Malaysia: August 2018 trade

HIGHLIGHTS

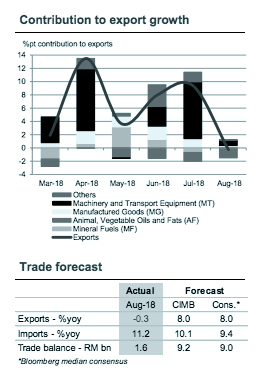

August 2018 trade

- Trade surplus sank to a 46-month low of RM1.6bn due to weaker non-oil commodity exports and E&E shipments

- Our 2018 export forecast is lowered to 6.5% to reflect challenging trade conditions and import growth lifted to 6.2% boosted by private consumption.

- We maintain Malaysia’s GDP growth forecast at 4.7% in 2018, as the scope for upside surprises is hampered by fading external tailwinds.

Underperforming export growth weighs on trade surplus

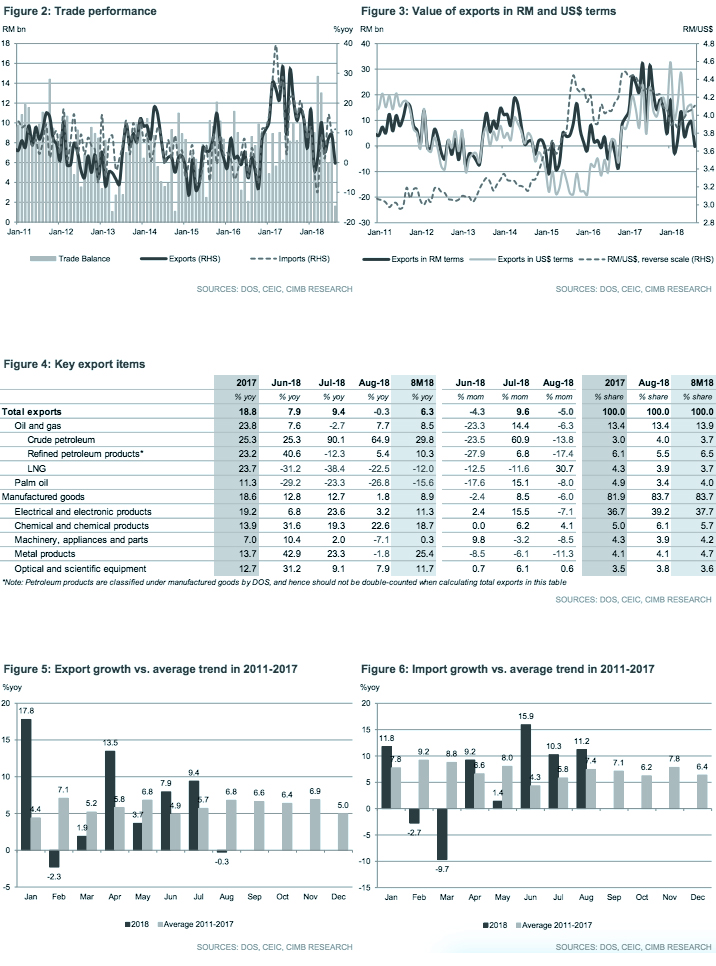

The trade surplus shrank to RM1.6bn in August (RM8.3bn in July) as global trade tensions took a toll on Malaysia’s export performance with a surprise 0.3% yoy decline in August (+9.4% yoy in July). The expansion of imports remained steady (+11.2% yoy vs. +10.3% yoy in July) on the back of resilient domestic demand in the final month of tax holiday. Total trade growth eased to 5.1% yoy (+9.8% yoy in July).

Supply shocks still a drag to commodity exports

The shipments of LNG (-22.5% yoy in August vs. -38.4% yoy in July) and palm oil (-26.8% yoy vs. -23.3% yoy in July) remained the weak spots in commodity segments. The global oil price uptrend was a boon to exports of crude oil (+64.9% yoy in August vs. +90.1% yoy in July) and refined petroleum products (+5.4% yoy vs. -12.3% yoy in July).

Manufactured exports floored by E&E and machinery

Manufactured export growth decelerated to a six-month low of 1.8% yoy (+12.7% yoy in July), particularly in E&E (+3.2% yoy vs. +23.6% yoy in July), machinery, appliances and parts (-7.1% yoy vs. +2.0% yoy in July) and manufacture of metals (-1.8% yoy vs. +23.3% yoy in July).

Exports to China and the US decelerate sharply ahead of Sep tariffs

Shipments slowed to China (+4.5% yoy vs. +37.5% yoy in July) and the US (-2.0% yoy vs. +6.7% yoy in July) after strong upticks in July, suggesting that manufacturers may have built inventories pre-emptively ahead of China’s Golden Week and additional tariffs levied by Beijing and Washington in August and September. There were pockets of weakness in export demand from the EU (-8.9% yoy), Japan (-22.9% yoy) and Singapore (-2.2% yoy).

Shopping spree ahead of the imposition of SST on 1 September

Domestic demand remained strong before the reintroduction of Sales and Service Tax (SST) on 1 September, as reflected in all three import categories: consumption goods (+14.2% yoy in August vs. +11.1% yoy in July), capital goods (+25.3% yoy in August vs. +4.6% yoy in July) and intermediate goods (+4.3% yoy vs. -0.1% yoy in July).

Wind knocked from export sails

Barring a strong reversal in September, net export contribution to headline GDP growth likely moderated further in 3Q18 from +0.1% pt in 2Q18. We tweak our 2018 forecast for gross exports from 7.7% to 6.5% and for gross imports from 5.5% to 6.2%. Hampered by external tailwinds, Malaysia is leaning more heavily on domestic demand, particularly private consumption, to drive growth, suggesting that GDP growth is unlikely to accelerate significantly in 2H18. We maintain our 2018 GDP growth forecast at 4.7%.

Originally published by CIMB Research and Economics on 5 October 2018.