AEC Blueprint 2025 Analysis: Paper 23 | An Analysis of the ASEAN Cooperation in Healthcare

by Dr. Bambang Irawan | Published on 19 May 2017

Summary

The ASEAN healthcare cooperation has now received greater attention due to its growing importance in the AEC. While there are still gaps among member states in the quality of medical services provided, cross-border trade in medical services has taken place in the form of medical tourism and has seen significant growth in the past few years. Member states need to increase their efforts to improve other areas such as the mobility of medical professionals. This will help address the dearth of medical professionals in parts of Southeast Asia and further develop and improve the quality of medical services in the region.

Foreword

The following report is part of a series which attempts to provide a detailed analysis on the ASEAN Economic Community (AEC) Blueprint 2025. Each report will cover a single element of the blueprint, providing a comprehensive look at past achievements, present problems, and the future plans of the AEC. Special attention will be placed upon the strategic measures outlined in the AEC Blueprint 2025. This report aims to provide insight into the viability surrounding regional economic integration under the AEC.

ASEAN Cooperation in Healthcare

Cross-border provision of healthcare services in the ASEAN region has blossomed during the last few years with the emergence of medical tourism, particularly in Malaysia, Singapore and Thailand. The positive economic growth experienced by the region has allowed more people to seek medical services elsewhere to get the best treatment possible. Under the ASEAN 12 priority integration sectors that paved the way for the AEC development, one of the prioritised sectors is cross-border trade of healthcare products. It is then clear that ASEAN has recognised the healthcare sector as increasingly important in the development and establishment of the AEC.

In the AEC Blueprint 2015, healthcare services were mentioned as one of the four prioritised services sector to be substantially liberalised by 2010, together with air transport, e-ASEAN and tourism. Post 2015, with the increasing importance of healthcare, ASEAN member states have agreed to lay out the strategic measures to ensure that development and integration of this sector is systematically implemented. Health cooperation is also an area highlighted under the ASEAN Socio Cultural Community (ASCC) pillar as important to improve the regions resilience against diseases. Therefore, there may be some form of cross-sectoral cooperation in the healthcare sector in the future.

This report aims to review the progress made in the cooperation of integration in healthcare products sub-sector, and in the liberalisation of the healthcare services sub-sector. It will also attempt to analyse the measures under the AEC Blueprint 2025 and propose some recommendations that could improve the current implementation.

A. Targets under the AEC 2015 Blueprint

The AEC 2015 Blueprint did not outline specific strategies and targets for the healthcare sector, but instead it is mentioned under several other sectors, which have committed to supporting the development and integration of the ASEAN healthcare sector. Those sectors include:

1) Free flow of services, where ASEAN is committed to remove substantially all restrictions on trade in healthcare services by 2010

2) Priority Integration Sectors, where integration in ASEAN healthcare sector has been identified as one of them, with a roadmap that combines specific initiatives of the sector and the broad initiatives that cut across other sectors

In addition, as mentioned before, the ASCC pillar covers ASEAN health cooperation. Under this area, the specific strategic objectives include (i) ensuring access to adequate and affordable healthcare, medical services and medicine, and promoting healthy lifestyles for the peoples of ASEAN, (ii) enhancing regional preparedness and capacity through integrated approaches to prevention, surveillance and timely response to communicable and emerging infectious diseases, and (iii) reducing significantly the overall prevalence of illicit drug abuse in the general population.

B. Significant Achievements To Date

Since the AEC Blueprint 2015 does not prescribe any strategic measures and targets on the healthcare sector, the progress explained here will be limited to progress on the liberalisation of the sector.

| Area | Progress |

|---|---|

| Substantial removal of all restrictions on trade in healthcare services by 2010 |

|

| Roadmap for healthcare sector integration that combines specific initiatives of the sector and the broad initiatives that cut across all sectors |

