Are central banks in ASEAN in a sweet spot?

The inflation conundrum

In recent months, we have been observing a rise in growth with low inflation numbers. The puzzle is that inflation remains tepid amid rising growth with labor markets near full employment. While low inflation bodes well for consumers it poses a conundrum for policy makers especially at a time when asset valuations remain high. So, should inflation levels drive the central bank’s policy or, rather, should the policy of central banks strive to affect the inflation rate?

The cyclical recovery in global growth has continued to gain ground in 2Q17. The US expanded at 3%, a faster pace than in Q1. In the Euro area recovery has broadened across constituent economies, and even in Japan growth surprised on the upside at 4%, beating expectations of 2.5%. In China, growth was stable at 6.9%, despite risks of rising debt looming over the economy. Elsewhere in ASEAN, the GDP print has been solid, faring better than what was expected for Malaysia, Thailand, Singapore and Vietnam.

As growth revives with unemployment rates falling, consumer spending ticking up and business investment expanding, wages start rising and prices start creeping up. Under normal circumstances, according to the Phillips curve, low unemployment is associated with rising inflation rates. However, this does not seem to be the case in the current global economy. Following the brief period of rising commodity prices at the turn of the year, headline inflation has softened and remains below central bank targets in most advanced countries. The 10 year breakeven rates continue to trend lower, signaling a retreat in investor inflation expectations.

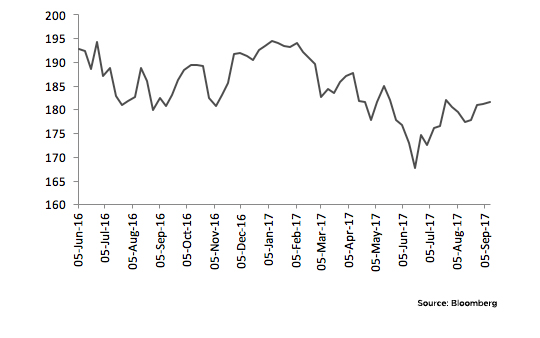

CRB Commodity Index

In ASEAN, the inflation story is in sync with global trends. Following a bout of overshooting, headline figures are largely receding. What does this mean for the direction of monetary policy? To answer this, we need to check on the underlying factors inflation is attributed to, i.e, exchange rate pass through (weaker currency resulting in imported inflation), excess demand beyond economy’s productive capacity (demand-pull) and supply side constraints (cost-push).

Is cost-push factor ruling inflation?

What constitutes supply-side pressures? The usual suspects are administered prices, costs of production inputs, prices of commodities, food and fuel etc. We need to ascertain how strong are these factors for MIST1.

From latest data for Malaysia we observe an easing of headline inflation. Transport cost which is perceived as the main driver of inflation, has been moderating after hitting a high in March 20172, as the low base effect of fuel prices dissipates. Headline readings for July were at 3.2% (y-o-y) and fall within the ambit of central bank target of 3 to 4% for 2017. For Indonesia, inflationary pressures are not broad-based and are largely attributed to administered price hikes (housing, electricity, gas and fuel). The central bank remains watchful of inflationary risks, which have inched lower and are likely to remain contained within the 3 to 5% target.

Headline inflation (%, y-o-y)

For Singapore, higher headline inflation numbers are largely boosted by supply-side factors (a combination of of energy related components and administrative price increases), rather than demand-side drivers. In Thailand, oil prices were the main driver pushing inflation higher at the start of the year. And with oil prices having softened again in recent months, it will now take an even longer time for the BOT to reach its inflation target of 1 to 4%.

How strong is “imported- consumption”?

In open economies fluctuations in exchange rate affect inflation. Thus a depreciation in the exchange rate would make imports costly for a consumer, assuming that other factors remain constant. For simplicity, we focus on the direct effect of pass through on consumer goods prices, and to gauge this we look at the import intensity of consumption, direction of exchange rate movement and import price index (IPI). The basic idea is if a commodity has a very low concentration in consumption basket, then the pass through effect of currency depreciation will be mild.

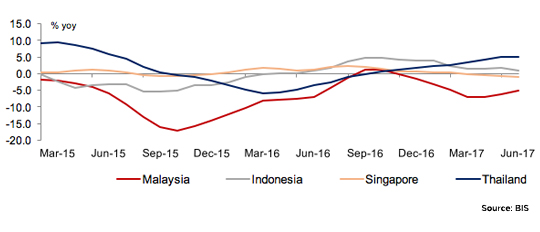

Evidence clearly points to a sustained strengthening of exchange rates on a trade weighted basis for Thailand and a downward bias for Indonesia and Singapore. Malaysia though remains weak has shown upward bias in recent times.

