Economic Focus: Trade tensions escalate with tit-for-tat tariffs

HIGHLIGHTS

Trade tensions escalate with tit-for-tat tariffs

- The US proposal of 25% tariffs on 1,333 types of imports from China worth US$50bn has been met by retaliatory duties from China on 106 products from the US.

- We count more winners than losers in MIST, as exporters are well placed to benefit from displacement of demand for categories in which it competes with China/US.

- Some sectors face supply chain disruptions for intermediate/capital goods that it exports directly or via other countries to China and eventually destined for the US.

- Indonesia is relatively insulated from US-China trade tensions due to low exposure to E&E and machinery exports.

- We expect the near-term impact on MIST to be limited and for a compromise to be reached. However, trade tensions may spiral if tit-for-tat US-China tariffs intensify.

US levies 25% tariffs on US$50bn of China imports

The US Trade Representative’s office (USTR) has proposed a 25% tariff on 1,333 types of imports from China worth US$50bn – equivalent to 2.1% of total US imports – in retaliation for what it alleges to be the “forced transfer of US technology and intellectual property” by China. The proposal was not a major surprise, as President Trump had ordered remedial action to counter China’s trade practices on 22 Mar and subsequently issued threats on twitter to levy tariffs on up to US$60bn worth of imports from China. Markets are bracing for further sanctions as the US Treasury is due to revert in the coming weeks on 1) measures to address investments by China in ‘sensitive’ industries or technologies, and 2) whether to label China a currency manipulator.

China retaliates with new tariffs on 106 US products worth US$50bn

Several hours after the USTR’s tariff announcement, China unveiled its own retaliatory tariffs of 25% targeting 106 types of US imports totaling US$50bn (2.7% of China’s total imports), including soybeans, automobiles, chemicals and aircraft. Officials indicated that the timing of China’s duties will coincide with the implementation of US tariff measures.

Rational end game is a compromise…

The tariffs are unlikely to go into effect until late May at the earliest, as the USTR allows a 30-day period for public comments, and a hearing on the proposal has been scheduled for 15 May. We suspect that, like in previous sanctions against washing machines, solar panels, steel and aluminium, the provisions in this proposal will likely be watered down. Rather, this may be a bargaining chip to negotiate for reduced tariffs and non-tariff trade barriers in China to US exports and improved market access for US companies.

…as no one wins in a trade war

IMF estimates that a 10% rise in import tariffs applied by the US and the rest of the world would depress global trade by 1% and world GDP by 0.5%, i.e. tit-for-tat protectionism is a negative-sum game. Financial markets have reacted adversely to the prospects of escalating trade tensions that may trigger contagion effects, tighten global financial conditions and erode tailwinds from last year’s trade-led, synchronised recovery.

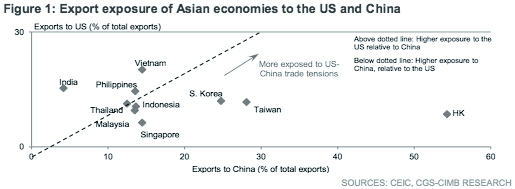

Potential winners and losers in ASEAN

If the tariff measures are implemented to the letter, we think exporters, particularly in Malaysia, Singapore and Thailand, are well placed to benefit from the displacement of demand for product categories in which it competes with China/US (E&E, machinery, chemicals, aircraft parts, rubber tyres and medical equipment). However, some sectors will also face disruptions in the supply chain for intermediate/capital goods that it exports directly or via other countries to China and eventually destined for the US (TVs, PCs, HDDs). Among MIST, Indonesia is relatively insulated from US-China trade tensions due to its low exposure to E&E and machinery exports. Meanwhile, Indonesia and Malaysia are well-placed to take advantage of China’s proposed tariff on soybean imports from the US (US$13.8bn in 2016) as the two largest exporters of palm oil, which is a substitute for edible oil.

US-China trade tensions

US levies 25% tariffs on US$50bn of China import

The US Trade Representative’s office (USTR) has proposed a 25% tariff on 1,333 types of imports from China worth US$50bn “in response to China’s policies that coerce American companies into transferring their technology and intellectual property to domestic Chinese enterprises” [link to tariff list]. The proposal, which resulted from an investigation under Section 301 of the 1974 US Trade Act [link to report and fact sheet], is part of a set of recommended remedial actions to address China’s ‘unfair trade practices’:

- Tariffs. The USTR will propose additional tariffs on certain products from China with an annual trade value commensurate with the harm caused to the US economy resulting from China’s unfair trade practices. After a period of notice and comment, the Trade Representative will publish a final list of products and tariff increases.

