Policy Brief: EU’s Renewable Energy Directive (RED) II and Implications on Palm Oil Trade

Published on 2 December 2019

1. Policy in focus: Renewable Energy Directive (RED) II

In December 2018, the European Union’s revised Renewable Energy Directive entered into force with an extended deadline and a new renewable energy consumption target.

Referred to as Renewable Energy Directive (RED) II1, the new delegated act sets a new and binding renewable energy consumption target of at least 32% for 2030 for the whole of the EU, instead of the previous 20% by 2020 to be attained through individual national targets.

To lay out the implementation of this renewed directive, the European Commission adopted the Delegated Regulation (EU) 2019/807 2 on March 13 2019, which came into effect two months later following scrutiny by the European Parliament and the Council of the EU.

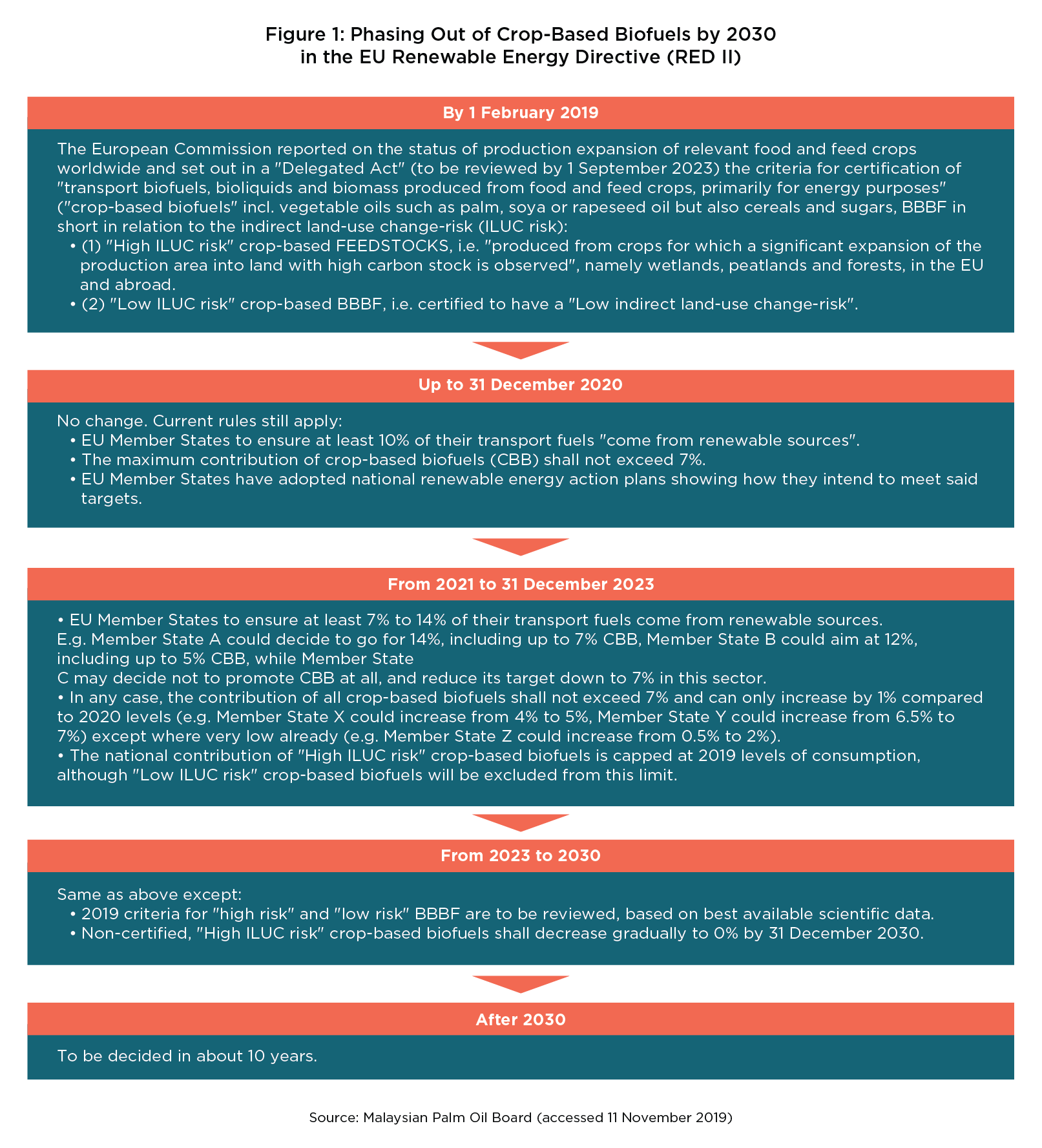

The revised directive, however, includes the phasing out of biofuels that use oil/feedstock certified as high indirect land-use change (ILUC)-risk3 by 2030 (see Figure 1).