Nominal effective exchange rate

Lately, import price indices are showing a downtick. On the third criterion, import intensity of consumption is observed to be low for Malaysia, Indonesia and Thailand, in tune with general global trends. Putting the above pieces together, for Thailand, a relatively strong currency has kept in check foreign cost pressures and thus imported prices in domestic currency terms low. Therefore the exchange rate pass-through is contained. In the case of Indonesia and Malaysia, the pass-through to consumer prices may be somewhat mitigated by the fact that consumption has a low import content.

Import price index Import intensity of consumption

In case of Singapore, consumer price inflation primarily stems from the prices of imported goods, as Singapore is highly dependent on imports for its consumption needs. However, a negative output gap3 shows slackness in growth which has undermined imported inflation, as is evident from the declining trend in IPI, thereby limiting the pass through effect of exchange rate.

Output Gap in Singapore

Is economic activity firm enough to drive inflation?

Incoming data clearly point to a fiscal expansion and exports as the primary drivers of growth in MIST.

We have seen a resurgence in growth in Malaysia with GDP rebounding to a three year high of 5.8% in 2Q17 (averaging 5.7% in 1H17) which has ushered in an air of optimism to the recovery story. Exports, mainly manufacturing and commodities are the drivers behind this growth, while private consumption remains supportive as well. Sentiment indicators (business and consumer) have also ticked up. Private investment has also shown some exuberance but yet to gain traction.

However, contribution from the external sector in 2H17 is expected to cool as global trade moderates. And if exports moderate, it will have repercussions on several other parts of the economy. Nevertheless, private consumption will continue to remain steady amid a stable labor market and moderate wage gains. Meanwhile, populist spending by the government, ahead of the elections in 2018, is also expected to boost household spending. In our earlier piece4 we quantified the claim that consumption is not driving growth in Malaysia and we reaffirm it. Rather it has been resilient in the face of external shocks and has helped cushion overall growth.

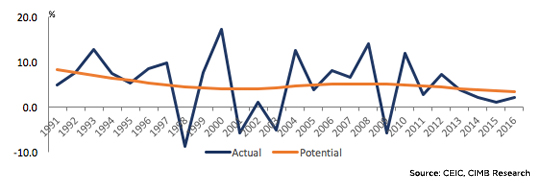

Growth Rates of Actual and Potential Output in Malaysia

In Indonesia, as per the latest release, growth has been flat at 5% in 1H2017, driven by public investment and an improved external position. Signs of a pick-up in investment in 2Q are encouraging, however, not strong enough to accelerate growth. On the other hand, private consumption (accounting for over 57% of the country’s economic growth) remains sluggish and consumption-GDP ratio has been falling. While household expenditure has shown some improvement since 2016, any significant rise is yet to be observed (multiple interest rate cuts totaling 175 bps failed to stimulate private spending and offtake in credit), given wages remain low. Recovery in export growth this year has not helped to boost consumption growth. As such, the link between stronger export growth and higher wage growth has been weak so far in 2017.

Domestic activity in Singapore has been growing below trend for a while now. The rebound in 2Q GDP print was largely the result of external demand for electronics which supports the manufacturing sector. However, structural challenges are weighing down the domestic sectors. Labor market conditions remain slack dampening consumption.

Growth Rates of Actual and Potential Output in Singapore

In Thailand, though the GDP prints for 2Q17 beat expectations (3.7% vs 3.2%), growth is yet to be broad-based. In 1H17, economic activity grew by 3.5%, exports with tourism and government stimulus providing the impetus. Private consumption has been lackluster, though recent improvements in farm income5 are helping stimulate it. Deleveraging also continues to weigh on consumption growth, especially in absence of stronger wage growth. Additionally, with capacity utilization at 67%, private investments remain stagnant, despite a mild improvement in 2Q mainly due to the base effect. On the other hand, export growth has surpassed expectations, but is unlikely to be sustained as China’s imports begin to slow.

Thus factors at play do not support a broad-based growth picture, though Malaysia seems relatively better placed than its peers. The next question is how are the current growth numbers and demand affecting inflation? Stated otherwise, is there a possibility of a demand-pull inflation? After all, monetary policy is a demand management tool.

The output gap analysis and inflation

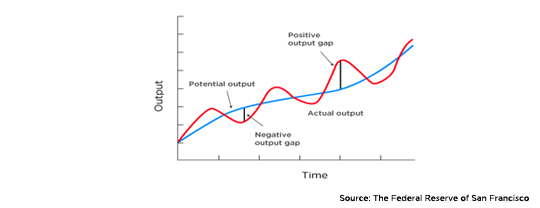

A measure often used for demand driven inflation is the output gap6. In other words, the output gap reflects the economy’s position in the business cycle, and also captures the possible presence of inflationary pressures arising from the level of utilisation of factors of production7. For example, an economy is operating with surplus capacity when actual output is below its potential level (negative output gap). This in turn is associated with easing of cost and price pressures.

