AEC Blueprint 2025 Analysis: Paper 5 | Liberalisation of the Financial Sector

by Ken Li Yee | Originally published on 20 April 2016.

Summary

Liberalisation efforts surrounding the regions banking, insurance, and other financial instrument markets will need to keep up with burgeoning growth in the region; the AEC Blueprint 2025 hopes to continue capitalising upon the success of previous policies.

Foreword

The AEC Blueprint Analysis series is a publication which seeks to provide insight into the ASEAN Economic Community Blueprint (AEC) 2025. The publication will seek to do so by adopting a holistic approach in its analysis; creating context by examining past achievements, defining present challenges, and discussing future plans. The series will pay special attention to strategic measures outlined within the AEC’s new blueprint, providing insights with regards to the viability of regional economic integration under the AEC.

A. Past Plans

What were the targets in the AEC 2015 Blueprint?

ASEAN financial integration envisages a well integrated and smoothly functioning regional financial system with more liberalised capital account regimes and interlinked capital markets that will facilitate greater trade and investment flows in the region. This will be achieved through:

- Financial services liberalisation

- Capital account liberalisation

- Harmonisation of payments and settlements systems

ASEAN aims to only achieve semi-integration in the financial sector by 2020. Full integration comparable to the level achieved by the core member countries of the European Union (EU) is deemed to be too ambitious in the next decade. (“Regional Cooperation in Finance”, 2016)

1. Roadmap for Monetary and Financial Integration of ASEAN (RIA-Fin)

Endorsed in 2003, the RIA-Fin articulated ASEAN’s goals and efforts within a roadmap format. The roadmap also affirmed the usage of a positive list modality, which meant that any commitments made would apply only to an explicit list of sectors. The task of integrating ASEAN’s financial sector was divided into four separate areas:

- Financial Services Liberalisation:

Intended to achieve free flow of financial services by 2015 through progressive removal of restrictions on financial services providers with the presence of Qualified ASEAN Banks (QABs) in other ASEAN countries. - Capital Market Development:

Intended to build capacity and lay the long-term infrastructure for development of ASEAN capital markets, with a long-term goal of achieving cross-border collaboration between the various capital markets in ASEAN. This is through enhancing market access, linkages and liquidity through such proposed initiatives as ASEAN Exchanges linkages, Bond Markets linkages; and promoting credit ratings comparability between domestic and international credit rating agencies. - Capital Account Liberalisation:

Intended to achieve freer flow of capital by 2015. This refers to the easing of capital restrictions and implementation of safeguards against volatility and systematic risks. In essence red tape surrounding Foreign Direct Investments (FDI), investment into equities, and bank borrowing will be addressed. - Currency Cooperation:

To explore currency arrangements between member states aimed at facilitating intra-regional trade, investment and economic integration are viewed as part of ASEAN’s goals in integrating financial markets. (“Regional Cooperation in Finance”, 2016)

2. AEC Blueprint 2015

Put into effect in 2007, the AEC Blueprint 2015 focused on further clarifying the objectives of financial

integration. Under the blueprint, the “ASEAN minus x” approach was adopted allowing for flexible

commitments. The blueprint also adopted a schedule for financial services subsectors identified for

liberalisation by 2015.

3. In 2008, the ASEAN Capital Markets Forum (ACMF) outlined six strategic components of the Implementation

Plan:

Creating an Enabling Environment for Regional Integration

- Design and Implement a Mutual Recognition/Harmonization framework of gradually expanding

scope and country coverage (Strategic Component I)

Creating the Market Infrastructure and Regionally Focused Products and Intermediaries

- Implement an Exchange Alliance framework to facilitate cross-border trades with local brokers

initially; and strengthen and harmonize exchange governance, listing rules and corporate

governance framework (Strategic Component II) - Promote new products and regionally active intermediaries to build awareness of ASEAN as an

asset class (Strategic Component III) - Reinforce and expedite implementation of ongoing strategies and initiatives to strengthen and

integrate bond markets. (Strategic Component IV)

Strengthening the Implementation Processes

- Refine the strategies for domestic capital market development in each ASEAN country and

incorporate measures and milestones that support regional integration initiatives. (Strategic

Component V) - Strengthen the ASEAN level working mechanisms in order to better coordinate regional integration

initiatives and monitor and support its implementation at the country level. (Strategic Component

VI)

4. ASEAN Financial Integration Framework (AFIF)

Adopted in 2011, the AFIF continued the blueprint’s initial objectives whilst committing ASEAN to the goal of a

semi-integrated financial region by 2020. Several developments were added in subsequent installments:

- Differentiated timelines and targets for the ASEAN 5 and BCLMV nations in recognition of differing

states of development and readiness - Accord of equal access, treatment and environment to QABs;

- Regard to safeguard financial and monetary stability in the process of financial services

liberalisation, capital market development, capital account liberalisation and harmonisation of

payments and settlement systems; and - Shared responsibility among AMS for enhanced collaboration on financial stability and capacity

building.