- This will be achieved by placing limits in the interim on the amount of said biofuels that can be counted by individual member states when calculating the

- (a) overall national share of renewables and

- These limits on the amount of biofuels that can be counted towards the renewable energy target of 32% will be frozen at 2019 levels between 2021-2023, to be gradually decreased to zero from the end of 2023 to 2030.

- From 2023 to 2030, the criteria established in 2019 for ‘high risk’ and ‘low risk’ biofuels will be reviewed.

- (b) the share of renewables in transport

- By 31st December 2020, EU Member States must ensure that at least 10% of their transport fuel come from renewable sources.

- Between 2021 and 2030, EU Member States are now required to ensure fuel suppliers supply a minimum of 14% of the energy consumed in road and rail transport are renewable energy

- The renewed directive also maintains limitations on the consumption of crop-based biofuels (CBBs) for transport at 7%.

- Between 2021 to 2030, member states are allowed to increase their consumption of CBBs for transport by 1% compared to 2020 levels, up to the maximum 7%.

2. How does it impact Palm Oil?

The new element added to the revised directive seeks to ensure that crops used for the production of biofuels

- are not sourced from recently deforested areas or peatlands – no matter where they are produced, and

- they have not merely displaced other production to other high-carbon, high-nature value areas, elsewhere either.

The regulation defines‘oil crops’ as: food and feed crops such as rapeseed, palm, soybeans and sunflower, that are not starch rich crops and sugar crops that are commonly used as feedstock for the production of biofuels, bioliquids and biomass fuels.

The regulation also included a report that provided data that claims that:

- palm oil has been associated with the highest level of deforestation, where over the period 2008-2015, 45% of the expansion of palm oil took place in high carbon stock areas.

- Whereas for soybean, the world average fraction of soy expansion onto high-carbon land was estimated at 8%.

3. Countries affected and response

Both Indonesia and Malaysia, which account for around 85% of global palm oil supply (see Figure 2), have slammed the EU’s decision as discriminatory and protectionist in nature, and is designed to support European producers of other types of vegeFigure oils such as rapeseed and sunflower.

According to a media statement by the Malaysian Ministry of Primary Industries, member countries of the Council of Palm Oil Producing Countries (CPOPC) viewed the EU Delegated Act as a ‘political compromise’ aimed at isolating palm oil for the benefit of EU rapeseed oil and other less competitive imported vegeFigure oils, including through the ‘scientifically flawed’ concept of the ILUC.

- The member countries argued that the Delegated Act did not characterize soybean from selected sources as high-risk ILUC, despite in-house research by the EU concluding that soybean is responsible for far more ‘imported deforestation’.

It should be noted that rapeseed comprises 60% of all biofuel now, although the European Commission has stated this demand for the energy source will shrink by a tenth by the end of the next decade (EU farmers are currently the largest producers of rapeseed in the world).

51% of palm oil imported into the EU in 2017 was used to make biodiesel. Since the introduction of an EU law to promote biofuels in 2009, palm oil used to make biofuel has steadily increased from 825,000 tonnes in 2008 to 3.9 million tonnes in 2017. According to a media report, 750,000 of the two million tons of palm oil shipped from Malaysia to Europe were used in biodiesel.

Former Indonesian Trade Minister Enggartiasto Lukita was quoted as referring to the move as ‘an act of protectionism and trade war’.

Malaysian Prime Minister Mahathir Mohamad also responded that both countries are considering bringing the case to the International Court of Justice. As he stated “This is about world trade, and we have to look into trading practices first. If it breaches any international law, of course, we will go to the international court.”

During the seventh ministerial meeting of the CPOPC held in Kuala Lumpur in July 2019, both member states Malaysia and Indonesia stated they would challenge the Delegated Act through the WTO Dispute Settlement Act and other avenues.