- WTO dispute. At the direction of the President, pursue a dispute settlement in the World Trade Organization (WTO) to address China’s discriminatory technology licensing practices.

- Investment restrictions. Address concerns about investment in the US directed or facilitated by China in ‘sensitive’ industries or technologies deemed important to the US.

Section 301 is a key enforcement tool that allows the US to address a wide variety of unfair acts, policies, and practices of US trading partners. The investigation of China’s Acts, Policies, and Practices Related to Technology Transfer, Intellectual Property, and Innovation addresses four categories of acts, policies, and practices of the Government of China that unfairly result in the transfer of technologies and intellectual property from US companies to China. These policies harm US businesses and workers and threaten the long-term competitiveness of the US.

China retaliates with new tariffs on 106 US products

The US proposal was met with resistance by China, with its embassy in the US stating that: “The Chinese side strongly condemns and firmly opposes the unfounded Section 301 investigation and the proposed list of products and tariff increases based on the investigation. As the Chinese saying goes, it is only polite to reciprocate. The Chinese side will resort to the WTO dispute settlement mechanism and take corresponding measures of equal scale and strength against U.S. products in accordance with Chinese law.”

Several hours after the USTR’s tariff announcement, China unveiled its own counter tariffs of 25% targeting 106 types of US imports totaling US$50bn, including soybeans, automobiles, chemicals and aircraft. Officials indicated that the timing of China’s duties will coincide with the US implementing its set of tariffs. The latest salvo follows an earlier implementation of duties by China’s government on imports from the US totaling US$3bn effective 2 Apr 2018, covering 1) pork products and aluminium scrap (tariffs of 25%) and 2) fresh fruit, dried fruit and nut products; wine; modified ethanol; ginseng; and seamless steel pipe (tariffs of 15%).

End game is a compromise as no one wins in a trade war

An IMF working paper estimates that a 10% increase in import tariffs in both the US and the rest of the world would result in a 1% decline in global trade and a 0.5% fall in world GDP i.e. tit-for-tat protectionism is a negative-sum game. The sensitivities estimated by the IMF assume that other countries do not raise tariffs vis-à-vis each other. Hence, if US vs. rest of world tensions spill over to other trade relationships, the drag on global trade activity and GDP growth would be larger.

The Trump administration is clearly cognisant of the negative implications on the US economy from import tariffs, having chosen product categories that exerted pressure on China exports, but limited the damage to US consumers. This resulted in a US tariff list that skewed towards capital and intermediate goods but excludes retail mainstays such as shoes, clothing, mobile phones and furniture. Nonetheless, higher costs of industrial inputs may still result in producers passing on costs to consumers or create disruptions in the US supply chain, given China’s dominant position in segments like consumer electronics and semiconductors. Likewise, China has played hardball by directing its trade riposte to important US export segments and key Trump support bases (soybeans, raw cotton, beef, motor vehicle and aircraft exports) but in turn these tariffs may increase consumer and producer price inflation, especially as soybean, which is a key ingredient for cooking oil and animal feed.

There is still time to avert the escalating trade confrontation between the US and China. The proposed US tariffs are unlikely to go into effect for several weeks, as the USTR allows a 30-day period for public comments and a hearing on the proposed tariffs has been scheduled for 15 May. After the completion of this process, USTR will issue a final determination on the products that will be subject to additional tariffs.

Likewise, China officials have indicated that its implementation of retaliatory tariffs will depend on when the US enacts its trade tariffs after a period of public consultation. We suspect that, like in previous US sanctions against washing machines, solar panels, steel and aluminium, the provisions in this proposal will likely be watered down. Rather, this may be a ‘Trumpian’ negotiation tactic to reduce tariff and non-tariff trade barriers to US exports and improve market access for US companies. We expect near-term impact to MIST to be limited and a compromise to be reached. However the willingness of the US and China to engage in tit-for-tat tariffs raises the risks of escalating trade tensions. Markets are bracing for further sanctions as the US Treasury is due to revert in the coming weeks on 1) measures to address investments by China in ‘sensitive’ industries or technologies, and 2) whether to label China a currency manipulator.

Potential winners and losers in MIST

If the tariff measures are implemented to the letter, due to complex trade linkages, it is unclear at this juncture whether, on an aggregate basis, Malaysia, Indonesia, Singapore and Thailand may:

- Benefit from the displacement of demand for product categories in which it competes with China/US (electric and electronics products, machinery, chemicals, aircraft parts, rubber tyres and medical equipment), or

- Face disruptions in the supply chain for intermediate products that it exports directly or via other countries to China and eventually destined for the US (TVs, PCs, hard-disk drives and storage).