5. ASEAN Banking Integration Framework (ABIF)

A framework agreement which was signed in 2015, the ABIF provided a guiding platform for the formation of

bilateral agreements between member states concerning the banking industry. Under the framework, Qualified

ASEAN Banks (QABs), which are defined by the individual bilateral agreements, will be given access to the

markets of member states with the support of central banks.

6. ASEAN Insurance Integration Framework (AIIF)

AIIF was finalised and agreed upon to guide the progressive liberalization to ensure more competitive

insurance markets and greater choice for consumers. Competitive insurance markets will lower the cost of

insuring business risks, which will stimulate economic growth and spur intra-ASEAN trade. ASEAN members

have agreed to prioritise the liberalisation of cross-border supply of Marine, Aviation and Goods in International

Transit (MAT) insurance.

B. Past Achievements

What has been achieved?

1. State of ASEAN Capital markets

As illustrated by the Figure #1, the disparity in the size of financial institutions and markets in member states

shows a developmental gap between the ASEAN 5 and CLMV nations

- With exception to Singapore, the capital markets of member states offer limited depth and liquidity,

and are therefore subject to excessive global capital flow volatility; this is only true when compared to

the relatively more systematically insulated nature of developed capital markets around the world

(Almekinders et el, 2014) - Despite its size, ASEAN’s market capitalisation jumped 12.2% in 2014 alone, whereas the

Compounded Annual Growth Rate (CAGR) of the ASEAN 5 bond market for the past decade stood

at 11.3% (ADB, 2015) - Increased growth however, cannot be attributed to financial integration between member states

2. Financial Services Liberalisation

As key financial intermediaries for the region, banks make up the bulk of ASEAN’s financial markets and can

be used as indicators of financial services integration through cross border activities.

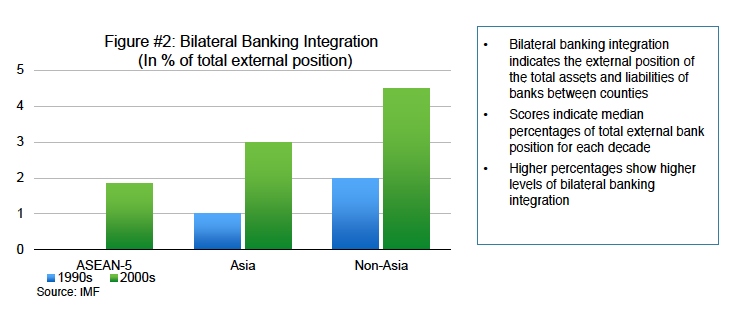

- As demonstrated in Figure #2, bilateral banking integration is relatively low within member states when

compared to the region and the rest of the world. - In 2009, foreign banks made up 18% of total commercial banks in Malaysia, the Philippines, and

Thailand; Malaysia accounted for the highest share of foreign ASEAN based banks at 8.5%. (IMF,

2015) Foreign banks in AMS countries are largely big sized international banks as opposed to ASEANbased

banks. (ADB, 2013) - Except Maybank Banking Berhad, no home grown ASEAN based bank has a branch or subsidiary in

all ASEAN countries; on the other hand, foreign owned and controlled insurance companies are

pervasive amongst member states, especially amongst the lesser-developed markets. (Lee, 2015) - The ABIF which was signed into effect by the Sixth Package of the AFAS in large part hopes to solve

the lack of ASEAN banking integration (Indonesian Ministry of Finance, 2015)

3. Capital Account Liberalisation

- The preliminary assessment and identification of rules relating to foreign exchange transactions has been

completed. - Member states have drafted individual roadmaps to liberalise capital account regimes.

4. Capital Market Development

- Agreement to adopt ISO20022 as a common standard for fund transfers in ASEAN, upon readiness of

individual countries - ASEAN Trading Link electronically connects exchanges in Malaysia, Singapore and Thailand providing

investors with easier and more seamless access into ASEAN markets from one single access point. - ASEAN Disclosure Standards provides significant efficiencies to issuers as they need only to adopt a

single set of disclosure standards for prospectuses in an offering across multiple ASEAN jurisdictions.