- The meeting proposed to establish a CPOPC-EU Joint Working Group on Palm Oil (JWG), as a new platform to respond to the EU Delegated Act. The JWG shall engage CPOPC Member Countries and other palm oil producing countries (including in Africa), and will raise the issue of smallholder farmers and poverty alleviation to counter the Delegated Act.

- According to the press release, the meeting also welcomed the findings of a study entitled ‘Masterplan for the Strategic Implementation of SDGs in the Palm Oil Sector by 2030’ commissioned by CPOPC which lays out the foundation for a Master Plan for the strategic implementation of the UN Sustainable Development Goals in the palm oil sector by 2030. The study indicated that palm oil meets most of the 17 objectives of UN SDGs based on case studies conducted in Indonesia, Malaysia, Thailand, Colombia and Nigeria.

Recent media reports indicated that Malaysia and Indonesia intend to file separate complaints against the EU. It was also reported that both countries intend to set up a fund to counter criticism of the industry.4. A snapshot of the Palm Oil Industry and the EU Market

a) Palm oil exports to Europe are declining- Palm oil exports from both Indonesia and Malaysia were already in decline before this dispute first arose. Independent Australian research institute Future Directionsnoted that Malaysian and Indonesian palm oil exports to the EU have dropped from US$4.4 billion in 2014 to US$3.3 billion in 2018.

- Malaysia’s palm oil exports to the Netherlands, the EU’s largest palm oil importer, dropped by 9.1% between 2017 to 2018. It further declined by 8.35% between January-July 2018 and January-July 2019 (see Figure 3).

