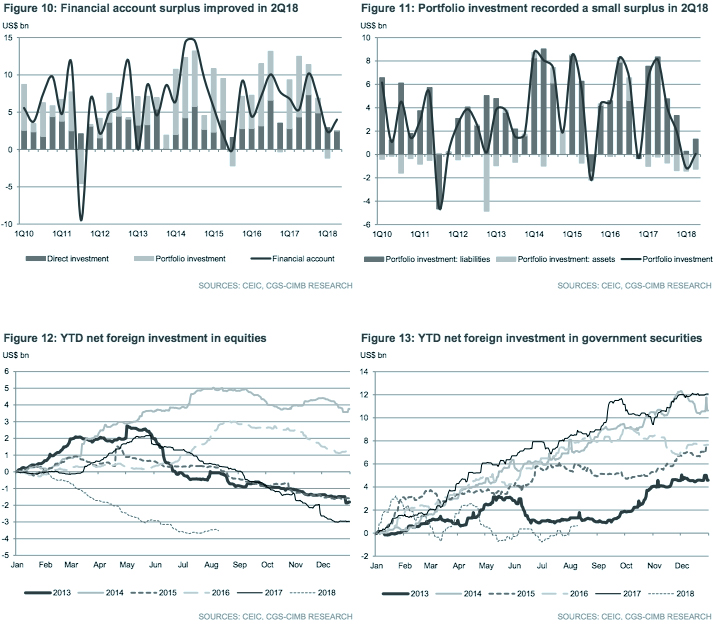

- The BOP remained in deficit as the financial account surplus was only sufficient to finance 50% of the CAD.

- Net portfolio investments recorded a small surplus (vs. a deficit in 1Q18), supported by the issuance of foreign currency-denominated bonds in April-May 2018.

- We maintain our CAD forecast at -US$26.6bn or -2.5% of GDP for 2018.

2Q18 current account deficit worsened to -US$8.0bn (-3.0% of GDP)

Indonesia’s current account deficit (CAD) widened more than expected to a four-year high of -US$8.0bn or -3.0% of GDP in 2Q18 (CIMB: -US$6.7bn; Bloomberg consensus: – US$7.8bn; 1Q18: -US$5.7bn or -2.2% of GDP). The increase in CAD outpaced the improvement in financial account (FA) surplus (+US$4.0bn or +1.5% of GDP in 2Q18 vs. +US$2.4bn or +0.9% of GDP in 1Q18). As a result, the balance of payments (BOP) deficit widened to -US$4.3bn or -1.6% of GDP (-US$3.9bn or -1.5% of GDP in 1Q18), leading to a decline in international reserves of US$6.2bn qoq to US$119.8bn at end 2Q18.

CA: higher imports and seasonal dividend payments

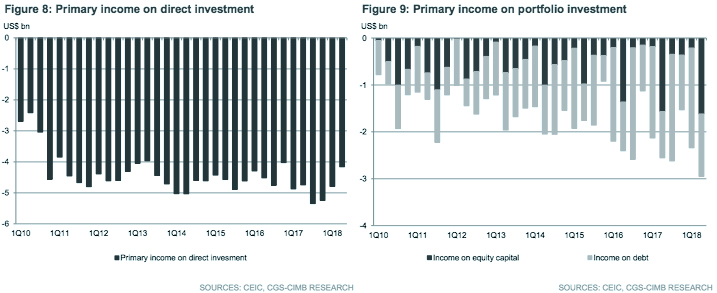

The higher CAD coincided with a smaller surplus in the goods account to +US$0.3bn in 2Q18 (+US$2.3bn in 1Q18) as stronger GDP growth of 5.3% yoy in 2Q18 spurred higher imports of raw materials, capital goods and O&G. This has also resulted in the quarterly trade balance turning into a deficit for the first time since 4Q14. Meanwhile, a higher primary income deficit (-US$8.2bn in 2Q18 vs. -US$7.9bn in 1Q18) was led by seasonally higher dividend payments, which typically takes place in 2Q. The long holiday associated with Lebaran celebrations fuelled higher overseas travel by Indonesians, resulting in a wider services account deficit (-US$1.8bn vs. -US$1.6bn in 1Q18) while higher secondary income was contributed by inward remittances of overseas Indonesian migrant workers.

FA: a marginal net inflow in portfolio investment

Given that higher investment abroad offset the increase in foreign direct investment in Indonesia, direct investment recorded a smaller inflow of US$2.5bn in 2Q18 (vs. +US$2.9bn in 1Q18). As a result, the basic balance (sum of the current account balance and net direct investment) fell deeper into negative territory as net direct investment inflows were only sufficient to finance 31% of the CAD in 2Q18 (vs. 51% in 1Q18). On a positive note, portfolio investments recorded a net inflow of US$0.1bn in 2Q18 (vs. -US$1.2bn in 1Q18) following the issuance of foreign currency-denominated bonds in April-May 2018 although foreign selling of rupiah-denominated government bonds continued during the quarter.

Higher cash transfers to boost low-income household consumption

Currently, the flat rate cash transfer of Rp1.89m p.a. is equivalent to 83% of the minimum monthly wage in Indonesia, relatively low compared to 120% in Malaysia. Higher allocations to the conditional cash transfer programme (Rp31tr in 2019F vs. Rp17tr in 2018F) through the adoption of a variable rate of cash transfers depending on the burden of low-income family should help boost low-income household consumption.

No change to our 2018F CAD forecast of -US$26.6bn (-2.5% of GDP)

The 1H18 CAD of -US$13.7bn (-2.6% of GDP) accounted for 52% of our annual CAD forecast of -US$26.6bn (-2.5% of GDP) for 2018, which was in line compared to an average of 51% in 2012-2017. Hence, we make no changes to our CAD forecasts. Our forecasts take into account higher travel receipts into the country during the Asian Games 2018, as well as a potentially milder yoy increase in primary income deficit, as we expect weaker foreign portfolio inflows into bond market so far this year to translate into smaller increase in interest payment outflows to foreign holders of Indonesian government bonds.

Originally published by CIMB Research and Economics on 13 August 2018.