Nonetheless, we think there are sectors that stand to gain more than others under certain conditions. We classify potential winners as sectors that meet the following conditions:

- China exports to the US market are sizeable (large market share for grab), and

- MIST’s exports to the US market by components are high (strong position to win market share), and

- MIST’s indirect exports to the US via China are low (low exposure to China supply chain/independent trade ecosystem).

We classify potential losers as sectors that meet the following conditions:

- China exports to the US market are sizeable (vulnerable to market share erosion), and

- MIST’s exports to the US market by components are low (weak position to win market share or not an exporter of the finished good to the US), and

- MIST’s indirect exports to the US via China are high (high exposure to China supply chain/dependent trade ecosystem).

Based on a study of each country exposures to key export categories affected by the US tariffs, we count more winners than losers in MIST, as exporters are diversified, competitive and well placed to capitalise on the potential re-routing of trade resulting from the US and China tariffs. Among the MIST countries, we think Indonesia is the most insulated from US-China trade tensions due to its low exposure to E&E and machinery exports.

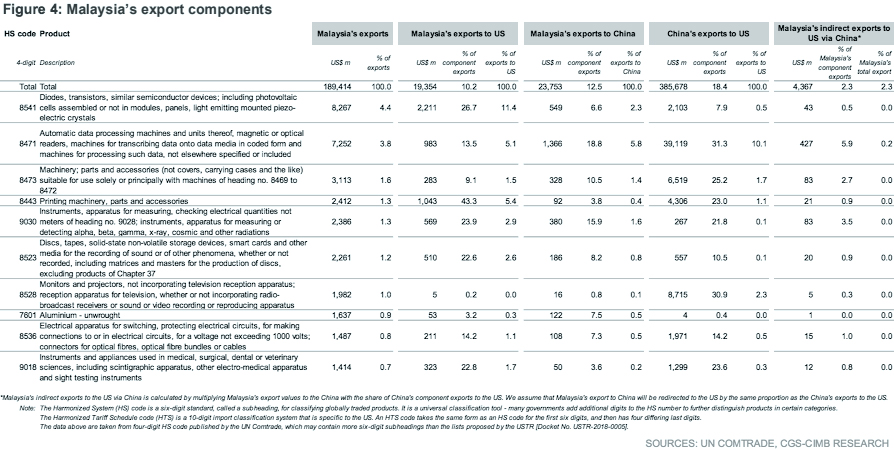

MALAYSIA

Potential winners are:

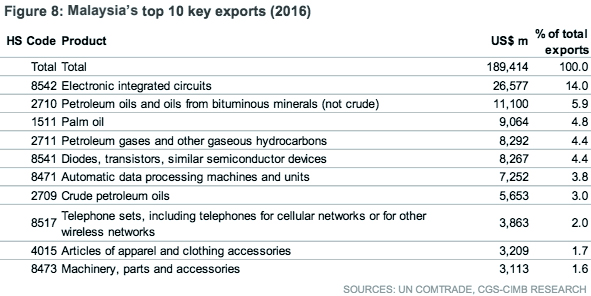

Malaysia exporters that compete directly with China for the US export market including semiconductors (HS code 8541), printers (8443), measurement instruments (9030), HDDs and storage (8523), medical equipment (9018), and electrical apparatus (8536), which cumulatively total US$4.9bn and account for 25.2% of Malaysia’s total exports to the US. Malaysia’s well-developed auto industry may also benefit from China’s tariffs on US motor vehicles and parts.

Edible oil substitutes. Malaysia is well-placed to take advantage of China’s proposed tariff on US soybean imports as the second largest producer of palm oil, which is a substitute edible oil.

Potential losers are:

Malaysia exporters of intermediate and capital goods to China destined for the US market including automatic data processors (8471) and machinery parts (8473), which cumulatively total US$1.3bn and account for 6.5% of Malaysia’s total exports to the US.

INDONESIA

Potential winners are:

Indonesian exporters that compete directly with China for US export market including pneumatic tyres (HS code 4011), printers (8443), monitors and projectors (8528), seats (9401), and wires and cables (8544), which cumulatively total US$1.8bn and account for 11.2% of Indonesia’s total exports to the US.

Edible oil substitutes. Indonesia is well-placed to take advantage of China’s proposed tariff on US soybean imports as the largest producer of palm oil, which is a substitute edible oil.

Potential losers are:

Indonesian exporters that export intermediate and capital goods to China destined for the US market are relatively limited due to its low exposure to E&E and machinery exports.