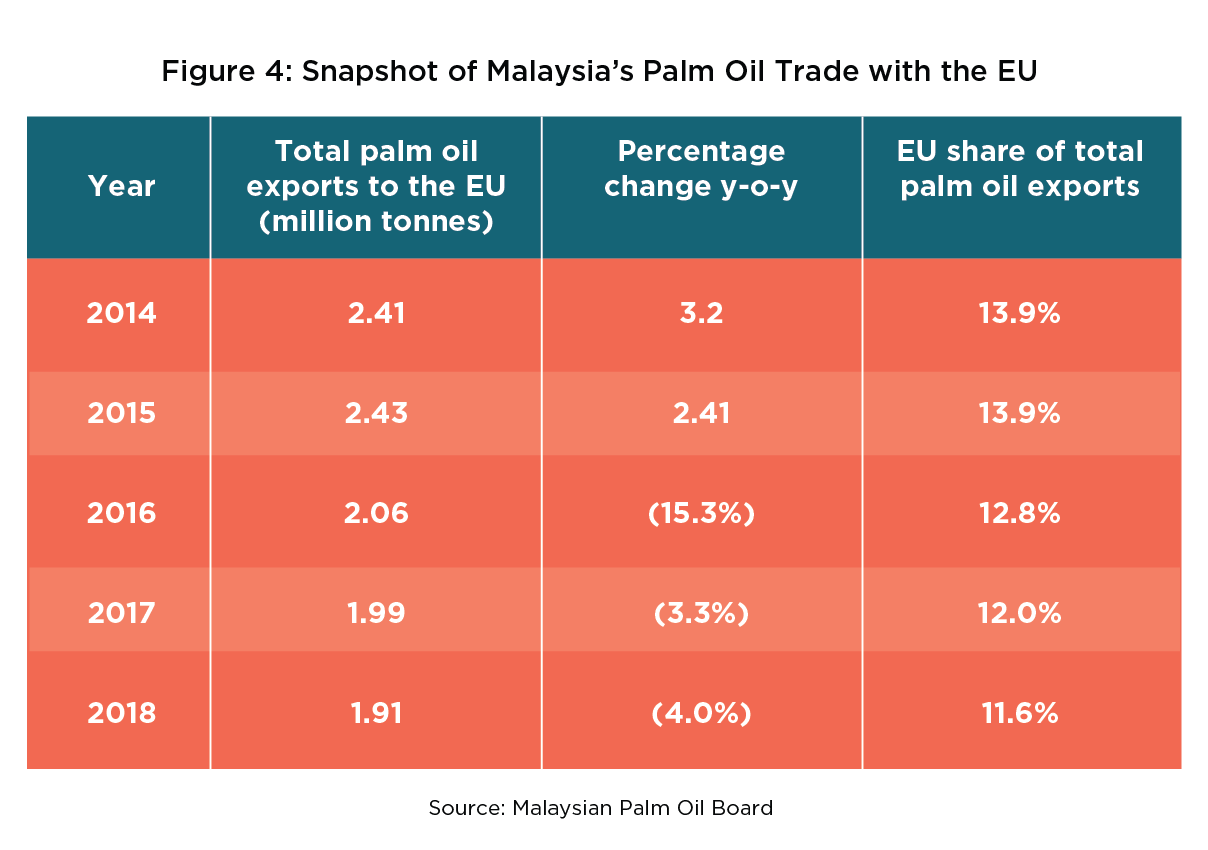

- According to the Malaysian Palm Oil Board, Malaysian total palm oil exports to the EU declined by 4.0% to 1.91 million tonnes in 2018 from 1.99 million tonnes in 2017 (see Figure 4).

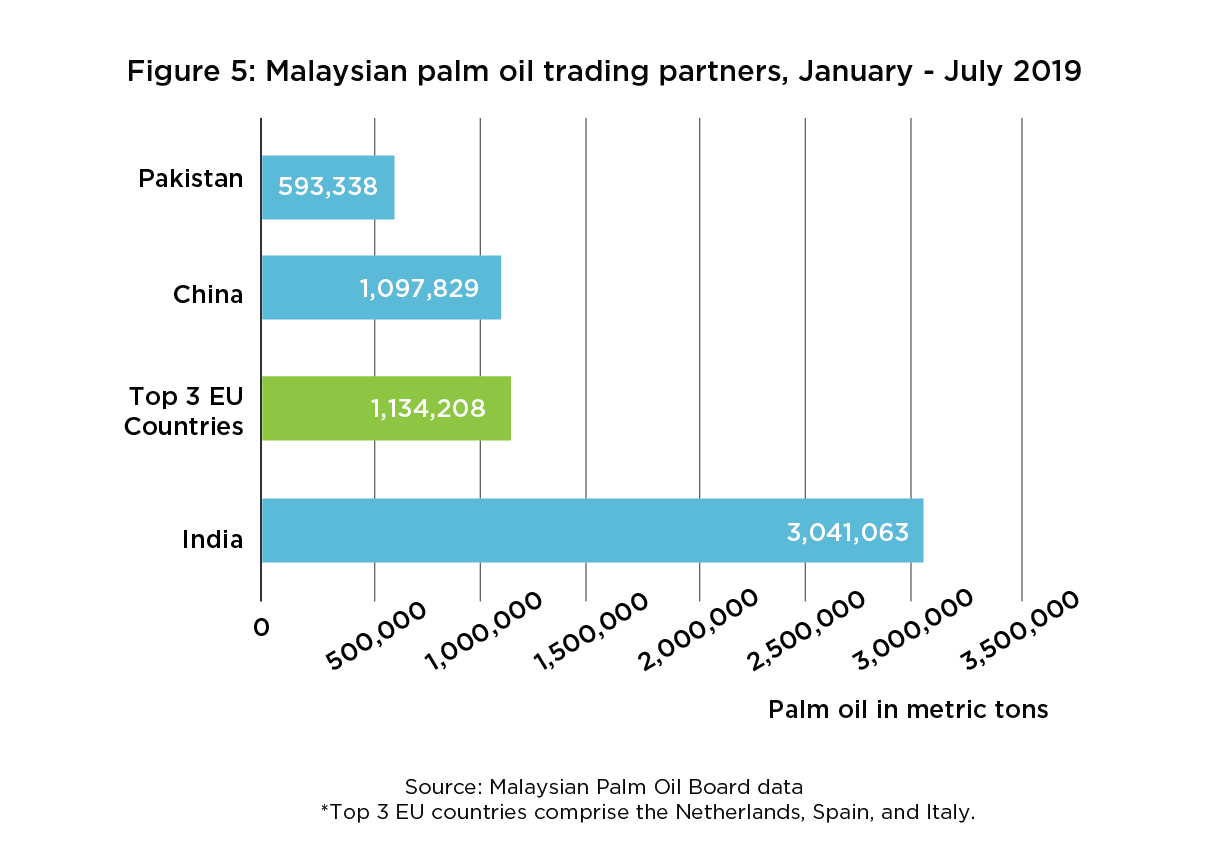

- The Netherlands, Spain, and Italy collectively comprised the second largest importer of Malaysian palm oil behind India (see Figure 5).