Malaysia, Thailand and Singapore are signatories to the Scheme. The Scheme is benchmarked against the

International Organisation of Securities Commissions’ (“IOSCO”) disclosure standards. A

Memorandum of Understanding (MoU) which establishes a Streamlined Review Framework for the

ASEAN Common Prospectus. - Through the Memorandum of Understanding (MoU) on Expedited Entry of Secondary Listings among

regulators and exchanges from Malaysia, Singapore and Thailand, the time-to-market for corporations

seeking a secondary listing in a participating ASEAN country has been reduced from the normal timeframe

of up to 16 weeks to 35 business days. - The ASEAN Corporate Governance Scorecard is based on a corporate governance ranking

methodology which leverages on methodologies already implemented in ASEAN countries, as well as

those applied by multilateral agencies such as the OECD. The Scorecard aims to raise corporate

governance standards and practices, showcase and enhance the visibility of well-governed PLCs and

promote ASEAN as an asset class internationally. - The ASEAN Capital Markets Infrastructure Blueprint aims to enhance connectivity of ASEAN capital

markets through post trading linkages. Having greater access to different markets helps ASEAN investors

to diversify risks and issuers to lower borrowing costs, while keeping transactions efficient. - The ASEAN Bond Market Development Scorecard monitors development of bond market development.

Starting with Malaysia, Singapore and Thailand, ASEAN member states have also developed and adopted

the ASEAN Debt Securities Standards. - ASEAN members monitor the progress of capital account liberalisation through the ASEAN Capital

Account Liberalisation Heat map and Individual Milestones Blueprint. - The Policy Dialogue Process on Capital Flows and Safeguard Mechanisms for Capital Account

Liberalisation allow ASEAN members to monitor capital flow trends and exchange experiences on capital

flow management. - The Principles and Guidelines on Pre-Departure Orientation Program ensure that migrant workers

receive adequate information to prepare them for their new life in their new destination, supporting a large

group in ASEAN that may lack access to financial education. - A Collective Investment Scheme (CIS) was operationalised in 2014, allowing for the cross border offering of products to signatory countries; five companies have already had their products approved as of 2015.

C. Present Challenges

What are the current issues?

1. Developmental Gap

The developmental gap which exists between ASEAN financial markets defines and divides the monetary and

fiscal policy goals of each member state. This in turn means that integration efforts are often retarded by

national restrictions and regulations, which is exacerbated by the ASEAN minus x formula.

2. Public-Private Collaboration

The success of ASEAN financial sector integration hinges not only on the policy reform of governments, but

also the efforts of private sector financial institutions and agents. Whilst policy reform has seen progress,

greater efforts will need to be placed on public private sector collaboration in order to see the true benefits of

integration efforts. In particular, a lack of private sector consultations has been highlighted as a key problem

with current policy direction. (Chia, 2011)

3. Translating regional commitments to country policy

Although the broad objectives and overarching regional commitments have been developed, comprehensive

initiatives have been lacking. As ASEAN continues to remain sensitive towards the policy objectives of member

states, various exclusions and exceptions and a time consuming national legislative process have been

marked as detrimental to financial integration. (Chia, 2011)

D. Future Plans

What new measures are included in the AEC 2025 Blueprint?

The AEC Blueprint 2025 refocuses financial sector integration with new measures relating to financial inclusion and stability; these two new areas largely involve information sharing initiatives and the adoption of best practices with regards to policy.

