Indonesia: 1Q18 direct investments

HIGHLIGHTS

1Q18 direct investments

- Direct investments (DI) rose 10.5% yoy to US$13.8bn in 1Q18, led by FDI (+11.5% yoy to US$8.1bn) and followed by DDI (+9.1% yoy to US$5.6bn).

- The key growth driver was the tertiary sector (utilities, construction and real estate).

- DI in the secondary sector contracted at a milder pace on the back of improving FDI, while DI in the mining sector took a back seat after strong realisations in 2017.

- Aided by a recovering investment climate, we project GDP to expand 5.2% yoy in 1Q18, and reiterate our 2018 GDP growth forecast at 5.3% yoy.

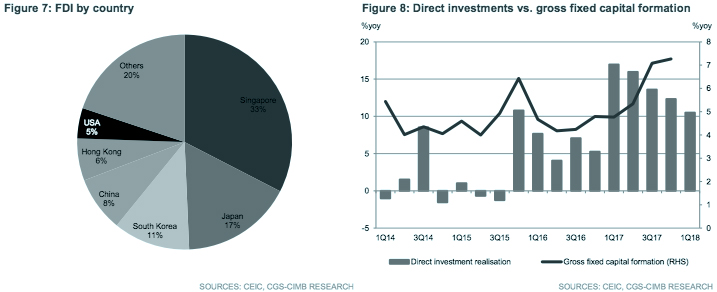

1Q18 direct investment realisation supported by FDI…

Total direct investments (DI) rose 10.5% yoy to US$13.8bn in 1Q18 (+12.3% yoy to US$13.4bn in 4Q17). Foreign direct investments (FDI), which accounted for 59% of DI, grew 11.5% yoy to US$8.1bn in 1Q18 (+11.4% yoy to US$8.4bn in 4Q17), whereas domestic direct investments (DDI) gained 9.1% yoy to US$5.6bn (+14.0% yoy to US$5.0bn).

… and led by investments in tertiary sectors

DI in tertiary sectors remained strong (+44% yoy to US$6.7bn in 1Q18 vs. +69% to US$6.4bn in 4Q17), and accounted for 48% of total DI, on the back of government’s infrastructure projects and power capacity expansion plans. The key drivers included real estate (FDI +141% yoy / DDI -28% yoy), utilities (FDI +22% / DDI +5%), and construction (FDI +592% / DDI +1,124%). DI in the mining industry (ex O&G) was weighed down by a strong expansion last year (-40% yoy to US$1.1bn in 1Q18 vs. -8% yoy to US$1.2bn in 4Q17). DI in the mining industry in 2017 was the highest since 2013, fostered by the lifting of mineral export ban in Jan 2017 and improving commodity prices.

Contraction of DI in secondary sectors eased amid improved FDI

The pace of contraction of DI in secondary sectors eased in 1Q18 (-12% yoy to US$4.7bn vs. -23% yoy to US$4.6bn in 4Q17), led by stronger FDI in machinery & electronics (FDI +73% yoy / DDI -20% yoy), wood (FDI +22% / DDI +48%), and chemical & pharmaceutical (FDI +9% yoy / DDI -15% yoy). DDI rose strongly in the motor vehicle & other transport equipment (FDI -56% / DDI +87%), and non-metallic mineral sectors (FDI -49% yoy / DDI +117% yoy). Singapore remained the largest source of FDI in 1Q18 (33% of FDI), followed by Japan (17%), South Korea (12%) China (8%) and Hong Kong (6%), which together contributed three-quarters of FDI.

More regulations to improve investment climate

The government’s push for a better investment climate has seen DI growing at a doubledigit pace in each of the past five quarters, with the share of new projects rising to 80- 83% in 2017-1Q18 from 63-70% in 2013-2014. The drive to spur more investment continued with recently issued regulations to simplify the tax holiday requirement and application process for investments worth at least Rp500bn (MOF Regulation No.35 of Year 2018), as well as a simpler application process for skilled foreign workers (Presidential Regulation No.20 of Year 2018).

Inflation rate to remain under control

BI did not highlight inflation pressure as a domestic risk. Policy adjustments, like the coal price cap at US$70 per metric tonne and the imposition of an approval process to raise non-subsidised fuel prices, have reduced upward price pressures and hence inflation expectations remain stable.

GDP growth of 5.2% yoy projected for 1Q18

Taking into account the latest DI readings, we expect 1Q18 GDP to grow 5.2% yoy, and reiterate our GDP growth forecast of 5.3% for 2018. The GDP reading for 1Q18 will be released on 7 May 2018.

Originally published by CIMB Research and Economics on 2 May 2018.