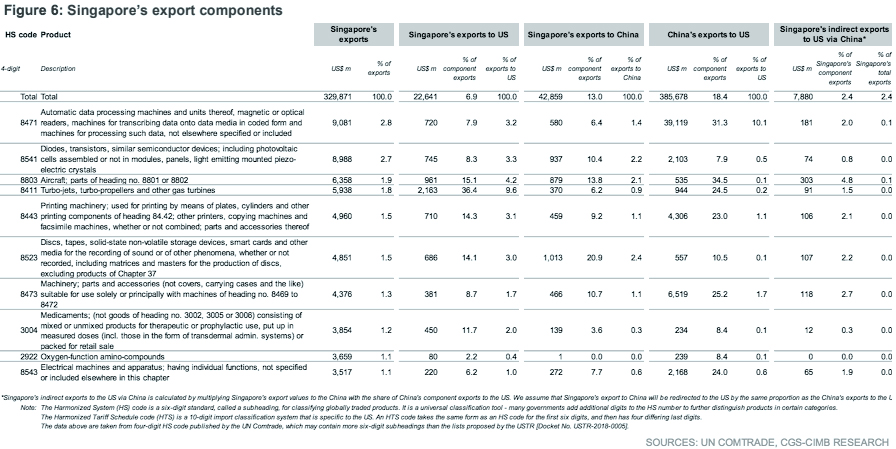

SINGAPORE

Potential winners are:

Singapore exporters that compete directly with China for US export market including automatic data processors (HS code 8471), aircraft parts (8803), turbojets, propellers and other gas turbines (8411), printing machinery (8443), and medicaments (3004), which cumulatively total US$5.7bn and account for 25% of Singapore’s total exports to the US.

Potential losers are:

Singapore exporters of intermediate and capital goods to China destined for the US market including semiconductors (8541), HDDs and storage (8523), and machinery parts (8473), which cumulatively total US$1.8bn and account for 8.0% of Singapore’s total exports to the US.

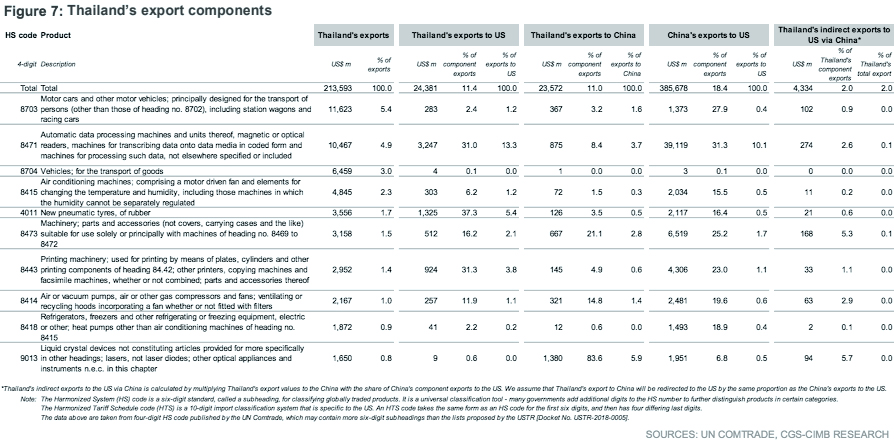

THAILAND

Potential winners are:

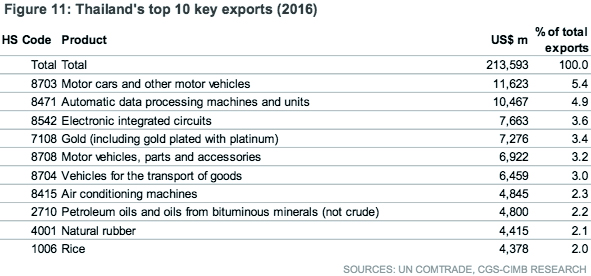

Thailand’s exporters that compete directly with China for US export market including automatic data processors (HS code 8471), air conditioning machines (8415), pneumatic rubber tyres (4011), and printing machinery (8443), which cumulatively total US$5.8bn and account for 23.8% of Thailand’s total exports to the US.

Potential losers are:

Thailand’s exporters of intermediate and capital goods to China destined for the US market including liquid crystal devices (9013), machinery parts (8473), motor vehicles (8703) and air or vacuum pumps/fans/compressors (8414) which cumulatively total US$1.1bn and account for 4.3% of Thailand’s total exports to the US.

APPENDIX – Top 10 export items in MIST

Originally published by CIMB Research and Economics on 05 April 2018.