|

C. Current Issues and Challenges

Healthcare expenditure

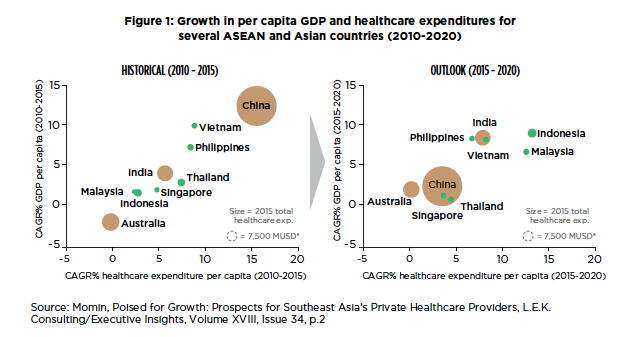

The future of healthcare sector in ASEAN is quite promising given the positive projection on the healthcare spending in the member states. By comparison, the average spending per capita in ASEAN is very low compared to that in advanced countries. For example, the average healthcare expenditure in the OECD countries was USD 4,471 in 2014, while the figure for ASEAN was only USD 643, suggesting a large potential for growth in the region. Figure 1 below describes the historical progress during 2010-2015 and the projected figures for 2015-2020. The chart on the left side of Figure 1 shows that there is a positive correlation between the compound annual growth rate (CAGR) of GDP per capita and that the CAGR of healthcare expenditure per capita and the level reached by ASEAN countries during 2010-2015 was lower than that of China. On the other hand, the chart on the right side of Figure 1 projects that between 2015 and 2020, ASEAN countries will experience higher growth than China and Australia with some countries introducing universal healthcare for most of the population.

MRAs and qualifications in the healthcare sector

However, some challenges remain for ASEAN member states to tackle. From the human capital point of view, ASEAN has not really encouraged the mobility of medical, dental and nursing professionals across the region, despite the commitments as exemplified in the MRAs, which has negatively affected supply of talents in some countries7. When cross-border movement can be allowed, the issue of inadequate supply of doctors and nurses in some areas can be addressed, and quite possibly, all member states would be able to participate in the medical tourism industry to attract patients from outside of the ASEAN region.

ASEAN currently does not have a standardised regional qualification and curriculum in the medical education, resulting in varying standards and skill base, and therefore limiting trade of services.

D. Plans under the AEC 2025 Blueprint

Under the new AEC Blueprint 2025, the cooperation in healthcare sector aims to promote the development of a strong healthcare industry that can contribute to better healthcare facilities, products and services to meet the growing demand for affordable and quality healthcare in ASEAN. This covers traditional knowledge and medicine, taking into account the importance of effective protection of genetic resources, traditional knowledge, and traditional cultural expressions.

The strategic measures under this sector include:

- Continue opening up of private healthcare market and public-private partnership (PPP) investments in provision of universal healthcare in the region.

- Further harmonise standards and conformance in healthcare products and services, such as common technical documents required for registration processes and nutrition labelling.

- Promote sectors with high growth potential such health tourism and e-healthcare services, which will not have negative impact on the healthcare system of each ASEAN member state.

- Promote strong health insurance systems in the region.

- Further facilitate the mobility of healthcare professionals in the region.

- Enhance further the development of ASEAN regulatory framework on traditional medicines and health supplements, through the setting of appropriate guidelines or frameworks.

- Continue to develop and issue new healthcare product directives to further facilitate trade in healthcare products in the region.

E. AEC 2025 Blueprint Analysis

The new blueprint has outlined what needs to be done to further develop and integrate the ASEAN healthcare sector, covering areas such as public and private roles, harmonisation of standards, health tourism, health insurance, and mobility of health practitioners. The table below provides some analyses on the progress on each measure in the blueprint.

| Issue | Current Status and Development |

|---|---|

| 1. Expansion of ASEAN Healthcare Market | |

| a. Greater public-private investments for better healthcare coverage in ASEAN |

|

| b. Harmonisation of standards and conformance in healthcare products and services |

|

| c. Promotion of high-growth sectors such as health tourism and e-healthcare services |

|

| d. Improvement of health insurance systems in the region |

|

| e. Promotion of cross-border movement of health practitioners across the region |

|

| 2. Development of regulatory framework and product directives | |

| a. Further development of regulatory framework on traditional medicines and health supplements (TM & HS) |

|

| b. Development and issuance of new healthcare product directives |

|

F. Conclusion: Moving Forward with the AEC 2025 Plans

ASEAN can further develop its health tourism sector by improving their medical capabilities and technology. As described above, Malaysia, Singapore and Thailand are the destinations for medical tourists from within as well as from outside of ASEAN. This has come at the expense of mainly the Indonesian medical sector which cannot yet compete with those three countries, resulting in many Indonesians seeking medical treatment elsewhere. The situation that Indonesia is facing can be addressed by facilitating mobility of medical practitioners, improving trade in medical devices, and partnering with travel and hospitality industries.