b. Palm oil compose a small proportion of total EU tradeWhile palm oil is an important export for Indonesia and Malaysia to the EU, often their biggest single exported goods to the bloc, it has declined in terms of volume from 2017 to 2018 and is worth less than 20% of their total trade with EU. Specifically:

- Indonesian exports of palm oil products to the EU totalled some US$2.1 billion in 2018, accounting for 12% of Indonesia’s total exports in 2018, down from 17% in 2016.5

- Malaysia’s exports of palm oil products to EU declined 4% year-on-year to US1.9 billion in 2018. The EU accounted for 11.6% of Malaysia’s palm oil export market in 2018.6

5. The palm oil industry faces increasing pushback

a) EU tariffs on Indonesian biodieselSeparately on 13 August 2019, the European Commission re-imposed countervailing duties of up to 8% to 18% on imports of subsidised-biodiesel from Indonesia, claiming that Indonesian biodiesel producers benefit from ‘grants, tax benefits and access to raw materials below market prices’.

The provisionally re-imposed tariffs will last until December, but could be extended for five years. The EU had previously scrapped tariffs on Indonesian imports in 2019 on orders of the WTO.

In focus: India’s tariffs on Malaysian refined palm oil

On 4 September 2019, India increased customs duties on refined palm oil from Malaysia by 5% to protect local producers. According to data from the Malaysian Palm Oil Board, India was the largest importer of palm oil from Malaysia between January-July 2019, at over three million metric tonnes.Previously, India levied a 40% duty on crude palm oil imports and 50% on refined palm oil imports. However, refined palm oil imports from Malaysia were taxed at 45% due to the India-Malaysia Comprehensive Economic Cooperation Agreement, which was signed in February 2011 and came into force in July later that year.

Analysts believe the levy will erode the competitiveness of Malaysian refined palm oil, with Indian importers possibly switching to purchases from Indonesia. However, they also argued that the decline in palm oil exports to India should be partially offset by demand in China following the latter’s suspension of the purchase of US agricultural products as part of the ongoing trade war.

Indonesia was overtaken by Malaysia as India’s largest supplier of palm oil in 2019, in part due to the India-Malaysia Comprehensive Economic Cooperation Agreement giving Malaysian exporters a competitive edge.

Malaysian crude palm oil exports to India was not affected however, and Indian importers may request Malaysian palm oil producers to replace refined palm oil with crude. However, Indonesian CPO are reportedly cheaper and may be imported instead.

On 1 October 2019, it was reported that India was considering limiting the import of palm oil in reaction to Malaysian Prime Minister Mahathir Mohamad’s comments about India’s actions in Kashmir. Based on government and industry sources, it was argued that India is planning on substituting Malaysian palm oil with edible oils from other countries such as Indonesia, Argentina, and Ukraine. The news prompted Malaysian palm oil futures to drop on the Bursa Malaysia Derivatives Market on the evening of Friday 11 October ending five days of gains. Like the EU, Malaysia currently benefits from a trade surplus with India, meaning it lacks the economic tools to retaliate to any move by India to disrupt trade. (Figure 6)

In response to this development, on 15 October, Minister of Primary Industries of Malaysia Teresa Kok in a statement said that Malaysia had offered to buy more raw sugar and buffalo meat from India, ‘in light of India’s importance as Malaysia’s third-largest export destination in 2018 for palm oil and palm-based products worth 6.84 billion ringgit ($1.63 billion).’

On 21 October, the Mumbai-based Solvent Extractors’ Association of India advised its members not to purchase Malaysian palm oil, with its President stating that ‘In your own interest as well as a mark of solidarity with our nation, we should avoid purchases from Malaysia for the time being.’

On 22 October, Theresa Kok urged the Association not to take unilateral action and to allow governments of both countries to resolve the issue diplomatically.

6. EU’s response to the dispute

In response to Malaysia and Indonesia’s protests that the revised Directive is discriminatory towards palm oil trade, the EU laid out these defenses:

- No discrimination: The European Commission defended the regulation in that no specific biofuel or feedstock is targeted as all vegeFigure oils are treated equally.