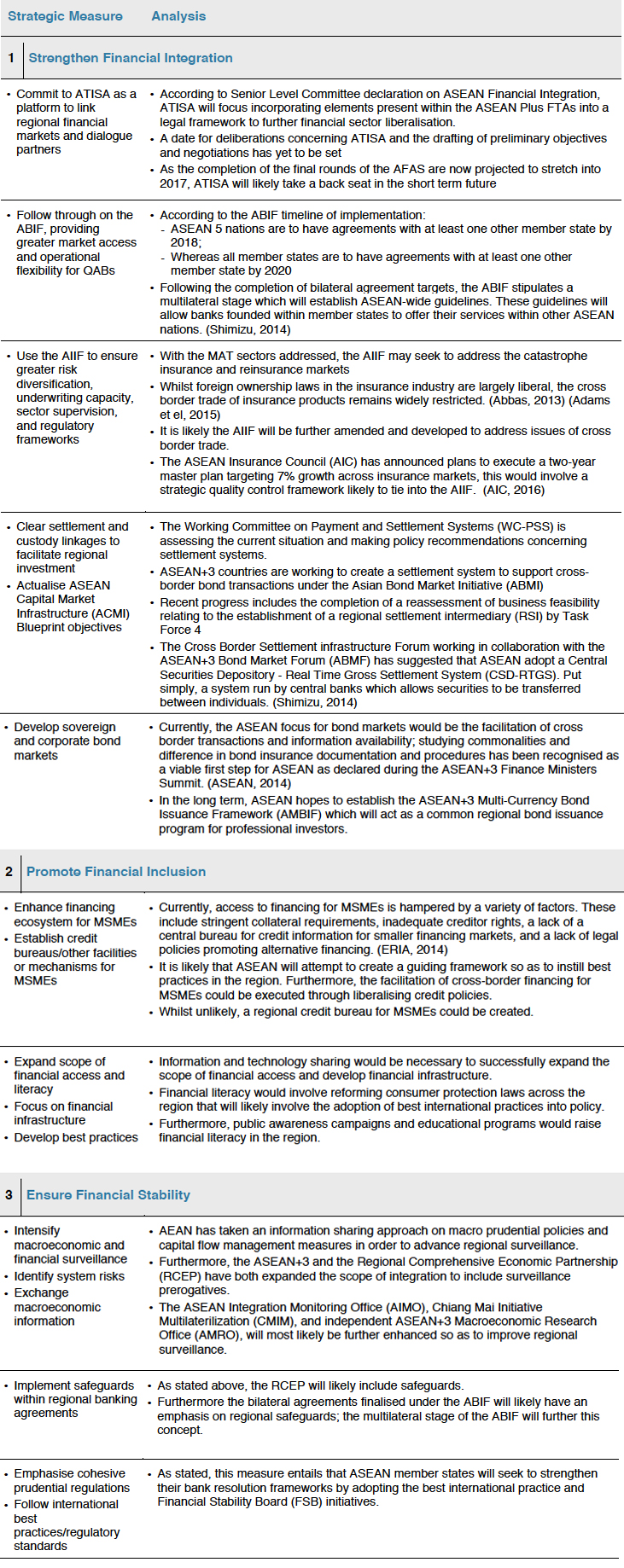

E. AEC 2025 Blueprint Analysis

What do the measures entail?

F. Conclusion

What does the AEC 2025 Blueprint mean in terms of the movement of skilled labor?

Given the development gaps among ASEAN member states, ASEAN has set itself a conservative target for

financial integration. Although the AEC Blueprint 2025 takes a step forward by introducing two new areas of

focus, financial inclusion and stability, the majority of strategic measures offered do not hint towards any big

changes in policy in achieving financial integration.

No central body such as the European Central Bank has been proposed, which continues to confirm that the

AEC’s goals lie towards financial integration tempered by flexibility rather than clear-cut unified policy.

Likely to be further developed under ATISA by 2017, the Blueprint focuses on completing previous objectives

and established initiatives.

References

Abbas, R. (2013, November). Waking up to an ASEAN community by 2015 – Dream or reality? Asia Insurance Review.

Adams, S., Irwin, G., & Caparelli, D. (2015). ASEAn Insurance Markets; Integration, Regulation, and Trade (Rep.). Global Council.

Almekinders, G., Fukuda, S., Mourmouras, A., & Zhou, J. (n.d.). ASEAN Financial Integration (Rep. No. 15/34). Asia and Pacific: IMF.

ACMF (2008). The Implementation Plan. ACMF. Vietnam, Danang.

ACMF (2013). ASEAN Regulators Implement Cross Border Securities Offering Standards.

ASEAN Insurance Council. (2016, February 8). Two Year Master Plan to Spur ASEAN Insurance Industry Growth

[Press release]. Retrieved February 8, 2016, from www.aseanic.org

ASEAN 2025: Forging Ahead Together, The ASEAN Secretariat (2015).

ASEAN. (2014, May 3). The Joint Statement of the 17th ASEAN 3 Finance Ministers and Central Bank Governors’ Meeting

[Press release]. Retrieved February 8, 2016, from http:/

www.asean.org/asean-economic-community/asean-finance-ministers-meeting-afmm/overview/

Secretariat, T. A. (2008). ASEAN Economic Blueprint.

Secretariat, T. A. (2015). ASEAN Intergration Report 2015.

Secretariat, T. A., & UNCTAD. (2015). ASEAN Investment Report 2015 Infrastructure Investment and Connectivity.

Secretariat, T. A. (2015). A Blueprint for Growth ASEAN Economic Community 2015: Progress and Key Achievements.

Shimizu, S. (2014). ASEAN Financial and Capital Markets —Policies and Prospects of Regional Integration (Vol. XIV, Ser. 54, Rep.). Japan Research Institute.