Member states need to work more to achieve 100 percent UHC as promoted by the United Nations’ Sustainable Development Goals. The current schemes existing in some countries have been able to provide both treatment and medicines but in larger countries like Indonesia, this has been very challenging. The government needs to find the right balance between public and private health coverage to ensure that the whole population can have access to better medical treatment and facilities. Further integration in the health insurance sub-sector could help promote greater health coverage throughout the ASEAN region, therefore discussions and cooperation between the health and finance authorities could pave the way for greater medical coverage. Figure 2 below explains the proportion between government and private healthcare funding. Brunei Darussalam’s government has made a substantial contribution to the healthcare coverage for the people. In most countries however, the private funding has dominated the provision of healthcare coverage with only Brunei Darussalam, Thailand and Malaysia having the government funding larger than the private funding. Myanmar and Cambodia are the countries whose private funding is the highest in the region.

The MRAs for ASEAN medical and dental professionals were signed in 2009 but to date ASEAN has not had competency standards and registration systems at both national and regional levels, which has discouraged the free flow of medical talents across the region. While natural barriers may exist (such as language abilities), ASEAN should continue to work towards facilitating free movements of those talents to help areas that cannot develop their health services due to shortage of doctors and nurses. Such facilitation of freer movements can also support the expansion of medical tourism and other health services in ASEAN.

Greater cooperation with the industry will help governments in moving forward and formulating strategies that could promote provision of health services. This includes the hospital, pharmaceutical (including traditional medicines) and health supplement industries.

1 Geared for health – ASEAN’s growing medical and healthcare industry by IPSOS Business Consulting (July 2015), p.4

2 Ibid p.4

3 Opportunities in ASEAN’s Healthcare Sector

4 UNWTO Tourism Highlights 2016 Report

5 Yoshinori Fukunaga, Assessing the Progress of ASEAN MRAs on Professional Services, ERIA 2015, pp.19-20

6 Zafar Momin, Poised for Growth: Prospects for Southeast Asia’s Private Healthcare Providers, L.E.K. Consulting/Executive Insights, Volume XVIII, Issue 34, p.1

7 Lifting the Barriers Reports, CIMB ASEAN Research Insitute, 2015, p.80

8 The content under this section is taken directly from the AEC Blueprint 2025 (ASEAN Secretariat, 2015).

9 Embracing Wellness, Healthcare, Invest in ASEAN

10 Budget 2017: RM25b allocated for healthcare boost, October 2016

11 Logan Connor, Region’s medical tourism boom fueled by Southeast Asians, May 2016

12 Healthcare insurance & reimbursement landscape in ASEAN markets, Deallus Consulting and JPMA, March 2015

13 An out-of-pocket maximum is the most a person has to pay during a policy period for healthcare services. Once the out-of-pocket maximum is reached, the person’s plan begins to pay 100 percent of the allowed amount for covered services.

14 Mohammad Faisal, AEC and congested labor mobility, 2016

15 ASEAN Alliance of Health Supplement Associations (AAHSA)

16 Lifting-the-Barriers Reports, CIMB ASEAN Research Insitute, 2015, p.78

17 Good Health and Well-Being: Why it matters

References

ASEAN Secretariat (2008). ASEAN Economic Community Blueprint

ASEAN Secretariat (2015). ASEAN 2025: Forging Ahead Together

ASEAN Secretariat (2015). A Blueprint for Growth ASEAN Economic Community 2015: Progress and Key Achievements

ASEAN Business Club (ABC) Forum. Lifting the Barriers Report 2015

Geared for health – ASEAN’s growing medical and healthcare industry by IPSOS Business Consulting (July 2015)

Healthcare insurance & reimbursement landscape in ASEAN markets, Deallus Consulting and JPMA, March 2015

Lifting-the-Barriers Reports, CIMB ASEAN Research Institute, 2015

Mohammad Faisal, AEC and Congested Labor Mobility, Jakarta Post, January 2016

Yoshinori Fukunaga, Assessing the Progress of ASEAN MRAs on Professional Services, ERIA 2015

Zafar Momin, Poised for Growth: Prospects for Southeast Asia’s Private Healthcare Providers, L.E.K. Consulting/Executive Insights, Volume XVIII, Issue 34