- Exclusion of low ILUC-risk palm oil: Palm oil that is certified as low ILUC-risk can continue to benefit from incentives. Exemptions include for example planting on unused lands.

- Exclusion of small holders: Noting the importance of smallholders in Indonesia and Malaysia, the delegated regulation has set the threshold for small holders to 2 hectares to ensure that their tenure and independence over land is secured.

- Future Reassessment: The European Commission will reassess the data and if appropriate the methodology in 2021 and will carry out a revision of the Delegated regulation in 2023. It states that any efforts undertaken by Indonesia (such as a revamped ISPO, the moratorium, the one map policy, or the recently adopted national action plan) will be taken into account while reassessing the data.

7. Do Malaysia and Indonesia have economic leverage over the EU?

Both Indonesia and Malaysia ultimately need the EU as a trading partner more than the EU currently needs them. This limits the tools at their disposal to retaliate to the EU’s moves.

Almost 10% of all Indonesian exports are shipped to the EU, yet the EU sells less than 1% of its goods to Indonesia. Indonesia’s threats to increase tariffs on EU dairy products to 20-25% will not be a significant blow to the EU, as the bloc’s dairy products only account for 2% of the EU’s total exports to Indonesia in 2018 (about US$220 million worth of dairy products).

Likewise, Malaysia’s threats to drop its planned procurement of US$1 billion worth of military hardware from European states is unlikely to influence Europe’s environmentalist lobby.

Both Indonesia and Malaysia ultimately export more to the EU than they import, meaning both countries will be more exposed to trade vulnerabilities.

- According to the European Commission, EU imports from Malaysia totalled €25.6 billion in 2018, while EU exports to Malaysia reached €14.2 billion. This gave Malaysia a trade surplus of €11.4 billion. While the EU is Malaysia’s third largest trading partner, Malaysia is only 23rd largest trading partner for the EU (see Figure 5).

- Likewise, according to the European Commission, in 2018 EU imports from Indonesia totalled €16.6 billion, while its exports to Indonesia totalled €10 billion. This gave Indonesia a trade surplus of €6.6 billion. While the EU is Indonesia’s third largest trading partner, while Indonesia is the bloc’s 31st largest trading partner (see Figure 7).7

However, it should be noted that the WTO has already ruled that trade policy can be used to influence environmental issues, as long as the applied measures are not blatant protectionism. In fact, the Indonesia-European Free Trade Association Comprehensive Economic Partnership Agreement, signed in December 2018, includes conditionalities on Indonesia’s environmental progress. Any complaint filed to the WTO could also take years to adjudicate.

8. Impact on FTA negotiations

The dispute may also affect negotiations for a free trade agreement between Indonesia and the EU, with the eight round of talks having concluded in June 2019, and another round set for December 2019. However, while Indonesia’s palm oil exports to the EU are worth around $2 billion per year – and already declining yearly – a FTA with the EU would almost immediately boost Indonesian exports to the bloc by between 17.3-17.7%, or around $7.5 billion, according to an EU assessment report released in April 2019.

- On November 1 2019, it was reported that Indonesian vice foreign minister Mahendra Siregar had stated that Indonesia was currently reviewing its draft trade deal with the European Union to ensure that palm oil was positioned ‘fairly’ in the planned deal. This would be in the run-up to filing a complaint with the WTO.

An FTA between Malaysia and the EU will also no doubt be affected by the dispute over palm oil, with negotiations over a trade agreement having stalled since 2012. There are no signs as of yet that they will continue due in part to the palm oil dispute.9. Moves by Malaysia and Indonesia towards improving palm oil production practise

Malaysia and Indonesia have made concerted efforts to improve the image of their respective industries.

Indonesian President Joko Widodo made a moratorium on forest clearing for new palm oil plantations permanent, protecting some 66 million hectares.

In Malaysia, the government is trying to push the Malaysian Sustainable Palm Oil (MSPO) certification system, which emulates the voluntary RoundFigure on Sustainable Palm Oil (RSPO) and International Sustainability and Carbon Certification (ISCC). MPOCC stated that ‘By 2020, palm oil shipments into Europe will be certified under MSPO and sustainably produced’. Official data by the MPOCC showed that, as of October 31 2019, an estimated 58.5% of total oil palm area in Malaysia have been certified under the MSPO.