Illustration of the relationship between actual and potential output and output gap

In the case of Malaysia, in level terms, actual output was close to potential output in 2016 (as per latest data available on output gap). Having said that, demand-pull pressures remain modest, in the absence of any significant increase in wages. This is also reflected in core inflation which has been hovering around 2.3 to 2.6%.

Output Gap in Malaysia Core inflation

For Indonesia and Thailand, core inflation has been inching down which clearly rules out the existence of demand driven pressure on prices. In the case of Thailand, inflation remains at multi year lows of sub 1%, while for Indonesia, we have pointed out earlier a muted growth in consumption.

Growth recovery in Singapore is still at an early stage and has yet to translate into greater private consumption and demand given the uncertainties. Consumer-focused industries such as retail remain subdued because of a weak labor market, the property market is still in a slump and there are worries about China’s growth outlook.

Should central banks change path?

From the above discussion, the influence of demand-pull pressures and exchange rate pass through on prices do not appear significant. This leads us to believe the role of supply-side factors adding to volatility in the headline figures.

In Malaysia, currently, demand-pull pressures that would call for a policy response are very modest. Of note, core inflation has remained below policy rate. For now, inflationary pressures are mainly cost-push. However, if growth remains strong, then inflationary pressures may become demand pull via higher wage growth. Bank Negara has held the interest rate at 3% since July 2016, which has translated to negative real interest rates, thereby calling for a tightening bias. However a rate hike at this stage is highly unlikely as the economic recovery is in its nascent stages and remains vulnerable to external headwinds, while inflation is gradually easing.

Bank Indonesia (BI) has recently surprised the markets, delivering a 25 bps cut, lowering the 7 day reverse repo from 4.75% to 4.5% in August 2017. The rate cut may be regarded as a signal that one should be more concerned about the current pace of GDP growth, and raises questions about the central bank’s traditional focus on financial stability and external environment. As such, BI appears to have left the door open for further rate cuts. But we do not foresee further easing. With the Fed announcement on balance sheet normalisation plans likely to be made this month, the external backdrop seems less supportive of rate cuts going forward.

In Singapore, with patchy growth and inflationary pressure remaining benign and well within the comfort zone of the central bank set targets, the Monetary Authority of Singpapore is expected to continue maintaining the current zero-appreciation of the SGD nominal effective exchange rate policy stance.

The Bank of Thailand (BOT) has kept its policy rate (one day repurchase rate) unchanged at a record low of 1.5% for more than two years now8. Though a negative output gap, low credit expansion9 and soft inflation numbers (the central bank has revised down core and headline inflation figures) do open up a debate for further easing, however, such a move at the current juncture might exacerbate financial stability risks, given a prolonged period of low interest rates. There are also doubts that any further cuts will lift demand, given the household debt overhang.

Output Gap in Thailand

Conclusion

We observe that inflation is largely cost-push in MIST. The underlying idea is to determine if the shock is temporary or permanent. The generally accepted theory is if the supply shocks are perceived as transient and expectations remain well anchored, then monetary policy need not respond to the shock. But if change in relative prices caused by the shock result in higher general inflation (via wage growth), central bank needs to step in.

As for MIST, inflation remains contained, as the temporary upswings wane in line with easing fuel and food prices. Having said that, central banks should ensure that the current cyclical pickup in economic activity stabilizes before paring back the accommodative stance. For now, this means that, in terms of monetary policy, interest rates will continue at the low levels for the foreseeable future.

Inflation in MIST

1 MIST is the acronym for Malaysia, Indonesia, Singapore and Thailand, and the piece primarily covers these countries.

2 Inflation in March 2017 was observed at an 8 year high at 5.1%, breaching the upper range of Central Bank projection of 3-4% for 2017, pushed up by higher fuel costs.

3 We have explained the concept of output gap later in the piece

4 Making trade great again: The misplaced reliance on the Asian consumer, March 2017 by Dr. Arup Raha

5 Resulting from increased agricultural yields following prolonged drought, as well as turnaround in global commodity prices.

6 Stated in simple terms, output gap is the difference between what an economy actually produces (actual output) and the maximum level of goods and services it can produce when operating at full capacity (potential output).

7 Increased demand for output beyond full capacity pushes up cost of factors of production.

8 The BOT had last changed rates in April 2015, when it cut the policy rate by 25 basis points to the present level.

9 There has been a reduced policy transmission, as domestic lenders have not lowered interest rates as much as the reduction in the policy rate owing to concerns about higher credit risks and non-performing loans.