Beyond certification, the Malaysian government has also implemented regulations to make the palm oil industry more sustainable, including capping the total of oil palm cultivated area to 6.5 million hectares, stopping the planting of palm oil in peatland areas, and making palm oil plantation maps available for public access.

In focus: The palm oil industry and the haze crisis

The recurring haze problem afflicting Malaysia and Singapore, caused mainly by forest clearing activities in Indonesia, will no doubt further tarnish the reputation of the palm oil industry. In recent years, the problem has accelerated as more land has been cleared for expanding plantations for the lucrative palm oil trade (although there is a lack of consensus on whether large commercial plantations or small farmers are more at fault).

The haze which affected Malaysia and Singapore between September and October 2019 was considered particularly severe, more so than the fires of 2015 which was believed to have been responsible for 100,000 premature deaths. Media reports in September 2019 indicated that there were close to 3,000 forest fires raging in Indonesia. On 18 September 2019, a total of 553 schools nationwide in Malaysia were closed affecting 312,337 students, while flights in several areas were also cancelled due to low visibility.

Both the Indonesian and Malaysian governments disagree on who is to blame for the haze. In September 2019, Indonesian authorities pointed fingers to the subsidiaries of Malaysian plantation companies, claiming they are responsible for the open burning, although sources claim foreign-operated plantations in Indonesia often face greater scrutiny than local ones.

An Indonesian government audit released on 23 August 2019 found that roughly 81% of oil palm plantations in the country are in violation of industry regulations, including lacking a right-to-cultivate permit, encroaching into protected areas, and non-compliance with the Indonesian Sustainable Palm Oil (ISPO) standard.

The findings echoed a similar audit by the country’s anti-corruption agency in 2016, which concluded that the palm oil industry lacks credibility and accountability. The Indonesian government continues to refuse to release documents detailing plantation boundaries, ownership, and licenses, claiming that the information is of national strategic interests.

However, according to a September 2019 statement by the Minister of Primary Industries of Malaysia Theresa Kok, it is ‘unfair’ to blame the palm oil industry for the haze crisis, as many companies in the industry adhere to sustainable agricultural standards. She also argued that the haze was occurring during the forest fire and El Nino season, with many plants and trees located on flammable peat soil.

10. Conclusion

The ongoing dispute between the EU and ASEAN Members Malaysia and Indonesia over RED II is complex and multifaceted. The EU claims RED II is a non-discriminatory measure aimed at phasing out potentially environmentally-damaging biofuels, while Malaysia and Indonesia argue the revised directive is merely a form of protectionism for European agricultural interests.

Given both Malaysia and Indonesia’s current vulnerabilities towards external shifts in the global palm oil trade, it will be incumbent on both governments to manage relations with the EU and India, both key palm oil markets, as diplomatically as possible.

Prudency will also demand that Malaysia and Indonesia actively seek out new markets for their palm oil exports to manage risks and cushion the impact of any stoppage from one particular market (China in particular has been identified as a viable alternative market).There have also been efforts on the part of the Malaysian and Indonesian government to encourage further domestic consumption of palm oil to offset possible disruptions to exports. In particular, Indonesian President Joko Widodo’s mandate for conventional diesel with 30% palm-based biodiesel to be in effect by January 2020 (and at 50% by the end of 2020) is believed to have led to a surge in palm oil prices from a year low in July 2019 to its highest level in two years (see Figure 8).

1 As defined by the European Commission: ‘directives require EU countries to achieve a certain result, but leave them free to choose how to do so. EU countries must adopt measures to incorporate them into national law (transpose) in order to achieve the objectives set by the directive.’

2 As defined by the European Commission: ‘delegated acts are legally binding acts that enable the Commission to supplement or amend non‑essential parts of EU legislative acts, for example, in order to define detailed measures.’

3 ILUC refers to the conversion of non-agricultural land into agricultural land to produce food or feedstock, which can lead to the release of stored carbon emissions especially when it affects land with high carbon stock such as forests, wetlands, and peat land.

Research Director: Hong Jukhee

Editorial Team: Mohd Imran Said Mohd Shamsunahar, Gan Bo Ren, Janet Leong, Nor Amirah Mohd Aminuddin

- (a) overall national share of renewables and